The Philadelphia Semiconductor Index, or SOX, is on a tear – it’s up about 50% in the last 30 days, and 164% over the past 12 months as investors continue piling into chip stocks powering the AI buildout.

Claim 55% Off TipRanks

Forget margin or options. Here's how the pros trade NVDAWhat began with enthusiasm around AI accelerators has now spread across nearly the entire semiconductor ecosystem. GPUs remain at the center of the boom, but demand is also rippling through memory makers, networking suppliers, data center hardware companies, and the equipment manufacturers helping expand global chip production capacity.

That backdrop has kept investors heavily focused on two of the AI industry’s biggest names – Nvidia (NASDAQ:NVDA) and Advanced Micro Devices (NASDAQ:AMD). Morgan Stanley analyst Joseph Moore, whom TipRanks ranks among the top 2% of Wall Street analysts, has been closely tracking both companies and believes one currently holds a clearer advantage in the AI race.

We’ve opened up the TipRanks database to take a close look at both Nvidia and AMD to see where they stand and how the Morgan Stanley expert ranks them. Here are the details, along with Moore’s comments on the stocks.

Nvidia

We’ll start with NVIDIA, the chip giant that has become the defining winner of the AI boom. Now carrying a market cap of $5.23 trillion, Nvidia stands as the world’s most valuable publicly traded company as demand for its AI chips and data center systems continues accelerating at an extraordinary pace.

The company entered the surge in AI spending with a strong advantage through its dominance in GPUs and other high-performance processors used to train and run advanced AI models. Yet, Nvidia’s advantage extends well beyond hardware alone. Its CUDA software ecosystem has become deeply embedded across hyperscaler and enterprise AI infrastructure, giving developers and companies a massive installed base of tools, applications, and workflows built around Nvidia’s platforms, making the company difficult to displace.

That ecosystem has helped Nvidia strengthen its hold on the AI infrastructure market at a time when cloud computing giants, including Microsoft, Amazon, Alphabet, and Meta continue committing hundreds of billions of dollars toward AI servers and next-generation data centers. As those companies expand computing capacity for generative AI applications, Nvidia remains one of the primary beneficiaries of the spending surge.

The strength of Nvidia’s AI business can be seen in its last quarterly financial report. During fiscal fourth quarter 2026, the company generated $68.1 billion in revenue, topping Wall Street expectations by $1.9 billion. Data center revenue alone reached $62.3 billion, accounting for more than 91% of total sales. Overall revenue climbed 73% year-over-year, while the data center segment surged 75%. On the bottom line, Nvidia posted non-GAAP earnings of $1.62 per share, nearly doubling the $0.89 reported in the same quarter last year and exceeding consensus estimates by 8 cents per share.

Among the bulls is analyst Moore, who believes Nvidia may still have more room to run despite its enormous size.

“NVIDIA has consistently put up more upside to quarterly guidance than either of these competitors, and while just how strong 2027 is remains to be seen, we believe that NVIDIA’s forecast leaves the most room for upside in the base case. Market share in this environment has more to do with supply chain, and we increasingly see potential for bottlenecks in other parts of the supply chain may actually bring preference to NVIDIA given a non supply limitation on GPU/XPU…. Our view is that the company’s market share will be more stable than the market thinks, and that the strength in AI spending will last longer (and we are less focused on the rate of growth in CY27 then the sustainability),” Moore opined.

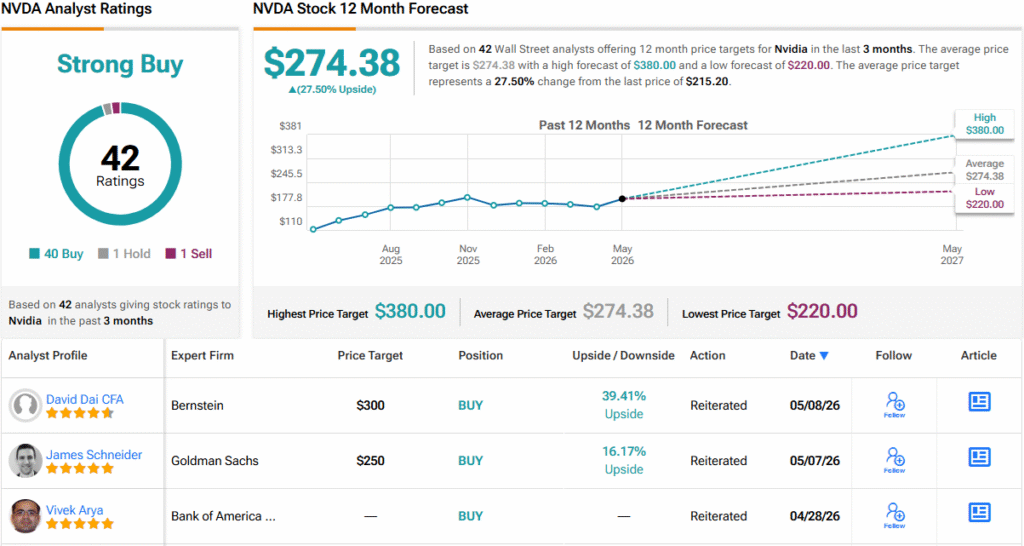

Backing up his bullish stance, Moore assigns NVDA shares an Overweight (i.e., Buy) rating with a $260 price target that points to ~21% upside potential from current levels. (To watch Moore’s track record, click here)

Overall, Wall Street analysts continue to line up behind NVDA. The stock boasts a Strong Buy consensus rating based on 42 recent analyst reviews, with 40 recommending Buy ratings versus just one Hold and one Sell. At the current share price of $215.20, the average price target of $274.38 suggests the rally may still have another 27.5% left in the tank over the coming year. (See NVDA stock forecast)

Advanced Micro Devices

The second stock we’ll look at is AMD, one of the semiconductor industry’s biggest names in the race to supply the hardware powering AI. Investor enthusiasm around the AI buildout has fueled a massive rally in the stock, with AMD shares soaring 347% over the past year and 112% this year alone.

The company is battling Nvidia in the market for AI accelerators while also competing against the growing adoption of ASIC chips, a category largely led by Broadcom. Although AMD has made meaningful progress with its expanding AI product lineup, it entered the race from a smaller position and still faces the challenge of gaining share against larger and more deeply entrenched rivals.

AMD has recently accelerated its AI push with the rollout of its Instinct MI350 series and the planned launch of its next-generation MI400 platform and Helios AI server architecture, part of a broader effort to compete not just on chips, but on full rack-scale AI systems.

The company has also started gaining traction with major cloud and AI customers, including Oracle and OpenAI, even as Nvidia continues to dominate the market. AMD is attempting to narrow that gap with its ROCm software platform, which has become a major focus in the company’s effort to win larger AI deployments.

In its recently reported fiscal first-quarter 2026 results, AMD generated $10.3 billion in revenue, up nearly 38% year-over-year and $336 million ahead of Wall Street expectations. The company’s data center segment, which includes its AI-related business, accounted for $5.8 billion of that total, representing about 56% of overall revenue. On the bottom line, AMD reported non-GAAP earnings of $1.37 per share, topping consensus estimates by 8 cents and rising from the $0.96 posted in the year-ago quarter.

Joseph Moore, in his coverage here for Morgan Stanley, notes that AMD is generally strong – but that the AI competition against larger competitors in a tough field remains something of a question mark.

“We would have thought server enthusiasm was already priced in given the sharp move in the stock, but in the last few weeks there seems to be limitless enthusiasm for CPU and management’s long term commentary was probably more impactful than the modest near term upside… We still believe that we are in a very strong investment phase for AI hardware, which should help, but in a very competitive market where NVIDIA and the ASIC vendors are all moving quickly, we will need to see a very strong MI400 offering next year for AMD to cement that position. AMD’s position in all of its other markets remains strong, given Intel’s disarray, but AI remains uncertain,” Moore wrote.

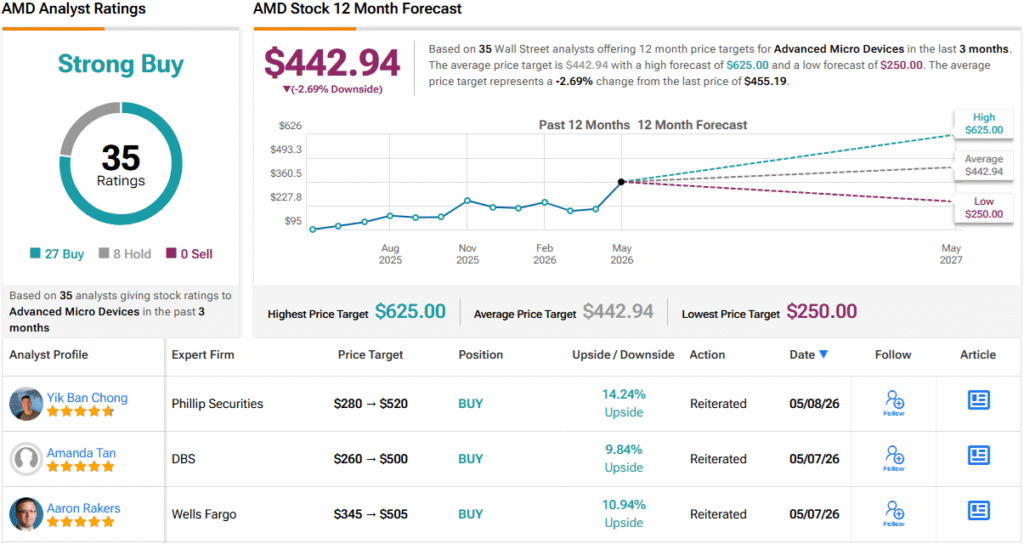

These comments support Moore’s Equal-weight (i.e, Neutral) rating on AMD. His price target, currently set at $410, suggests the stock has ~10% downside from current levels.

As a whole, Wall Street is more bullish on AMD than is Morgan Stanley. The stock has a Strong Buy consensus rating, based on 35 reviews that include 27 Buys and 8 Holds. Yet, after the stock’s massive recent run and despite that positive sentiment, the average price target of $442.94 sits slightly below the current share price of $455.19. (See AMD stock forecast)

With the facts laid out, it’s clear that Morgan Stanley’s top analyst Joseph Moore sees Nvidia as the stock to buy for investors seeking exposure to the chip sector.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.