The AI boom has reshaped the growth of the semiconductor industry, turning chips into the foundation of the global compute economy. Investment in AI data centers now flows through the entire semiconductor stack, from GPUs and AI accelerators to HBM memory chips, networking silicon chips, and advanced packaging.

Meet Samuel – Your Personal Investing Prophet

Explore NVDS for 2X short leverage on NVDAThat has opened up big investment opportunities, as demand for AI chips has only grown more acute and chip stocks have become some of the market’s best performers over the past few years.

Wall Street’s biggest investors have naturally been taking advantage of this situation, among them billionaire investor Steve Cohen, the founder of Point72 Asset Management, a hedge fund that boasts $40 billion in AUM (assets under management).

Cohen’s portfolio includes giants such as Nvidia (NASDAQ:NVDA) and Advanced Micro Devices (NASDAQ:AMD), but recently, the billionaire has shown a clear preference for one over the other, opening his checkbook for one AI stock while selling a chunk of the other.

So, we’ve decided to get the lowdown on both and find out what might be behind Cohen’s recent moves.

Nvidia

Nvidia has grown into something the market has never really seen before. With a valuation of $5.3 trillion, the AI chip giant is now worth more than the entire stock markets of countries such as the UK, France, and Germany, while only a handful of national economies still exceed Nvidia’s size.

Over the past several years, Nvidia has assembled an expansive AI computing ecosystem spanning GPUs, networking hardware, software platforms, AI systems, and full-scale data-center architectures. Its CUDA software stack remains deeply embedded within the AI ecosystem, giving Nvidia a substantial advantage as technology firms race to deploy larger and more sophisticated AI models.

That position has become even more important as the industry shifts toward massive inference workloads and enormous “AI factories” built by hyperscalers and sovereign governments. Nvidia’s Blackwell platform now sits at the core of that buildout, with demand for GB300 systems and NVL72 racks continuing to climb among cloud providers and frontier model developers. Networking products such as NVLink, Spectrum-X Ethernet, and Quantum-X InfiniBand have also become essential as AI clusters expand into tens of thousands of GPUs.

At the same time, Nvidia is already preparing its next generation of AI infrastructure. CEO Jensen Huang recently highlighted the upcoming Vera Rubin platform, which is expected to extend Nvidia’s position further in AI inference and accelerated computing. The company is also moving deeper into robotics, autonomous vehicles, industrial AI, and sovereign AI infrastructure, broadening Nvidia far beyond its original role as a semiconductor designer.

That momentum was evident once again in Nvidia’s newly released fiscal first-quarter results. Revenue climbed 85% year-over-year to $81.62 billion, surpassing expectations by $2.65 billion. Data Center revenue reached a record $75.2 billion, up 92% from the same period last year, driven largely by continued strength in Blackwell deployments. Adjusted EPS came in at $1.87, topping consensus estimates by $0.10, while Nvidia projected fiscal second-quarter revenue of approximately $91 billion, well above Wall Street expectations of near $87 billion.

In a sense, Nvidia is now a victim of its own success. Because it is such a monster, the threshold for impressing the market has become extremely high. As such, strong earnings are no longer enough on their own to deliver the kind of explosive stock moves shareholders once grew accustomed to.

That backdrop may help explain why Steve Cohen trimmed his Nvidia position during the first quarter, selling 2,402,596 shares and cutting his stake by 25%.

Investor Jonathan Weber, who ranks among the top 2% of stock pros on TipRanks, is among those who believe Nvidia’s latest quarterly report reinforced the company’s long-term strength. Yet, that does not automatically make the stock an obvious buy after its enormous run.

“Nvidia’s results looked pretty good all in all, but that was not much of a surprise — the company regularly outperforms expectations,” the 5-star investor said. “Revenue growth accelerated, which is great, while margins seem to have more or less flattened out, which isn’t great but okay. Does that make NVDA a buy?… I thus believe that investors could do quite well over a multi-year time frame if they hold Nvidia and if the AI boom continues, but I think right now isn’t an ideal time to enter or expand a position — better buying opportunities could materialize, as they have done from time to time in the past.”

Accordingly, Weber rates the shares a Hold (i.e., Neutral). (To watch Weber’s track record, click here)

Most on the Street, however, remain firmly in Nvidia’s corner. Based on a mix of 40 Buys vs. 1 Hold and Sell, each, the stock claims a Strong Buy consensus rating. At $299.97, the average price target points toward 12-month returns of 36%. (See NVDA stock forecast)

AMD

Nvidia remains the undisputed AI chip king, but several companies are working hard to close the gap, one of the most prominent being AMD. Nvidia might have gotten a head start in the AI-driven new paradigm, being faster to repurpose its hardware for AI workloads, while AMD lagged in both software ecosystem depth and AI-specific optimization, but it is now catching up.

Its data center business is growing fast, supported by strong demand for its MI300 lineup and expectations surrounding its next-generation MI400 AI accelerators, seen as able to realistically compete with Nvidia’s offerings. The company has also been nabbing some significant deals, including collaborations with Meta and OpenAI.

Meanwhile, the rise of agentic AI has been a massive boon for AMD’s core CPU business. Because AI agents depend more on coordination, decision-making, and moving data around than on pure number-crunching, the industry is seeing stronger demand for CPUs. Traditional generative AI training is still heavily GPU-focused, but agentic workflows tend to need more balanced systems overall. This shifts the GPU-to-CPU mix from an 8-to-1 or 4-to-1 ratio closer to a 1-to-1 relationship, driving massive demand for server CPUs.

AMD’s booming business was on display in its recent Q1 readout. Revenue came in at $10.25 billion, up 37.8% year-over-year and ahead of expectations by $330 million. The data center segment generated $5.8 billion in revenue, rising 57% compared with the same period last year. At the bottom-line, adj. EPS landed at $1.37, beating the Street’s forecast by $0.08.

Looking ahead to the second quarter, AMD guided for revenue of about $11.2 billion, plus or minus $300 million, compared with consensus expectations of $10.52 billion.

Cohen must have liked all of that. During Q1, he bought 868,663 AMD shares, increasing his holdings by 160%. That stake is currently worth more than $388 million.

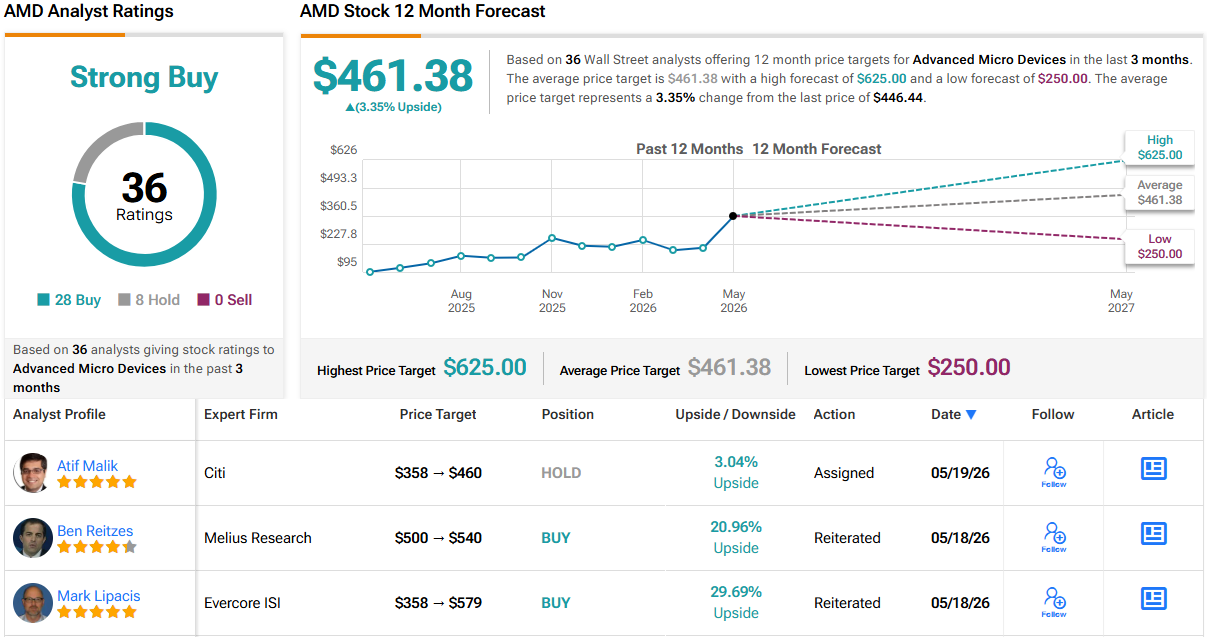

AMD also gets the endorsement of Melius Research analyst Ben Reitzes, who thinks the future looks bright for the Lisa Su-led company.

“AMD is positioned to benefit from GPU and CPU upside long-term, and recent progress in OpenAI enterprise revenues increases our confidence,” the analyst said. “AMD Server CPU revenues should grow well over 70%+ this year as agentic deployments drive demand well ahead of prior models. While AMD just raised its x86 server CPU TAM to $120B by 2030 at a 35%+ CAGR, we actually think this estimate may be too conservative. AMD’s GPU business should benefit from new customer wins as it inflects with the MI450 ramps with OpenAI and Meta in 2H26.”

To this end, Reitzes rates AMD shares as a Buy, while his $540 price target offers 12-month upside of 21%. (To watch Reitzes’ track record, click here)

27 other analysts join Reitzes in the bull camp, while an additional 8 Holds can’t detract from a Strong Buy consensus view. However, the $461.38 average price target leaves room for only modest one-year returns of 3%. (See AMD stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.