Shares of Nvidia (NVDA) have surged more than 1,000% over the past five years, pushing the company’s market capitalization above $5 trillion. The stock remains one of Wall Street’s favorite AI pick as strong demand for its chips continues to fuel growth in data centers, cloud computing, and AI infrastructure. However, the bullish case for Nvidia is now so widely accepted that even small signs of slowing growth, rising competition, or margin pressure could trigger sharp market reactions. Here are three key risks Nvidia investors should watch closely in 2026.

Claim 55% Off TipRanks

New trading tool for AMZN bulls1. Customer Concentration Risk

One of NVDA’s biggest hidden risks is customer concentration. According to the company’s filings, just two customers accounted for 36% of FY26 revenue. That means if any of Nvidia’s largest customers decide to slow AI spending, delay infrastructure upgrades, or reduce chip orders, the company’s revenue growth could face meaningful pressure.

However, customer concentration risk does not make NVDA uninvestable. Nvidia’s CUDA software ecosystem remains one of its biggest competitive advantages, and switching away from the company’s full AI platform is not easy for customers.

But the risk does show that Nvidia is not necessarily a buy-and-forget stock. The company’s growth still heavily depends on continued AI spending from major hyperscalers and cloud companies. That means investors may need to monitor AI infrastructure spending trends, customer demand, and competitive developments closely each quarter.

2. Rising Competition in AI Chips

Competition in the AI chip market is intensifying. Rivals such as Advanced Micro Devices (AMD) and Intel (INTC) could pressure Nvidia’s market dominance over time. At the same time, major tech companies are increasingly developing their own AI chips to reduce reliance on Nvidia. Google (GOOGL) is already using newer generations of its custom TPU chips for many internal AI workloads, while Amazon (AMZN) and Meta (META) are also investing heavily in in-house AI hardware.

Investors will closely watch whether Nvidia can maintain its lead in AI hardware and software.

3. Premium Valuation Risk

Notably, NVDA currently trades at a trailing P/E ratio of 43.48, well above the semiconductor sector average of 25.1. Nvidia continues to command a premium valuation compared to many chip peers, reflecting extremely high investor expectations around AI growth.

That premium leaves the stock vulnerable to sharp pullbacks if earnings disappoint or market sentiment shifts. Even small signs of slowing revenue growth, weaker guidance, or softer AI spending trends could trigger significant volatility in NVDA shares.

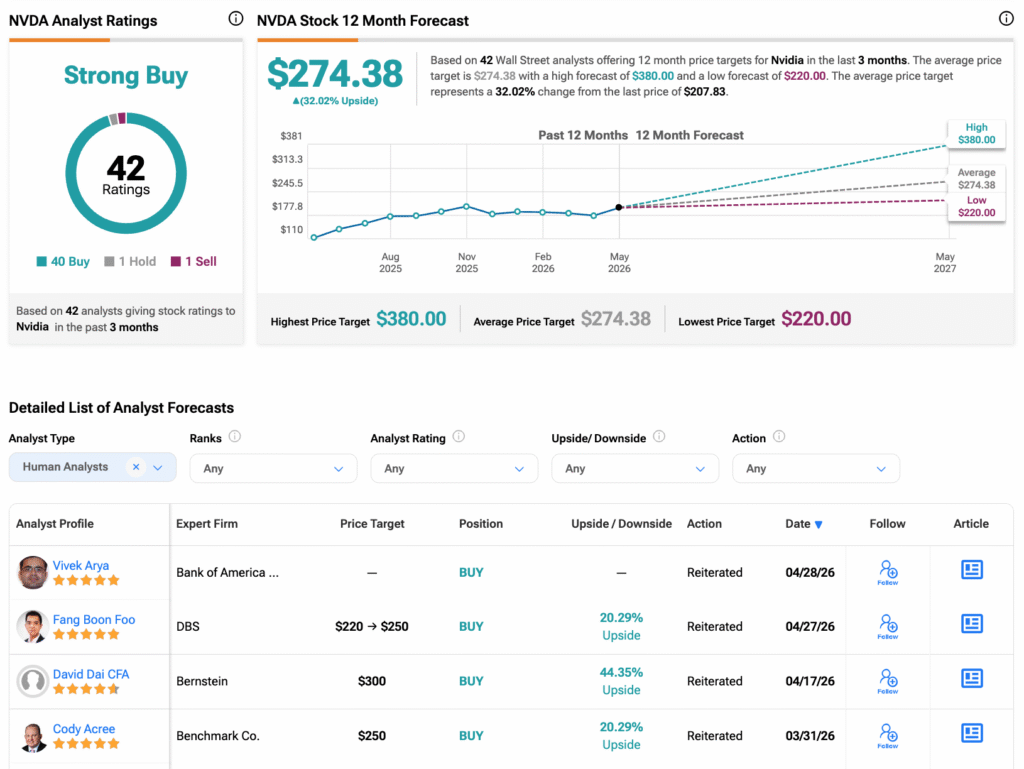

What Is Nvidia’s Stock Price Target?

Looking ahead, analysts still rate Nvidia stock as a Strong Buy, with 40 Buys, one Hold, and one Sell assigned in the last three months. At $274.38, Nvidia’s average 12-month stock price target implies an upside of over 30% from the current level.