The Q1 2026 earnings report from CoreWeave (NASDAQ:CRWV) landed with a resounding thud. Though there were many positives – including large jumps in both quarterly and year-over-year revenues – the market was none too pleased by an EPS miss.

Claim 55% Off TipRanks

Trade CRWV with leverageIndeed, the company’s ability to generate revenues isn’t the issue. CoreWeave continues to grow sales, and its $2.1 billion last quarter represented 32% sequential growth and a 112% year-over-year increase.

Moreover, the company’s revenue backlog exploded to $99.4 billion, growth of some 50% sequentially and roughly four times greater than the previous year. And, in another milestone, CoreWeave surpassed 1 gigawatt of active power, while increasing its contracted power to >3.5 gigawatts.

However, the company’s profits (or more accurately, lack thereof) bogged down sentiment. An EPS loss of -$1.11 was worse than the -$0.92 that analysts had been expecting, and CRWV was down about 11% in Friday’s trading session.

Is this a great opportunity to go dip buying? Not according to top investor Geoffrey Seiler, who worries about the company’s highly leveraged business model.

“It’s not generating a lot of cash flow to pay for its build-out, so it’s going to have to take on a lot of debt,” explains the 5-star investor, who is among the top 3% of stock pros covered by TipRanks.

Seiler draws a sharp distinction between CoreWeave and the big hyperscalers, pointing out that Alphabet, Amazon, and Microsoft are all bringing int tons of cash to fund their data center buildout. He worries that this makes CoreWeave highly vulnerable to the rising cost of GPUs and other chips, especially since its not making its own silicon.

As evidence of this dynamic, he notes that the company raised the lower end of its full-year capex guidance to $31 billion, though it did keep its high-end prediction of $35 billion intact.

Moreover, the investor notes that the company’s Q2 revenue guidance of $2.45 to $2.6 billion came in slightly lower than the $2.69 billion that the market had estimated. (Though it did keep its full-year guidance range of $12 to $13 billion untouched.)

While the sales and backlog are strong, it’s not enough to convince Seiler to take the leap.

“Overall, CoreWeave is a highly speculative stock. Its model could work as it scales, but it’s not the way I’d want to play the AI infrastructure boom,” concludes Seiler. (To watch Seiler’s track record, click here)

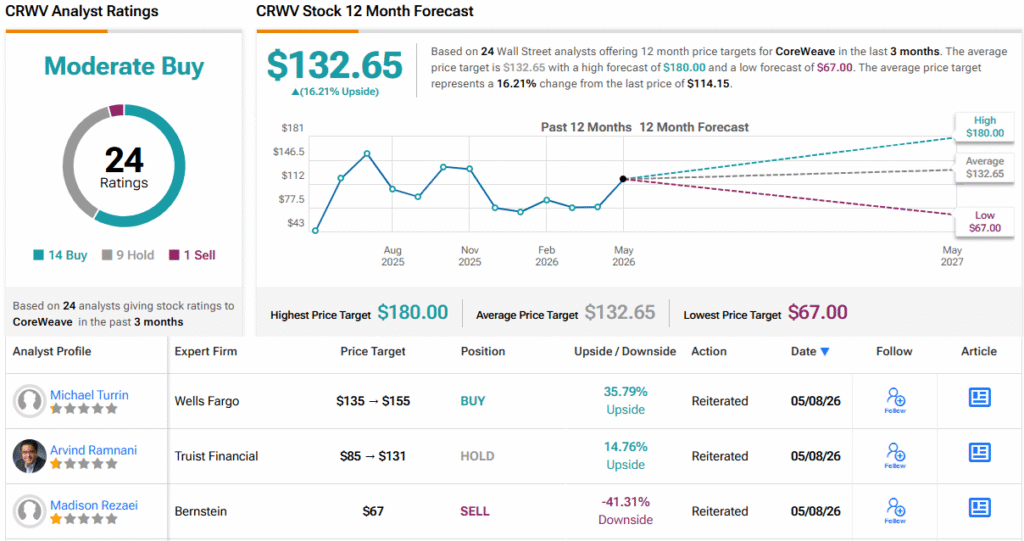

Wall Street, on the other hand, is focusing on the upside. With 14 Buys, 9 Holds, and 1 Sell, CRWV enjoys a Moderate Buy consensus rating. Its 12-month average price target of $132.65 points to an upside of 16%. (See CRWV stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.