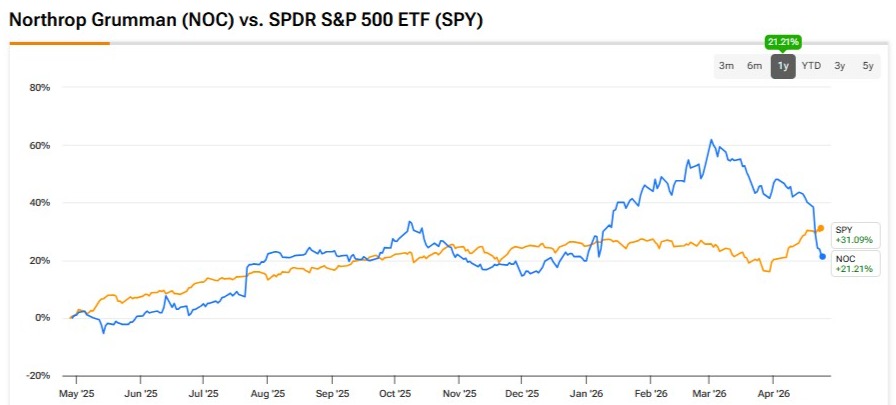

Northrop Grumman (NOC) remains a compelling buy despite its post-earnings dip, with B-21 growth continuing to strengthen the buy case. The leading aerospace and defense company’s first-quarter print on April 21 highlighted solid execution across core defense programs, even as the market focused on near-term cost pressures and increased capital spending. With the B-21 moving deeper into production, Sentinel adding long-duration visibility, and backlog staying robust, the underlying growth profile remains intact, reinforcing my bullish stance on the stock.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The B-21 Halo and the First-Quarter Beat

Northrop’s numbers this past week suggest the business is starting to deliver the payoff from significant earlier work. Q1 adjusted earnings per share (EPS) came in at $6.14 versus $6.03 expected, and revenue rose 4% to $9.88 billion. However, the real standout was Aeronautics, where sales climbed 17%, largely powered by the B-21 entering low-rate initial production.

Management said margins in Aeronautics recovered to 9.3%, helped in part by not having to deal with the loss charges that had dragged things down in early 2025. So the improvement is not just about revenue picking up. The profitability is starting to look healthier, too.

It is not only the bomber story driving that. Defense Systems also grew sales 5%, with the Sentinel program continuing to ramp at a strong pace. On the call, Kathy Warden also made clear that Northrop has reached an agreement with the Air Force to expand annual B-21 production capacity by 25%. That is a meaningful signal. When the Pentagon wants more output and wants it faster, that usually tells you demand is not going away anytime soon. For Northrop, it adds even more visibility to a business that already has a long runway.

The sum of the Q1 report, for me, is that it reflects a company transitioning from “development risk” to “production rewards.” While Mission Systems’ top line stayed relatively flat, its operating income rose 20% due to favorable contract adjustments. This tells me that Northrop is getting better at managing its complex portfolio even as the macro environment remains unpredictable. The investment case remains robust because Northrop is moving to sell high-end technology, integrated battle command systems, and advanced radar, which enable the rest of the military to operate in modern conflicts.

A Backlog Built for a Volatile Era

To get a sense of why Northrop is positioned for stable, predictable success over the medium term, just look at its backlog. It is sitting at $96 billion, giving the company significant built-in visibility. That is not just a healthy order book. It is 2–3 years of work already lined up. What’s also noteworthy is how management is responding to that demand. Warden said the company plans to put $2.5 billion of its own capital into B-21 facilities through 2029.

Some investors get nervous when they hear “higher capex,” but in a business like this, it usually means demand is strong enough that the company needs more capacity to keep up.

The broader backdrop is doing a lot to support the defense story right now. Governments are treating defense spending more like something they cannot afford to get wrong. That shift is key for companies like Northrop because it means demand is being driven by long-term strategic priorities. Northrop is in a strong spot within that environment. It is already tied to critical programs, and it is also moving into areas where capacity is still tight, like solid rocket motors, which could pay off big because it puts the company closer to one of the real bottlenecks in the missile supply chain.

In addition, Northrop’s growth story is getting broader. Beyond the headline programs like the B-21 or Sentinel, the weapons business is becoming a more meaningful piece of the company, and it is growing faster than the rest of the portfolio. That is important because demand for munitions and tactical rocket motors still looks strong and likely to stay that way. Management’s decision to open more than 20 new facilities in the last two years makes it pretty clear they are building for that demand in a serious way.

Price Is What You Pay, Value Is What You Get

So, why did the stock take a breather after the report? It might be that investors disliked the $200 million hike in 2026 capex or the $71 million unfavorable adjustment in the Space segment related to the Graphite Epoxy Motor (GEM) 63XL program. There could also be some simple profit-taking happening after the stock’s impressive rally over the last couple of years. Yet, I feel this dip is an overreaction.

When you do the math, Northrop stock isn’t expensive at these levels. It is currently trading at just under 21x the 2026 consensus EPS estimate of $27.93. Now, if you look at the history books, that’s admittedly a bit higher than the mid-to-high teens multiple we saw in the late 2010s. However, we aren’t in the late 2010s anymore. We are in an era when earnings are expected to grow in the mid-single-digit to low-double-digit range for the foreseeable future.

A 21x multiple for the world’s premier stealth and nuclear modernization firm, in a world that is desperately seeking security, is a fair price, if not a bargain.

The “margin of safety” here comes from the visibility of the cash flow. With the backlog at $96 billion and the B-21 production rate officially accelerating, the risk of a medium-term earnings “miss” is low. We are looking at a company that is essentially a utility for the Pentagon, but one with the growth profile of a high-end tech firm. To me, the post-earnings pullback is just a chance for long-term investors to get in before the market fully prices in the multi-decade ramp of the B-21 and Sentinel programs.

Is NOC Stock a Buy, Sell, or Hold?

Despite the stock’s post-earnings decline, Northrop Grumman still has a Moderate Buy consensus rating on Wall Street, based on 10 Buy and five Hold ratings. Notably, no analyst rates the stock a Sell. Further, NOC’s average price target of $743.33 implies nearly 29% upside potential over the next 12 months.

Conclusion

Northrop is proving it can handle some of the world’s most demanding programs without sacrificing its growth and innovation capabilities. With a $96 billion backlog and a 25% increase in B-21 production capacity, the path ahead looks pretty clear. At roughly 21x earnings, that still looks reasonable for a business with this much visibility and momentum.