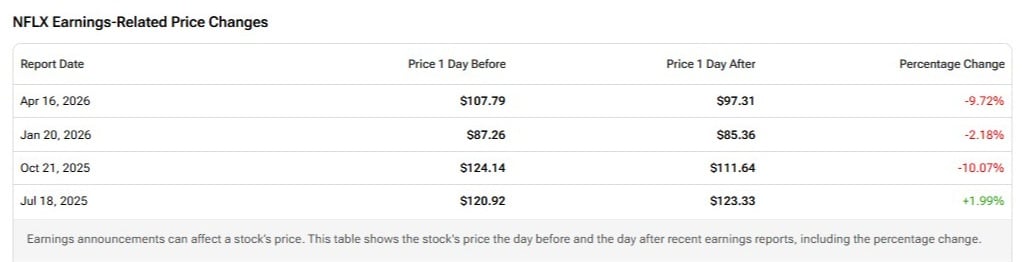

Netflix’s (NFLX) soft first-half setup may be creating a stronger second-half opportunity. Shares are down roughly 9% since the company’s mid-April earnings release, as investors reacted to a narrow Q1 beat, softer-than-expected guidance, and lingering concerns around pricing dynamics in Europe. The pullback also reflects broader uncertainty in the streaming sector, where competition, content spending, and the evolving role of artificial intelligence (AI) continue to shape investor sentiment.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

That said, I think the market may be focusing too much on the near-term noise. Netflix remains the global leader in streaming, with unmatched scale, a deep content library, and a growing ability to monetize its user base beyond subscriptions. While the first half of 2026 may look somewhat muted due to timing factors — such as content amortization and the ramp of newer initiatives — the underlying fundamentals remain intact. I reiterate my bullish stance on the stock.

Q1 Was Not Bad, but Expectations Were High

Netflix’s Q1 results were solid, though not strong enough for a stock that had high expectations heading into the print. Revenue grew 16% year-over-year to $12.25 billion, slightly ahead of consensus and company guidance. Operating income came in at $3.96 billion, with an operating margin of 32.3%, up 60 basis points year-over-year.

The issue was guidance. Netflix guided Q2 revenue to $12.57 billion, up 13% year-over-year, slightly below prior expectations. Management also noted that Q2 will likely mark the peak year-over-year content amortization growth rate for 2026, before that pressure eases in the second half.

That matters because Netflix reiterated its full-year revenue outlook of $50.7 billion to $51.7 billion and operating margin guidance of 31.5%. In other words, the company is still pointing to a stronger back half.

Advertising Could Become a Bigger Growth Driver

The advertising business remains one of the most important parts of the bull case. Netflix expects ad revenue to roughly double to about $3 billion in 2026 after growing around 150% last year.

The early signs are encouraging. The ad‑supported tier represented more than 60% of new subscriptions in Q1 across countries where the plan is available. Netflix also said its advertiser count rose 70% year-over-year to more than 4,000 clients.

This business is still early. Over time, Netflix can improve targeting, use AI to strengthen ad products, expand partnerships, and add more live or event-driven content. That could make advertising a larger and more profitable revenue stream in 2027 and beyond.

Price Increases Still Look Supportive

Netflix’s ability to raise prices remains a major advantage. Recent U.S. price increases could add meaningfully to 2026 revenue, and survey data suggest churn risk remains manageable.

Several recent surveys suggest that only a small, single‑digit percentage of Netflix subscribers plan to cancel in the near term, with a large majority planning to keep their subscription and a modest share considering tier changes. This supports the idea that Netflix’s content depth and user habits remain strong.

Europe is a risk, as resistance to price increases and legal challenges could create some overhang. However, Netflix’s domestic pricing power and global scale still give it more flexibility than most media companies.

Free Cash Flow and Buybacks Add Support

Netflix also raised its 2026 free cash flow guidance to $12.5 billion from $11 billion. That is a major improvement and gives the company more room to invest in content, improve its ad stack, and return capital.

On April 22, Netflix authorized an additional $25 billion share repurchase program. This comes on top of the $6.8 billion still available under its prior authorization as of March 31.

That buyback support is important after the recent pullback. If Netflix continues to generate strong free cash flow, repurchases could become a meaningful driver of earnings per share.

Valuation Is Not Cheap, but Quality Deserves a Premium

Netflix is not a cheap stock on traditional valuation metrics. It trades at a P/E ratio of about 30x, above the sector median of around 14. Its price-to-operating-cash-flow ratio is about 30.7, far above the sector median of roughly 9.

Still, I do not think traditional metrics tell the full story. Netflix is the clear global streaming leader, has industry-leading engagement, strong pricing power, improving ad monetization, and rising free cash flow. It is also one of the few media companies with real scale, global distribution, and a proven ability to monetize content more efficiently than peers.

Wall Street’s View

According to TipRanks, Netflix has a Strong Buy consensus rating, with 27 Buy, seven Hold, and no Sell ratings. Based on 34 Wall Street analysts, the average 12-month price target is $116.06, implying 32.05% upside from the last price of $87.89.

Conclusion

Netflix’s Q1 report did not fully satisfy investors, and Q2 guidance looked soft. However, the full-year outlook still implies a stronger second half, supported by pricing, advertising growth, content timing, and stronger free cash flow.

With shares down about 9% since earnings, I think the pullback creates an attractive opportunity. Netflix remains a dominant streaming platform with multiple growth levers, and I am bullish on NFLX.