Software stocks are catching a lift today after Atlassian delivered a stronger-than-expected earnings report, giving the battered SaaS group a reason to bounce after weeks of heavy selling pressure. The upbeat results, along with encouraging guidance, are helping ease concerns that demand across enterprise software is falling off a cliff, at least for now.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Those concerns have been building around the rapid advance of generative AI and its potential to upend traditional software models. As these tools improve at turning natural language into working code, investors are questioning whether the long-term need for a wide range of standalone SaaS applications could diminish, leaving parts of the industry more exposed than previously assumed.

That idea has led to growing talk of a so-called “SaaSpocalypse,” a scenario in which enterprise customers move away from paying for numerous subscriptions and instead rely on AI platforms capable of handling a wide range of tasks within a single interface.

However, Morgan Stanley analyst Elizabeth Porter sees some light at the end of the tunnel for the sector, pointing to early signs that investors are starting to differentiate between companies that face higher disruption risk and those that can adapt and integrate AI into their offerings.

“Against increasingly bearish investor sentiment, intra-quarter data points – both channel conversations and CIO survey indicators – reflected durability / signs of cautious optimism within fundamentals, as: 1) Partners cited in-line / modestly ahead quarters, pointing to durability in core tailwinds like platform consolidation and increased demand for differentiated content and marketing strategies amidst AI diffusion; while 2) our CIO survey points to modest acceleration in Software budgets in 2026, with application vendors continuing to screen as key vendors used to operationalize AI technologies,” Elizabeth noted.

Porter looks ahead and adds, “With material estimate revisions and / or accelerating toplines needed to prove out the broad-based bull case on the group and give shares support (as evidenced by pressure in application bellwether NOW), we remain selective on what can work in Q1.”

Against this backdrop, Porter highlights two beaten-down SaaS stocks she believes are worth buying. Do other analysts see it the same way? We turned to the TipRanks database for answers. Here are the details.

Klaviyo, Inc. (KVYO)

Boston-based Klaviyo, the first software stock we’ll look at here, focuses on marketing automation. The company’s expertise is business-to-customer CRM, and its subscription-based Klaviyo Data Platform brings AI insights to bear on data analytics and customer service, so that businesses can better understand their own customers – and create more effective, better-targeted, and better-branded direct marketing efforts.

Klaviyo has adopted agentic AI technology to offer users automated agents that can see a customer’s full picture – everything from purchase history to real-time account behavior. The result is a chatbot that is capable of doing more than just answering questions; it can recommend products that the customer actually wants to buy, help the user make the purchase, and keep the conversation moving no matter when the customer makes contact.

Klayvio’s AI-powered helpdesk provides a comprehensive service, based on quick access to every contact the customer has had with the vendor, including marketing engagements and loyalty status. When a human contact is needed, the AI chat agent can provide a seamless handoff, providing contact context and history for efficient resolutions.

All of this has made Klaviyo a popular choice for e-commerce vendors and direct marketers. The company has over 193,000 customers as of the end of last year and saw 30% year-over-year revenue growth in 4Q25.

At the same time, the company is registering solid growth. As noted, Q4 revenue showed a strong year-over-year gain; quarterly revenue, at $350.2 million, beat the forecast by $16.22 million. The bottom line, reported as a non-GAAP EPS of $0.19, was 2 cents per share better than had been expected. These results were driven by a 15.5% year-over-year increase in the company’s year-end customer count.

Still, the stock has not been immune to the broader pressure across software names and is down 38% year to date.

Looking ahead, Morgan Stanley analyst Porter argues that Klaviyo’s underlying business strength provides a solid base for future gains, suggesting the recent weakness may not fully reflect the company’s longer-term potential.

“[The] recent multiple compression appears increasingly disconnected from the durability of the business, with strength across international, upmarket, and multiproduct adoption reinforcing a long runway for sustained growth. FY26 guidance appears conservative, particularly with minimal assumed contribution from newer AI and Service initiatives, setting up room for Q1 upside and forward estimate revisions as adoption ramps. Importantly, we see Klaviyo management leaning aggressively into agentic customer experiences, well exhibiting commitment to the pace of innovation in the technology landscape,” Porter commented.

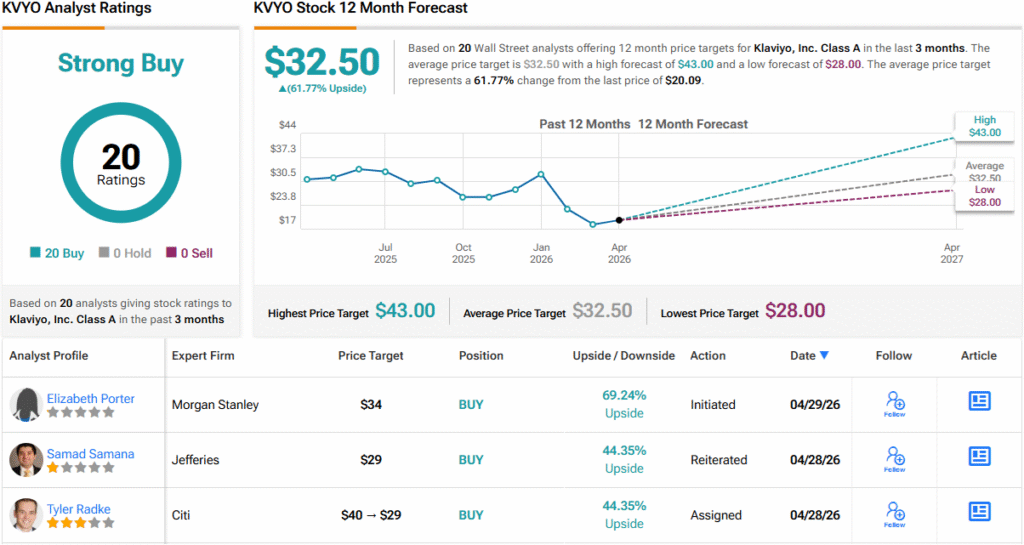

Based on this stance, Porter rates KVYO shares as Overweight (i.e., Buy), with a $34 price target that indicates room for a 69% upside in the coming 12 months. (To watch Porter’s track record, click here)

That’s broadly in line with the analyst consensus on Klaviyo, whose Strong Buy consensus rating is based on 20 unanimously positive recent recommendations. The shares are selling for $20.09, and the $32.50 average price target implies a ~62% one-year upside potential. (See KVYO stock forecast)

HubSpot, Inc. (HUBS)

HubSpot, the second stock under Morgan Stanley’s radar, has quietly become a force in marketing software, with its cloud-based platform serving as a go-to solution for businesses looking to manage customer relationships, content, and digital campaigns in one place. Since its founding in 2006, the company has expanded well beyond basic marketing tools, offering an integrated suite that helps teams handle everything from CRM and social media to SEO and content management, making it a core platform for marketers, customer service teams, and inbound sales operations alike.

A key point in HubSpot’s success has been its bent toward innovation. The company has built a toolset that can be automated to simplify a wide variety of marketing functions, including ad placement, newsletter builds, content publishing, and chatbot development. HubSpot has brought AI tech to all of these through its Breeze AI digital assistant.

More recently, HubSpot has been making use of the newer agentic AI tech, providing apps that let its enterprise customers build and modify more ‘personalized’ AI tools. HubSpot’s AI system brings features and agents for prospecting, closing, data management, and customer experience personalization – all to give enterprise users greater flexibility when it comes to designing an online marketing approach. From a client perspective, HubSpot provides the tools that let AI handle busy work while humans focus on decision-making and data management.

HubSpot has always operated on the freemium model, providing a basic level of service for free account users, with more advanced features, tools, and upgrades available for paid subscribers. The company has tightened restrictions on its ‘free forever’ basic CRM account – but that base level remains accessible. The freemium model is, in effect, its own advertising and has proven successful in many online subscription fields.

This company will release its next financial results for 1Q26 next Tuesday (May 5); for now, we can look at the 4Q25 results to get an idea of where the company stands. In Q4, HubSpot brought in quarterly revenue of $846.7 million, up 20% year-over-year and $16 million better than had been anticipated. The revenue total included a 21% year-over-year gain in subscription revenue, which reached $829 million. The company’s bottom line, of $3.09 per share in non-GAAP measures, beat the forecast by a dime.

Even though HubSpot has proven successful long-term, and continues to generate sound revenues and earnings, the company has not been immune to the ‘SaaSpocalypse’ sell-off or the worries that the spread of AI will cut into its market share. HUBS shares have fallen by ~64% in the past 12 months, as those worries have gained steam.

Once again, we’ll check in with Elizabeth Porter, who takes a bullish view here, writing of HubSpot: “Leading indicators continue to represent momentum in underlying demand at HubSpot, with Net New ARR growth exceeding CC revenue growth in every quarter of 2025, and full-year NN ARR growing 24% YoY, materially above 18% CC revenue growth. Our checks on the quarter continued to reinforce the durability of HubSpot’s core growth drivers, competitive positioning, as well as ramping adoption of AI initiatives – however, AI adoption (and monetization) remains somewhat measured… Remain OW HUBS with shares trading at 0.14x EV / S / G (vs SMid peers at 0.28x), though expect acceleration and revisions catalysts needed to re-rate shares more likely to materialize in the 2H.”

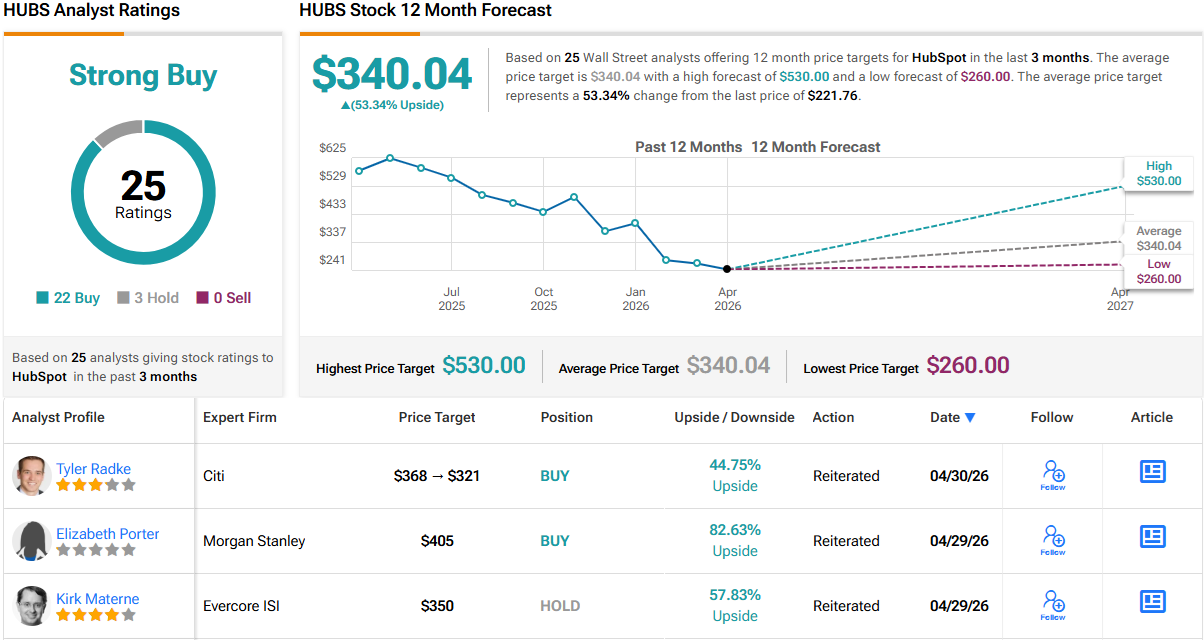

To this end, Porter assigns HUBS shares an Overweight (i.e., Buy) rating, and a $405 price target that suggests the share will gain ~83% on the one-year horizon.

All in all, HubSpot has a Strong Buy consensus rating on Wall Street, based on 25 reviews that break down to 22 Buys and 3 Holds. The stock is selling for $221.76, and its average target price, $340.04, implies an upside of 53% by this time next year. (See HUBS stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.