Despite the pandemic-spurred profits, Etsy (ETSY) has faced a rough patch recently, with the stock taking a significant hit, declining over 69% in the past three years. While the company is trying to revamp its image via policy updates and operational efficiency, its comparison to competitors like Amazon (AMZN) and Walmart (WMT) reveals the depth of the challenges Etsy is facing in maintaining its market positioning.

Claim 30% Off TipRanks

New trading tool for AMZN bullsHowever, the company recently announced it beat revenue expectations for Q2, suggesting it is making progress. Investors may want to continue to watch the company’s progress for further confirmation of success before taking action on the stock.

Etsy’s Platform of Services

Etsy is a comprehensive online marketplace operating in the United States, Canada, the UK, France, Germany, and Australia. The company is known for its focus on unique, handmade, or vintage items and craft supplies, such as jewelry, clothing, bags, toys, art, home decor, and furniture.

Etsy has implemented measures to safeguard buyers through the Etsy Purchase Protection program. This company offers the Etsy Share and Save program, where sellers can save on Etsy fees for sales driven to their Etsy shop from their own channels. The company also operates other platforms, such as Reverb for musical instruments, Depop for fashion resale, and Elo7, which caters to the Brazilian market.

Etsy’s Recent Financial Results & Outlook

The company recently announced its financial performance for the second quarter. Sales increased 3% year-over-year, reaching $647.8 million, higher than analysts’ projections of $629.2 million. The surge in revenue is credited primarily to the growth in payments and transaction fee revenue from Offsite Ads. However, consolidated gross merchandise sales (GMS) decreased by 2.1%, and ETSY marketplace GMS decreased by 3.2%.

The total net income was $53.0 million, a decrease of $8.9 million year-over-year, mainly due to a $7.2 million retroactive non-income tax expense. Consequently, the net income margin was approximately 8.2%, and the earnings per share (EPS) stood at $0.41, slightly less than the analysts’ prediction of $0.44 per share.

The company ended the quarter with $1.1 billion in cash and investments. Under Etsy’s stock repurchase program, the company repurchased approximately $150 million, or 2.4 million shares, of its common stock.

Management has issued Q3 2024 financial guidance, with consolidated GMS projected to decline by a low single-digit percentage year-over-year. The Take Rate is expected to mirror Q2 2024’s performance. The Adjusted EBITDA Margin is forecasted at approximately 27%. As for the full-year outlook for 2024, the consolidated adjusted EBITDA margin is anticipated to match or surpass the 2023 results.

What Is the Price Target for ETSY Stock?

The stock is volatile, sporting a beta of 1.54, and has been on a downward trajectory, shedding 31% year-to-date. It trades at the low end of its 52-week price range of $55.08 – $89.58 and shows negative price momentum, trading below its 20-day (61.55) and 50-day (61.90) moving averages. With a P/E ratio of 25.8x, the stock trades at a relative discount to peers in the Internet Retail industry, with an average P/E of 30.37x.

Analysts covering the company have taken a cautious stance on the stock. Oppenheimer analyst Jason Helfstein, a five-star analyst according to Tipranks’ ratings, recently downgraded Etsy to Perform from Outperform, noting a lack of catalysts and weaker Q3 guidance.

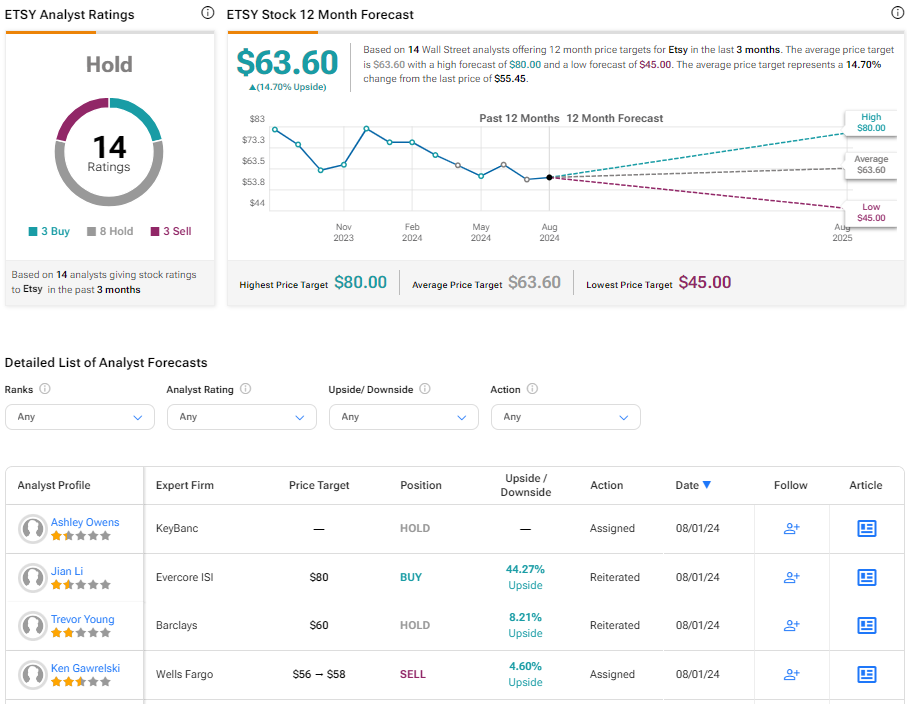

Based on the recommendations and price targets assigned by 14 analysts, Etsy is rated a Hold overall. The average price target for ETSY stock is $63.60, representing a potential 14.70% upside from current levels.

ETSY in Summary

In a challenging market, Etsy finds itself battling to maintain its position. Despite seeing a substantial decline in stock value over the past three years, recent updates suggest it is charting a path forward. Q2 results beat revenue expectations, hinting at a potential turnaround. However, the recent performance also showed a decrease in gross merchandise sales (GMS) and lower than predicted earnings per share (EPS), showing there is still ground to cover.

In conclusion, investors should monitor Etsy’s ongoing efforts to revamp its image and operations to see if there are further signs of progress.