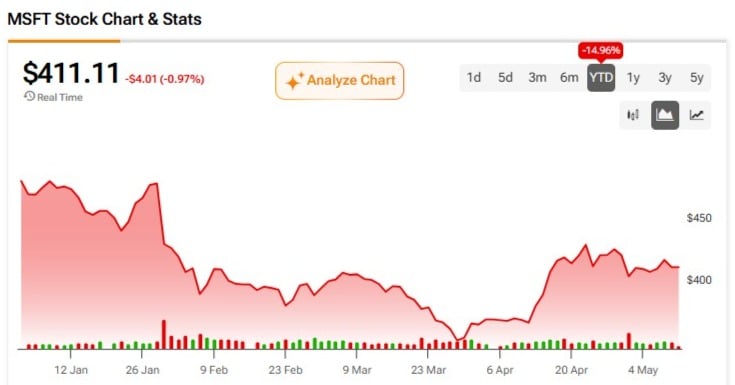

Microsoft’s (MSFT) Q3 report suggests the company’s long-term artificial intelligence (AI) thesis may actually be getting stronger beneath the surface, with yet another round of robust results posted on April 29. The company’s shares are still down roughly 14% year-to-date. However, I believe the more important takeaways from the latest earnings report were far more subtle than the headline numbers alone suggest. For me, beyond simply delivering a beat across the board in Q3, the quarter highlighted three key points.

Claim 55% Off TipRanks

New trading tool for AMZN bullsCopilot is becoming much more than just another seat-based software product. Meanwhile, AI infrastructure efficiency appears to be improving, which could support margins over time. Azure’s AI story also looks increasingly less dependent on OpenAI exclusivity than many investors may have previously assumed.

Microsoft currently trades at more de-risked valuations around 25x trailing P/E — roughly 25% below its five-year average. At the same time, the combination of these three factors suggests the Big Tech giant is quietly building the infrastructure, software layer, and enterprise workflow platform for long-term AI monetization. In my view, that continues to reinforce the bullish thesis for the stock.

Copilot Is Becoming More than a Seat-Based Business

Perhaps one of the most important and least obvious points from Microsoft’s recent earnings results relates to its monetization model. Historically, Microsoft primarily generated revenue through user-based subscription products, such as Office licenses assigned to each employee within a company. In that setup, more users essentially meant more revenue.

Now, with the advancement of AI, Microsoft appears to be building something with Copilot that looks much more similar to Azure. Beyond the fixed license fee, customers can increasingly pay based on usage — whether through agents, automation, processing, workflows, or broader AI consumption.

During the most recent earnings call, CEO Satya Nadella repeatedly emphasized a shift from a per-user business model to a per-user plus usage-based model. In other words, Microsoft is trying to transform traditionally seat-based businesses into models with a growing consumption layer on top. This could drive Average Revenue per User (ARPU) growth far more meaningfully than the market may currently anticipate.

How Is Copilot Influencing the Balance Sheet?

To get a sense of the potential impact on Microsoft’s P&L, the company already reports more than 20 million Microsoft 365 Copilot paid seats, with a list price of roughly $30 per month. On a rough basis, that would imply around $7.2 billion in annualized revenue. Not all customers pay the full list price due to enterprise discounts, bundles, and pricing dynamics. Because of that, I believe that assuming an Annual Recurring Revenue (ARR) of about $5.5 billion to $7 billion for M365 Copilot alone is more realistic.

Although this still represents only around 2% of Microsoft’s total revenue today, the more important point is the economic mix and where this could be heading. Copilot seats grew 250% year-over-year, while consumption credits nearly doubled quarter-over-quarter. At the same time, Microsoft continues to push deeper into agents, workflows, and usage-based monetization.

If Microsoft 365 is indeed becoming the operational interface for enterprise AI, it would not be unreasonable to eventually see Copilot scale to 50–100 million seats. Combined with ARPU expansion and improved inference efficiency, this could translate into an additional $20–30 billion in AI productivity revenue per year. That would make Copilot a much more meaningful part of Microsoft’s overall business.

AI Infrastructure Is Becoming Economically More Efficient

Much of the skepticism surrounding Microsoft shares this year has stemmed from the market’s perception that the company is “burning through” money on AI infrastructure. The concern is whether those investments will ultimately generate a proportional return. However, the Redmond-based company showed some early signs in its Q3 results that the story is starting to improve. Beyond simply expanding capacity, Microsoft also appears to be improving the economic efficiency of that capacity.

Microsoft showed that the unit cost of AI is starting to fall. The company reported a 40% improvement in inference throughput, or the amount of AI work processed by its infrastructure. This means that Microsoft can now generate roughly 40% more output with essentially the same capex base — graphics processing units (GPUs), power, and hardware.

The impact of this eventually shows up in margins. Every time a user interacts with Copilot or AI agents, Microsoft incurs compute costs. So if the company can process more AI workloads with the same GPU base, margins can improve meaningfully over time. Despite the massive AI investment cycle, recent results are already beginning to reflect some of that operating leverage. In Q3, gross margins came in at 67.6%, only slightly below the 68.7% reported a year earlier, while operating margins increased year-over-year from around 45% to 46%.

What is even more interesting is that some segments directly exposed to Copilot’s growth also showed margin resilience. In Productivity & Business Processes, for example, operating income grew 21% year-over-year, while gross margin percentage increased slightly despite higher investments in AI infrastructure to support the continued growth in Microsoft 365 Copilot seats and usage.

Azure’s AI Growth Is Becoming Less Dependent on OpenAI

Another subtle takeaway from Microsoft’s latest earnings report concerns Azure. Here, the bull case for the cloud business is becoming more solid because Microsoft appears to be getting less reliant on OpenAI to justify its AI growth. Arguably, a meaningful part of the risk surrounding Microsoft has stemmed from the idea that large portions of its AI momentum were too closely tied to OpenAI workloads and Azure exclusivity.

For example, in Q3, commercial bookings declined 4% year-over-year, including OpenAI. However, excluding OpenAI, bookings actually grew 7% year-over-year. This suggests Microsoft’s core commercial demand remains very healthy even after stripping out the OpenAI impact.

There have been recent changes to the OpenAI agreement. The end of exclusivity could be somewhat negative for Azure in the short term. However, it also reduces Microsoft’s dependency risk. The company still benefits from OpenAI through revenue sharing until 2030, royalty-free IP access until 2032, and its equity exposure. At the same time, Azure no longer needs to be viewed solely through the lens of OpenAI demand.

Ultimately, this matters because if Azure continues growing strongly even as OpenAI diversifies across Amazon Web Services (AMZN) and Google Cloud (GOOGL), Microsoft’s AI cloud thesis becomes much more durable.

Is MSFT a Buy, According to Wall Street Analysts?

The consensus rating for MSFT is Strong Buy, based on ratings from 35 Wall Street analysts over the past three months. Of those, 33 analysts rate the stock as a Buy, while only two maintain Hold ratings. The average price target currently stands at $559.98, implying potential upside of roughly 36.1% from the current share price.

The AI Thesis Looks Increasingly Durable

Microsoft’s latest quarter reinforced my bullish view on the company’s long-term positioning in AI. Copilot is starting to look much more like a consumption-driven platform rather than just another software subscription. At the same time, AI infrastructure efficiency appears to be improving faster than the market arguably expected, while Azure’s growth is becoming increasingly less dependent on OpenAI exclusivity, which I view as very healthy for the long-term cloud thesis.

Combined with Microsoft’s still-strong margins, double-digit growth, and valuation multiples below historical averages, MSFT currently appears to be one of the most underappreciated long-term AI plays in the market.