Micron (MU) stock is up about 31% for the year after delivering strong financial results, positive surprises, and strong executions throughout 2024. It’s still trading at an attractive multiple, and there’s a lot to look forward to with Micron, especially in AI. In this article, I will lay out the thesis for why MU stock might be the best long-term AI stock that’s currently on sale.

Meet Samuel – Your Personal Investing Prophet

200% short exposure to NVDA with NVDSMicron makes memory products for smartphones and PCs. Its products include dynamic random-access memory (DRAM), flash memory, and solid-state drives. Micron is a leader in its industry and continuously wins market share.

As was the case in September, I am still bullish on Micron stock and see this company delivering material capital appreciation in the long term. Apart from the attractive discount it’s offering investors right now, I like Micron’s dominant position, strong executions, and AI-related potential.

Micron Continues to Execute Strongly

Central to my thesis are Micron’s strong executions and continued winning streak. The company reported results for the Fiscal fourth quarter and full year of 2024 on September 25. Its sales grew by 93% during the quarter to $7.75 billion, and its earnings per share came in at $1.18, ahead of the Street estimates by $0.07. It’s clearly winning market share. Its main competitors in the DRAM market, Samsung (SMSN) and SK Hynix, have a higher market share. However, Micron is working on closing the gap.

What particularly caught my attention was Micron’s progress with HBM or high-bandwidth memory. HBM chips are DRAM chips stacked together to allow more data to flow through different components in a time and energy-efficient manner. Currently, Samsung and SK Hynix are the leading players for these chips. Nevertheless, I was very pleased when Micron said its HBM chips sold out through 2025.

According to data from Depend, SK Hynix, Samsung, and Micron’s HBM market share currently stands at 49%, 46%, and 5%, respectively. According to media reports and management’s commentary, Micron is gunning for a 20%-25% HBM market share in 2025. Clearly, the company is not shying away from competition. Instead, it’s improving its products, like its HBM3E 12-high, 36-gigabyte chip, which delivers 20% power savings over competitor chips.

Micron’s AI Potential Should Not Be Ignored

My bull case for Micron is centered around its AI potential, which should not be ignored. Building on the HBM discussion above, the company expects the HBM total addressable market (TAM) to grow from $4 billion in 2023 to $25 billion in 2025. Also worth noting is MU’s management, which remains committed to maintaining time-to-market and technological prowess with its HBM4 and HBM4E products. The company started shipping HBM3E chips to its AI customers in FQ4 2024.

Additionally, management said it expects to ramp up the production of its HBM3E chips in early 2025 and increase shipments of these chips throughout the year. Micron remains optimistic about 2025 and 2026 and expects a more diversified revenue stream from HBM, as the company has already become a preferred supplier of several HBM clients. It didn’t surprise me when management said its HBM chips are sold out, given that the demand for Nvidia’s (NVDA) Blackwell chips is “insane,” and yes, HBM chips are used in those.

Moreover, the AI PC market is also important to observe, and Micron is winning there, too. Micron’s AI PC chips offer more power savings, higher performance, and more space savings. Management said the company’s LPCAMM2 chips, which offer power savings and better performance, are the preferred product of multiple PC manufacturers. The company also launched new DDR5 chips on October 15, specifically for AI computing, two times faster than the predecessor DDR4 chips.

Micron Stock Is on Sale

Despite showing many promises that warrant a premium, Micron is still on sale. That is good news for people paying attention to this stock and believing in its long-term potential. MU stock is currently trading at 12 times its 2025 earnings estimate, and analysts on Wall Street expect its earnings to grow by ~ 584% in 2025.

Micron’s core business was supplying memory products for PCs, smartphones, and cars, so it had a lot of exposure to the consumer. Now, it’s involved on the enterprise side of things, and I don’t believe that when people pause buying a new car or a phone, it would severely impact Micron’s profits. Maybe Micron can deliver consistent profits as it becomes more popular with data center clients.

While I will not assume a multiple or a growth rate for Micron here, I do believe its AI stream is promising and see the company delivering consistent bottom-line growth in the long term.

Analysts’ Take on MU Stock

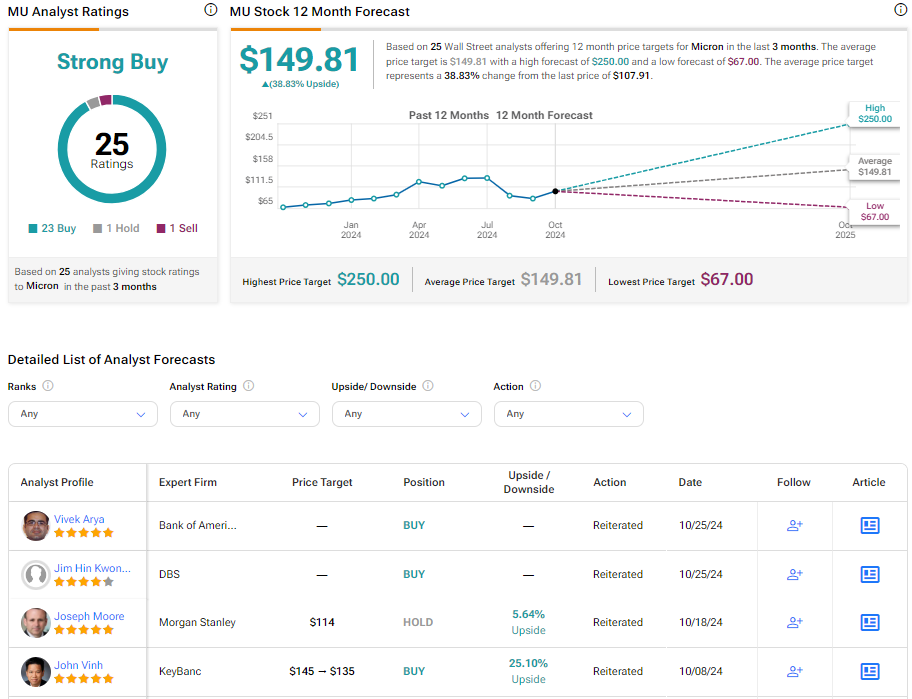

On the Street, MU stock sports a consensus Strong Buy rating based on 23 Buy, 1 Hold, and 1 Sell recommendation. The average price target of $149.81 represents an upside of 38.83% from current levels.

The Takeaway

Micron’s AI story is just starting, and the stock is still cheap. Its application space and TAM are expanding, and it’s committed to one-upping competitors. It’s constantly working on newer technology that offers power savings and higher performance in smaller chips. As the company continues prioritizing being among the first to market with the most innovative chips, it can grow its market share and capitalize on strong demand from AI and HPC applications. The stock is a winner, but investors will have to be patient.