Semiconductor firm Micron (MU) has become one of the biggest drivers of earnings estimate changes in the market. In fact, according to investment firm Goldman Sachs (GS), Micron alone accounts for about 51% of all EPS revisions in the S&P 500 (SPY) since the war with Iran began. This shift is largely due to strong demand for semiconductors, especially as spending on AI infrastructure and defense technology continues to rise.

Claim 55% Off TipRanks

Forget margin or options. Here's how the pros trade SPYIt’s also worth mentioning that the changes are unusually large. More precisely, Micron’s expected EPS growth for 2026 is now around 605% after its estimates were raised by 93%. As a result, Goldman Sachs has highlighted Micron as a key name to watch ahead of its earnings report, with its own estimates sitting about 19% above the broader consensus. This shows how quickly sentiment has shifted as stronger demand became more visible.

However, most of the remaining EPS revisions are coming from energy companies rather than tech. For instance, Exxon Mobil (XOM) and Chevron (CVX) together account for about 24% of the index’s revisions due to higher oil prices. In addition, Occidental Petroleum (OXY) posted the largest individual increase at 251%, although its overall impact is smaller due to its size. At the same time, companies like ConocoPhillips (COP), Valero Energy (VLO), and EOG Resources (EOG) have also contributed meaningfully.

Is MU a Good Stock to Buy?

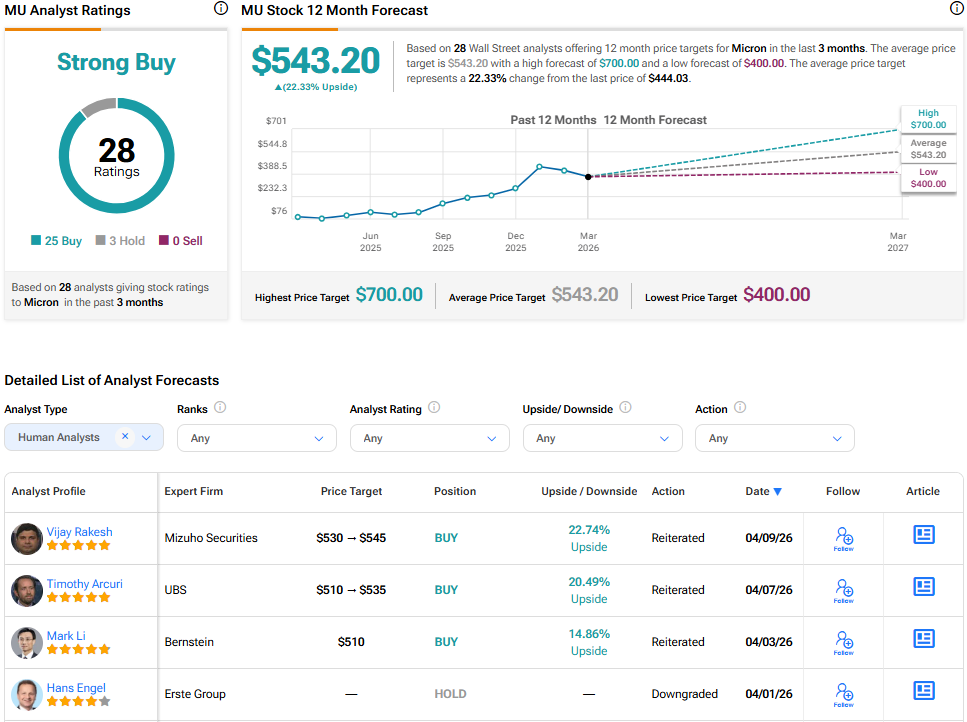

Turning to Wall Street, analysts have a Strong Buy consensus rating on MU stock based on 25 Buys, two Holds, and zero Sells assigned in the past three months, as indicated by the graphic below. Furthermore, the average MU price target of $543.20 per share implies 22.3% upside potential.