Marvell Technology (MRVL) stock soared about 6% on Wednesday, as top Wells Fargo analyst Aaron Rakers increased his price target for MRVL stock to $195 from $135 and reiterated a Buy rating, saying, “Significant AWS Trainium Expansion Ahead.” Also, 5-star rated Oppenheimer analyst Rick Schafer raised his price target for MRVL stock to $200 from $170 while reaffirming a Buy rating ahead of the semiconductor company’s Q1 FY27 earnings on May 27. Schafer sees upside to Q1 results and Q2 guidance, driven by demand for AI networking and custom ASICs as cloud service providers (CSPs) continue to expand their data center infrastructure.

Meet Samuel – Your Personal Investing Prophet

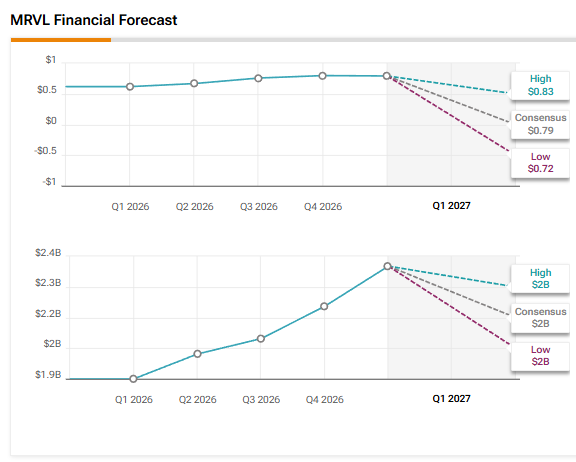

AMZO: built for a short position on AMZNMRVL stock has rallied 120% year-to-date, driven by strong demand for its custom AI chips and optical connectivity solutions. Wall Street expects MRVL to report earnings per share (EPS) of $0.79, reflecting 27.4% year-over-year growth. Revenue is estimated to rise by about 27% to $2.40 billion.

Here’s Why Wells Fargo Analyst Is Bullish on Marvell Stock

Rakers noted that Marvell has guided for more than 20% year-over-year growth in its custom XPU revenue in Fiscal 2027. More importantly, the company expects its Fiscal 2028 custom XPU revenue to more than double, driven by increasing deployments of Amazon’s (AMZN) AWS Trainium v2 and v3 chips, along with Microsoft’s (MSFT) Maia, which is expected to contribute more than $700 million in Fiscal 2028.

The 5-star analyst believes that investor sentiment is focused on Marvell’s potential to deliver upside to 30% to 40% plus year-over-year growth, driven by AWS’ expansion and additional upside from OpenAI and Anthropic Trainium commitments. Rakers highlighted that Amazon exited Q1 2026 with $225 billion in Trainium commitments. Interestingly, Wells Fargo analyst Ken Garelski estimates that AWS’ Trainium deployment capacity could expand by more than 2 gigawatts annually between 2027 and 2029.

Using a conservative assumption of about $3 billion in revenue per gigawatt (well below Broadcom’s (AVGO) $10 to $12 billion per gigawatt expectation), Rakers projects Marvell’s Trainium-only revenue to reach about $5.5 billion to $6 billion annually. This compares with Rakers’ current estimates for Marvell’s custom XPU revenue of $2.15 billion and $4.57 billion for FY27 and FY28, respectively, and the Street’s projections of $2.06 billion and $3.93 billion. He believes the upside could be closer to $5 billion to $6 billion, or more, per GW deployed.

Is MRVL a Strong Buy?

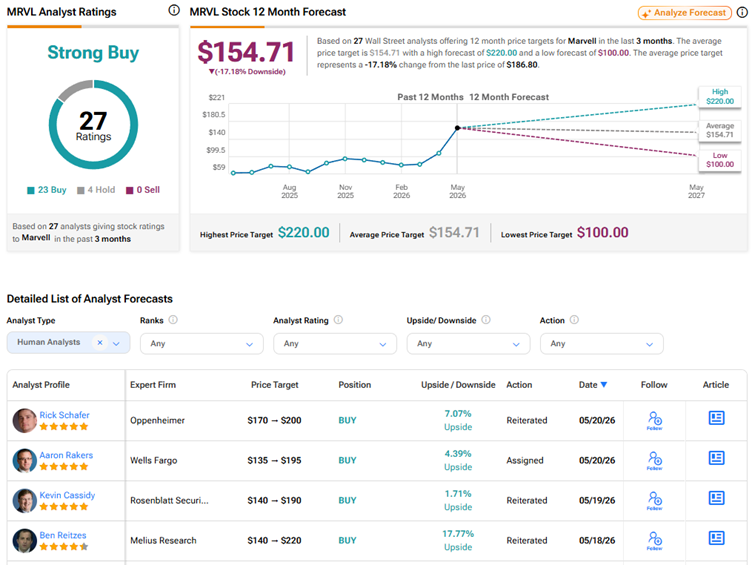

Ahead of Q1 FY27 earnings, Wall Street has a Strong Buy consensus rating on Marvell Technology stock based on 23 Buys and four Holds. The average MRVL stock price target of $154.71 indicates 17% downside risk, following a stellar year-to-date rally.