Nvidia (NASDAQ:NVDA) stock has been defined over the past two years by the company’s near-total control over the most valuable layer of the AI stack – the compute itself. That positioning turned Nvidia into the primary toll collector of the AI buildout, as hyperscalers raced to secure GPUs and scale out infrastructure. The result has been one of the most powerful growth cycles the semiconductor industry has ever seen.

Claim 55% Off TipRanks

Trade NVDA with leverageWhat’s changing now isn’t demand, but ownership of that stack. Nvidia’s revenues are still expanding at a rapid clip, yet the market reaction is becoming less forgiving as expectations stretch further and the conversation shifts from “how big” to “how durable.” Even strong results are struggling to clear that rising bar.

The latest pressure didn’t come from Nvidia’s own numbers, but from the very customers that fueled its ascent. Earnings from Alphabet and Amazon reinforced that AI spending remains elevated, yet they also pointed to a subtle pivot – a growing focus on in-house silicon designed to complement, and in some cases reduce reliance on, Nvidia’s chips.

So, the question is no longer whether AI spending continues – it clearly does – but how much of that spend continues to flow through Nvidia versus being absorbed internally by hyperscalers. If the largest buyers become partial competitors, Nvidia’s role evolves from indispensable supplier to one piece of a broader, more fragmented ecosystem.

That potential shift in where the dollars land makes Nvidia’s next move critical. If its grip on the GPU layer faces incremental pressure, the company’s ability to expand its footprint across the rest of the stack becomes far more important – and, according to top investor Yiannis Zourmpanos, that next leg of growth is “hidden in plain sight.”

“Many don’t realize that the CPU layer, which will benefit from heavy orchestration workloads in agentic AI, will make the CPU layer relevant and generate more revenues,” states the 5-star investor, who is among the top 1% of stock pros covered by TipRanks.

The crux of Zourmpanos’ investment thesis rests on the company turning into a full system AI factory. This transition began with Blackwell, he notes, and the next-gen Vera Rubin continues with this logic.

By integrating GPU, CPU, networking, and memory, Zourmpanos posits that Vera Rubin will allow Nvidia to generate additional revenues without adding to its existing clientele. The analyst further explains that this will have the additional benefit of increasing “the monetization rate per unit.”

And there’s another “weapon” that Nvidia has in its arsenal. Zourmpanos argues that Vera Rubin is turning CPUs into the “main component of the system,” and increasing the company’s control of the entire flow in the process. That will make it even more difficult for custom silicon to serve as a true alternative to Nvidia’s chips.

“The roadmap of the company is all about control rather than competition,” adds Zourmpanos, who gives NVDA a Strong Buy rating. (To watch Zourmpanos’ track record, click here)

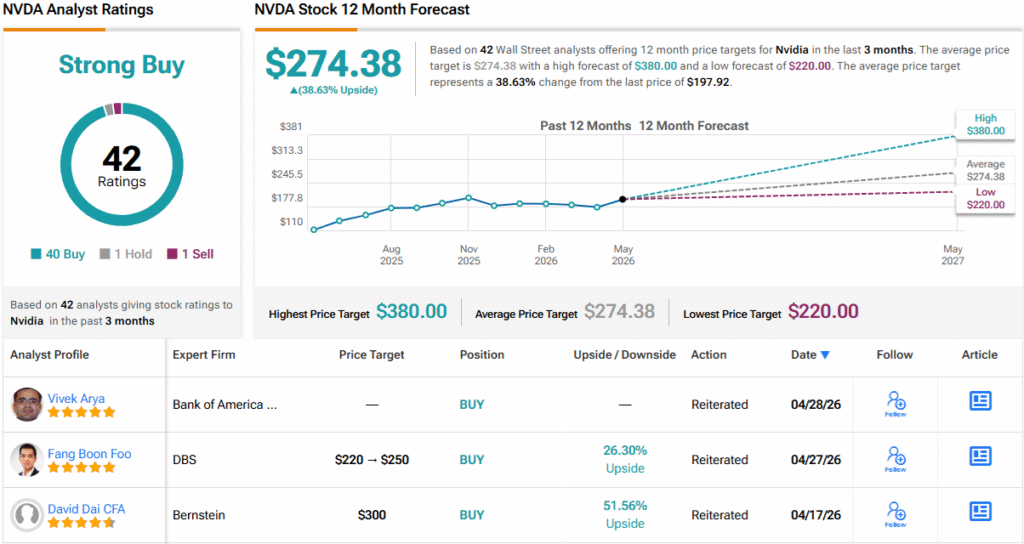

That’s the spirit on Wall Street as well. With 40 Buys, 1 Hold, and 1 Sell, NVDA continues to boast a Strong Buy consensus rating. Its 12-month average price target of $274.38 points to an upside approaching 40%. (See NVDA stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.