Apple (NASDAQ:AAPL) has long been a major player in the portfolio of legendary investor Warren Buffett. Now that the Oracle of Omaha has left the leadership of Berkshire Hathaway in the hands of CEO Greg Abel, some have been wondering whether the iPhone maker would continue to comprise such a significant chunk of the company’s holdings.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The answer is in, as Berkshire’s 13F filing on Friday made abundantly clear. With close to 228 million shares as of March 31, 2026, Apple comprises just over one-fifth of Berkshire’s holdings – its largest position.

Apple’s share price has been steadily moving upward, gaining some 10% year-to-date. For top investor Daniel Sparks, Berkshire’s move makes a lot of sense.

“Beyond the portfolio mechanics, Apple’s underlying fundamentals make Berkshire’s decision to leave the largest position alone look easy,” explains the 5-star investor, who is among the top 1% of stock pros covered by TipRanks.

Sparks believes that Apple’s business is “a long-term hold,” pointing to its recent quarterly earnings for validation. For one thing, the company just posted its best March quarter of all time, with revenue rising 17% year-over-year to reach $111.2 billion.

Better yet, this growth was global, as Apple delivered double-digit growth across every geography. This extended to different segments as well, notes Sparks, with iPhone revenue increasing year-over-year by 22% to $57 billion and services revenue hitting an all-time high of $31 billion (an increase of 16%).

“And the services business may matter even more than the top-line numbers suggest; the segment’s gross margin in fiscal Q2 came in at 76.7%, far above the 38.7% products gross margin,” adds Sparks.

The investor does note that there are some risks, however. These include growing memory costs and the upcoming leadership transition at Apple, with CEO Tim Cook set to step aside on September 1.

Still, Sparks isn’t deterred by these concerns, liking what he sees from AAPL (and by extension Berkshire). And that makes him view Berkshire, under this new leadership, more positively.

“Ultimately, the way Abel handled Berkshire’s biggest positions in his first quarter as CEO arguably makes the conglomerate’s stock more attractive,” concludes Sparks. (To watch Sparks’ track record, click here)

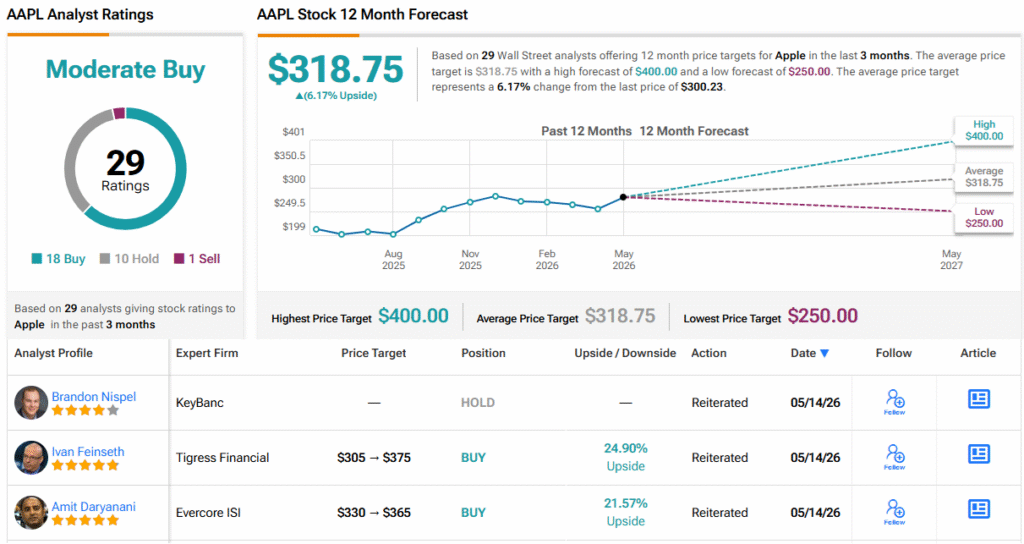

Wall Street appears content to stick with AAPL as well. With 18 Buys, 10 Holds, and 1 Sell, AAPL enjoys a Moderate Buy consensus rating. Its 12-month average price target of $318.75 points to an upside of ~6%. (See AAPL stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.