Magnet Forensics (TSE: MAGT), a digital investigation software company, recently reported its Q3-2022 results. Magnet’s results beat revenue expectations but missed earnings-per-share (EPS) estimates. Nonetheless, the company is growing at a rapid pace, and the earnings report was good enough to send the stock soaring. Please note that the following figures are in U.S. dollars unless otherwise stated.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

MAGT’s revenue rose to $25 million (a 41% year-over-year increase), which beat expectations of $23.93 million. Notably, its annual recurring revenue grew by 50% to $80.9 million.

However, its adjusted earnings per share were $0.03, less than the $0.05 consensus estimate ($0.07 in Canadian dollars). This is also lower than last year’s EPS of $0.05.

Still, Magnet Forensics’ adjusted EBITDA rose 25% year-over-year to $5.9 million, and the company’s gross profit margin stayed at a very high 93%.

Regarding cash flow from operations for the nine months ended September 30, it was $8.52 million compared to ~$9.05 million in the same period last year. The company’s cash position also increased by 3.55% to $122.3 million while having negligible debt.

Lastly, the company provided full-year 2022 guidance. Revenue is expected to grow by 37% to 39%, reaching $96 million to $98 million, and adjusted EBITDA is forecast to be $16 million to $19 million compared to $14.9 million last year.

Is Magnet Forensics Stock a Buy, According to Analysts?

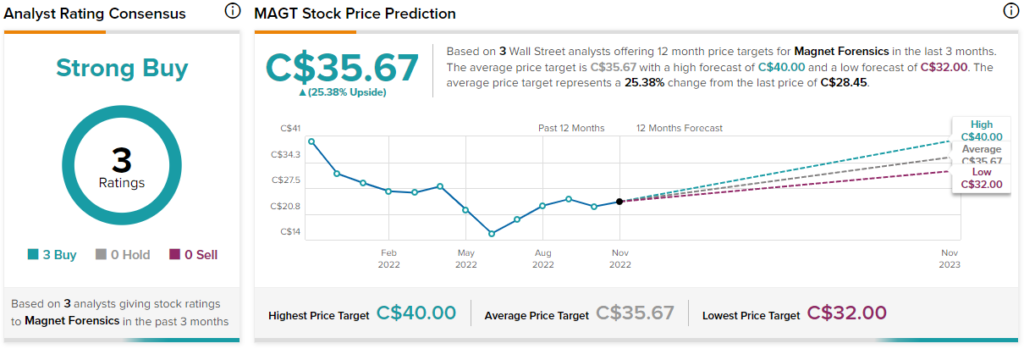

According to analysts, Magnet Forensics has a Strong Buy consensus rating based on three Buys assigned in the past three months. The average Magnet Forensics price target of C$35.67 implies 25.4% upside potential.

Conclusion: Magnet’s Earnings Report Was Mixed but Solid

Operating in a resilient industry, Magnet Forensics’ business is still performing relatively well in the current environment. While the earnings report was mixed, the company is still experiencing high growth while maintaining profitability – something that many companies find hard to achieve.