As advancements in autonomous driving continue to advance, Luminar Technologies (LAZR) is well-positioned to tap into the market’s potential growth. The company made significant strides in the third quarter of 2024, boasting new deals with global automakers and an upswing in production with Volvo Cars (V). Despite a challenging balance sheet and a need for restructuring, industry analysts believe that if Luminar can navigate through this tricky period, it could be looking at a significant model ramp-up and clearer visibility into reaching breakeven.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

However, recent disappointing Q3 revenue results and ongoing financing activities question the stock’s immediate future. While it is an intriguing option, investors may want to wait a bit longer and look for positive financial results in the next quarter or two before taking action.

Luminar Progressing on Several Fronts

Luminar Technologies is an automotive player developing advanced LiDAR technology. It has made significant progress year-to-date, contributing its technology to the successful launch of the Volvo SOP and the TPK facility for additional capacity and improved cost.

The successful ramp-up of Volvo’s EX90 shows promise, with the delivery of four figures of vehicles set to jump to five figures in the coming months. Further, Volvo has adopted Luminar as standard equipment on its next model, solidifying the partnership. Luminar has also signed an advanced development contract with a Japanese OEM for the next-gen assisted driving system.

Furthermore, the company unveiled its next-gen LiDAR, Luminar Halo, which remains on track for sample deliveries to select customers by the end of this year. Luminar Halo has successfully demonstrated its increased performance capabilities at a lesser cost and size than the previous iteration. A mass launch for Halo is anticipated in 2026.

Luminar continues its commitment to growing its LiDAR ecosystem and plans to launch its insurance app soon, with the start of initial policy writings expected in early next year.

In other news, Luminar plans to execute a 1-for-15 reverse stock split to enhance stock value, effective November 20, 2024

Analysis of Luminar’s Recent Financial Results

The company recently reported results for Q3. Revenue of $15.49 million missed analysts’ expectations of 18.7 million and marked an 8.7% year-over-year decrease. The decline was mainly due to renegotiating a significant non-automotive, non-series production contract. However, despite this renegotiation, the firm experienced growth in sensor sales during the quarter.

The company reported a GAAP gross loss of $14 million and a non-GAAP gross loss of $11.7 million, consistent with previous guidance. Non-GAAP earnings per share (EPS) of -$0.16 missed consensus estimates by $0.01.

As of the quarter’s end, the company reported $249 million in cash and access to $431 million in capital, providing a reasonable runway to last until the end of 2026.

Further, Luminar has implemented operational restructuring steps to foster cost savings measures. Since the beginning of the year, the firm reduced its workforce by approximately 30%, initiated contract reductions, and downsized its real estate footprint to generate a projected annual savings of $145 million by the end of next year.

What Is the Price Target for LAZR Stock?

Shares of the company have been volatile (beta of 2.84) and declining, shedding roughly 70% in the past year. The stock trades near the low end of its 52-week price range of $0.73 – $3.69 and shows ongoing negative momentum by trading below the 20-day (0.93) and 50-day (0.93) moving averages. Despite the decline in share price, the company trades at a premium to the industry, with a P/S ratio of 6.33x compared to the Auto Parts industry average of 0.55x.

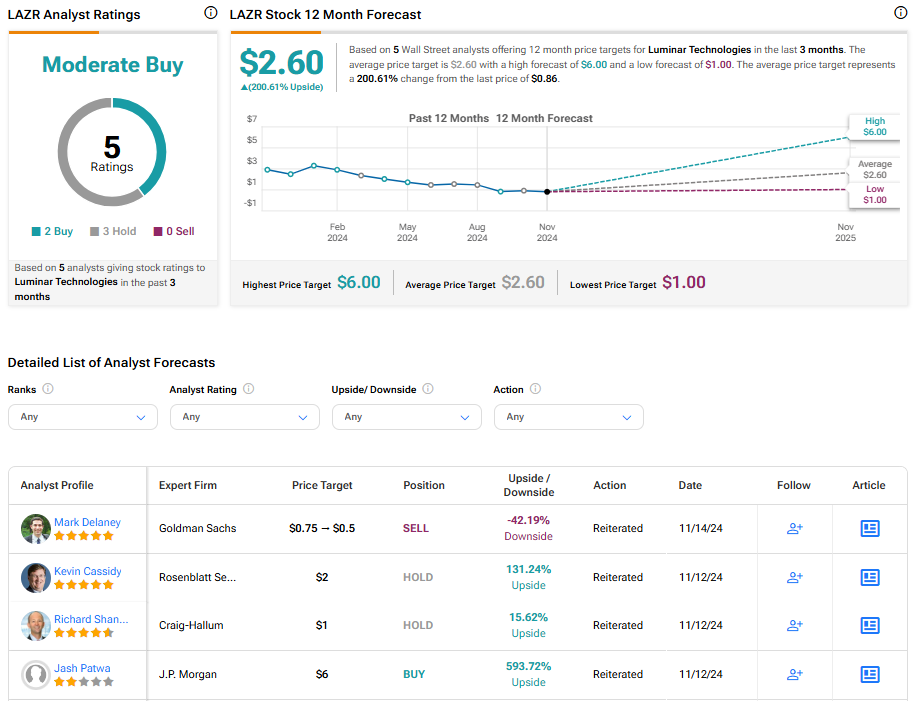

Analysts following the company have taken a cautious view of LAZR stock. For instance, Craig-Hallum analyst Richard Shannon recently lowered the price target on the shares from $1.50 to $1 while maintaining a Hold rating. Shannon noted that the company is ramping up with its first meaningful customer, a vehicle that has lidar as a standard, with another model on the way. Yet its balance sheet and cost structure need a lot of work.

Luminar Technologies is rated a Moderate Buy overall, based on the most recent recommendations of five analysts. The average price target for LAZR stock is $2.60, representing a potential upside of 200.61% from current levels.

Bottom Line on LAZR

Luminar Technologies is well-positioned to participate in the autonomous driving industry’s expected growth as technology accelerates. Despite recent financial hurdles, the company’s forward movement, including new deals with global automakers and increased production with Volvo, suggests future optimism. Moreover, successful advancements such as the next-gen LiDAR, Luminar Halo, and a planned insurance app launch further reflect Luminar’s commitment to growth. However, despite displaying potential, investors may wish to monitor the company’s near-term financial results before committing to the stock.