Lululemon (LULU) stock looks like a train wreck, trading near its 52-week low after falling about 62% over the past 12 months. At first glance, that kind of collapse may make the stock look like a tempting “buy-the-dip” opportunity. However, I do not see it that way. As long as negative comparable sales in the Americas, falling profitability, elevated inventory, and leadership uncertainty persist, I believe the stock is likely to underperform. That is why I view LULU as a Sell today.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

The problem is that Lululemon’s decline does not appear to be a simple overreaction. In my view, the market has stopped treating the company as a premium athletic apparel retail compounder with high margins and predictable growth. Instead, investors have started pricing it more like a cyclical retailer facing issues around demand, execution, and margins.

Weak Comps, Falling Margins, Rising Inventory

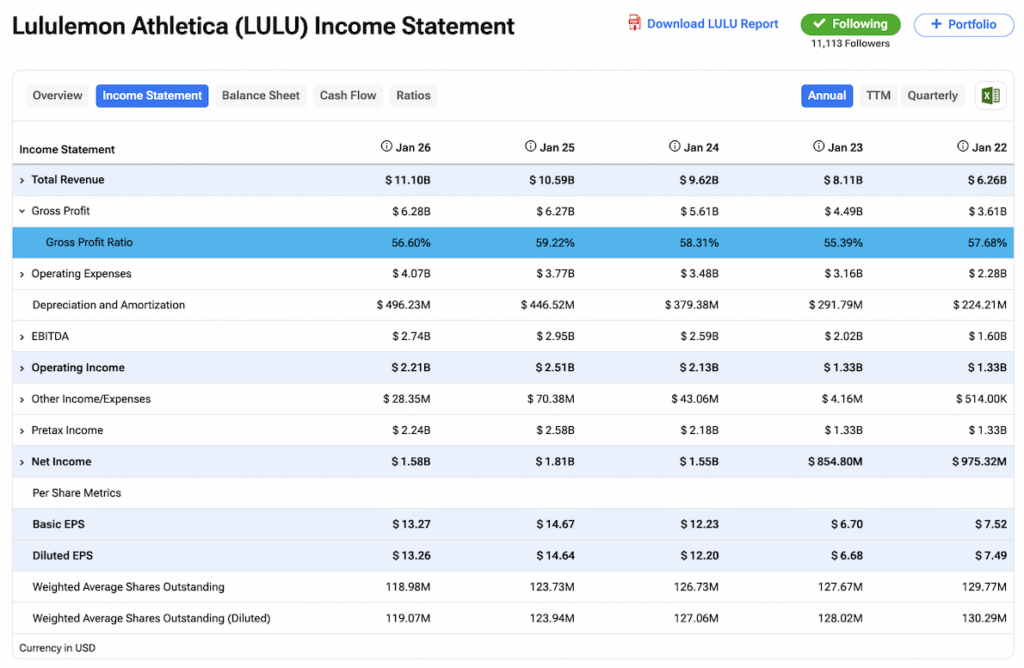

The Canada-based retailer is still growing internationally, but the problem is that the market primarily focuses on the Americas, since this remains the brand’s most mature and important region. In Q3 2025, Lululemon reported a 5% decline in comparable sales in the Americas, while International comps grew 18%. In Q4 2025, Americas comps fell another 1%, even as International comps increased 20%. For the full FY25, Americas comps declined 3%, while International comps rose 15%.

To make matters worse, weak comp sales in its core market have been accompanied by a sharp decline in gross margin, highlighting the erosion of the brand’s strong pricing power from just two to three years ago. Lululemon reported gross margins of 56.6% in FY26, down 260 basis points from 59.2% in FY25. At the same time, operating margin fell 380 basis points to 19.9%.

Inventory trends reinforce this view. Lululemon ended 2025 with $1.7 billion in inventory, up 18% year-over-year, while revenue grew just 5%. When inventory grows much faster than sales, investors begin to question whether the brand can still sell products at full price as it once did. In this case, the answer appears to be clearly no.

When the Growth Story Lost Its Shine

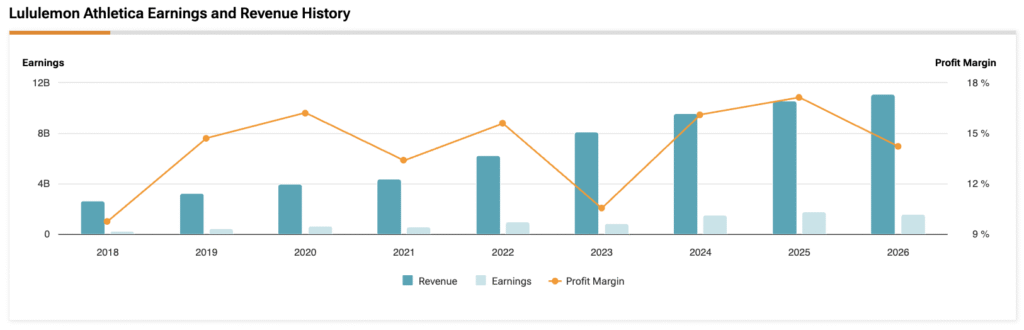

A big part of the Lululemon story is how richly the stock was valued in the post-pandemic period through 2024, reaching as much as 65x earnings in January 2024. That period was driven by the athleisure trend — sportswear becoming part of everyday life — and by a much more casual corporate environment. Lululemon was firing on all cylinders.

Lululemon carved out a unique position by offering products that were more premium than Nike (NKE) and Adidas (ADDYY), yet more functional than those of traditional luxury brands. Its direct-to-consumer model, minimal reliance on wholesale, and strong pricing power all supported exceptionally high margins.

By FY25, the company had reached peak profitability. Since then, the normalization of those margins has led investors to question whether the stock still deserves a premium multiple. So much so that LULU now trades at a mere 9.8x forward P/E, a 35% discount to the industry average of near 15x, and more than 70% below its own five-year average valuation.

Much of the decline in comparable sales and margins in the Americas appears to be tied to market share losses, driven by weak execution in marketing and product assortment. Meanwhile, premium athleisure brands such as Vuori and Alo Yoga have gained both share and cultural relevance in the U.S., particularly among higher-income consumers and younger audiences. Lululemon has not lost its leadership position, but the market no longer views it as the only aspirational brand in the category.

A New CEO, but Not a Fresh Start

The latest developments at Lululemon Athletica center around changes in its C-suite. Former CEO Calvin McDonald had led the company since 2018 and was largely responsible for its strong growth cycle from 2019 to 2024. However, in late 2025, he was effectively pushed out as the board concluded that Lululemon needed a new strategic direction.

The company was then led by internal executives during the transition until April, when Heidi O’Neill, a former senior executive at Nike, was selected for the role. The idea was to bring in someone with deep product and branding experience to help restore the brand’s “cool factor.”

The chaos was further fueled as Chip Wilson — Lululemon’s founder and one of the company’s most vocal critics — did not fully endorse O’Neill’s appointment.

A Turnaround Story Still without Conviction

Chip Wilson stated that he “hopes” Heidi O’Neill is the right person for the job. However, he also emphasized that a nearly 30-year veteran of Nike does not, by itself, represent the transformational leadership he believes is necessary. He also argued that, without a board with deep expertise in branding and product, even a capable CEO would struggle to execute a successful turnaround.

Following Wilson’s remarks, Lululemon Athletica shares fell to a new 52-week low, as the market arguably interpreted Heidi O’Neill as a relatively conservative choice. There are few guarantees of immediate, radical changes. The most visible signs of execution will likely not emerge until 2027, since Heidi O’Neill does not officially take over until September 2026.

Under current conditions, Wall Street expects Lululemon’s revenue growth to remain in the mid-single digits over the next few fiscal years, with consensus around 3.5% near-term and about 4.5% annually over three years. That is a dramatic slowdown from what the company delivered over the past several years. For that reason, I am not surprised the stock is in tatters right now. I would not risk buying the dip until the governance situation stabilizes and management presents a more constructive path forward.

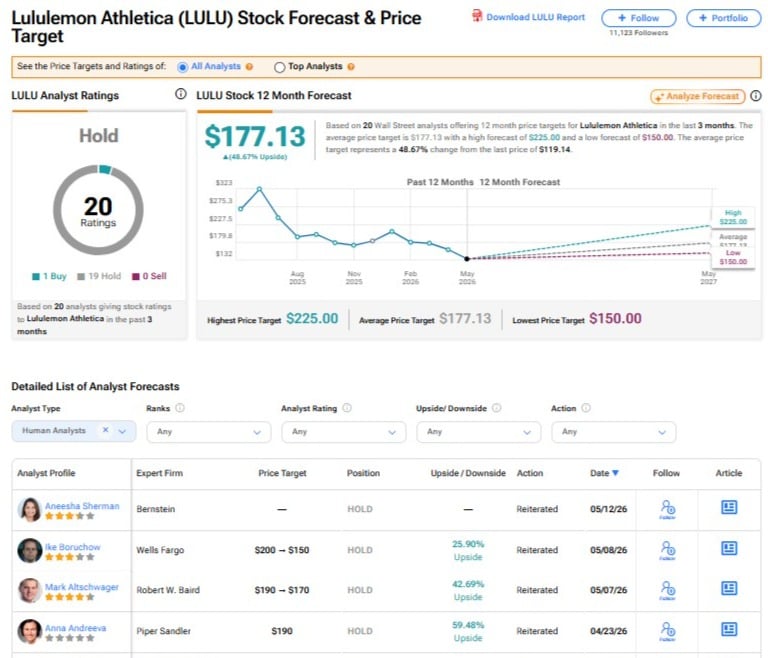

Is LULU a Buy, Hold, or Sell, According to Wall Street Analysts?

Wall Street remains broadly skeptical about Lululemon Athletica’s outlook, assigning the stock a Hold consensus rating. Of the 20 analysts who have covered LULU over the past three months, 19 recommend Hold, and only one rates the stock a Buy. The average LULU price target of $177.13 implies potential upside of 48.67% from current levels.

Not Every Dip Is Worth Buying

I view LULU as a Sell today. The valuation has become very cheap, but I do not think that, on its own, is enough to make the stock attractive. The problem is that the current discount reflects a real deterioration in the key pillars of the investment thesis. Negative same-store sales in the Americas, falling margins, elevated inventory levels, a loss of cultural relevance, and leadership uncertainty all point in the same direction.

These are structural issues that require concrete actions to be resolved. So far, management does not seem to be conveying the level of confidence and clarity needed to support a more convincing turnaround story. As long as that remains the narrative, I see little reason to treat the decline as a simple “buy-the-dip” opportunity.