Palantir (NASDAQ:PLTR) shares are down about 1% in Monday’s after-hours session following the company’s Q1 earnings release, a muted reaction despite a strong set of results and an outlook that continues to point to robust growth.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Palantir reported non-GAAP EPS of $0.33, beating the $0.28 consensus, alongside revenue of $1.63 billion, up ~84% year over year and ahead of expectations by about $90 million. The company now expects Q2 revenue of $1.797 to $1.801 billion, above the $1.68 billion consensus, while full-year 2026 revenue is projected at $7.65 billion to $7.66 billion, also ahead of the roughly $7.28 billion expected.

Still, the weak move suggests that investors are weighing that upbeat outlook against valuation and execution risks that remain part of the story.

That cautious tone is echoed by RBC’s Rishi Jaluria, who continues to argue that valuation remains the central issue. While the analyst acknowledges Palantir’s growth profile stands out versus peers, he writes that he “struggle[s] to underwrite a scenario that justifies current valuation levels,” pointing to what he sees as limited room for further multiple expansion.

Jaluria also highlights what he views as a shift in investor focus, particularly among retail participants. The analyst notes that investors “remain focused on the potential for a stock split and dividend payments,” suggesting attention may be drifting toward capital return narratives rather than core business fundamentals, and hinting that some investors could become frustrated given the company’s sizable cash position and lack of direct returns.

Beyond valuation and sentiment, Jaluria’s concerns extend to execution, especially in the commercial segment. The analyst points to “ongoing churn discussions among enterprise clients,” which raises questions about retention and the durability of growth as competition intensifies across AI-driven software offerings. He also flags broader risks tied to government revenue sustainability, geopolitical considerations, and rising competition from large AI labs targeting similar use cases.

Taken together, the setup reflects a company that continues to outperform expectations and raise its outlook, while still facing a debate around whether that strength is enough to justify the current valuation.

That tension ultimately underpins Jaluria’s call, as he assigns PLTR an Underperform (i.e., Sell) rating with a $90 price target, implying about 38% downside from Monday’s closing price. (To watch Jaluria’s track record, click here)

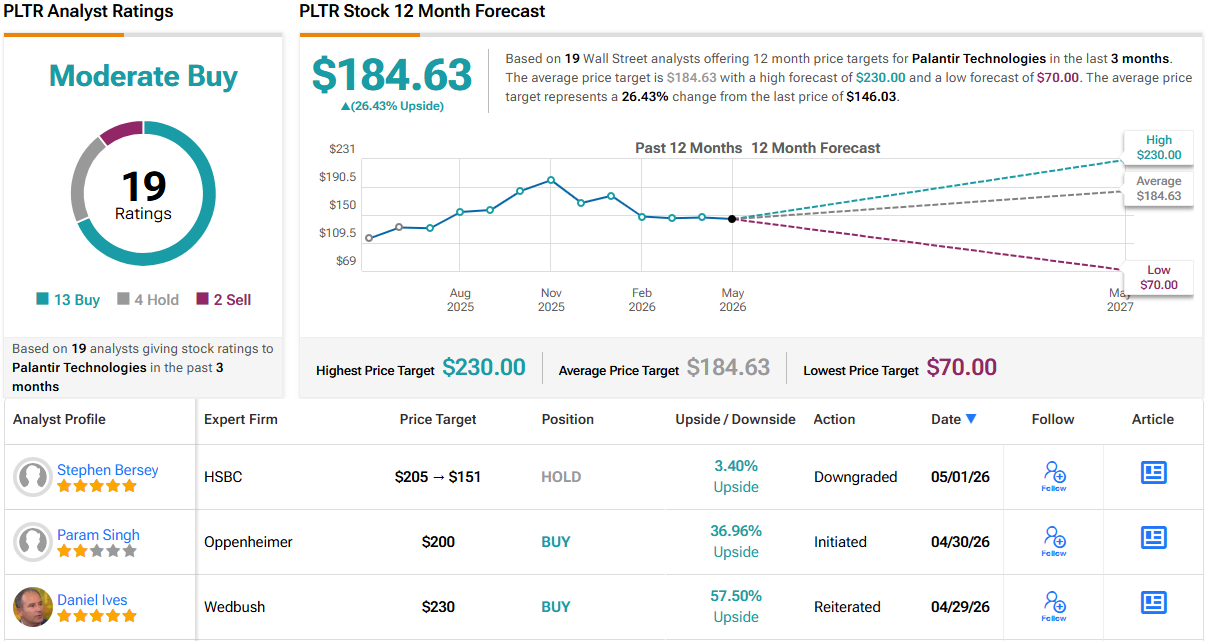

While that cautious view is one side of the debate, Wall Street overall still leans positive on Palantir. The stock carries a Moderate Buy consensus based on 19 analyst ratings, including 13 Buys, 4 Holds, and 2 Sells. Price targets also point higher, with an average of $184.63, implying about 26% upside from current levels. (See PLTR stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.