Joby Aviation (JOBY) is set to report Q1 2026 results after the close on May 5, and the key focus will not be profit. Instead, the market will watch for signs that Joby is still on track with FAA work, its plant ramp, and its plan to launch paid air taxi service.

Claim 55% Off TipRanks

Trade JOBY with leverageThe eVTOL firm is still in a build phase, so a loss is widely expected. The main issue is pace. Joby has made clear gains in FAA work, and its last call showed real steps ahead. The firm said its first FAA-conforming aircraft was ready to fly, while aircraft meant for TIA tests were in the build stage. It also noted an 18-point gain in Stage 4 FAA work.

That makes the next update key. Any fresh news on FAA tests, issue papers, or flight work with FAA pilots could shape how the stock trades. On the other hand, slow progress could reignite fears that the launch path may take longer.

Meanwhile, JOBY shares rose 0.65% on Friday, closing at $9.25.

Cash Use and Blade Revenue Will Also Matter

Cash burn will be the next big item. Joby ended Q4 with $1.4 billion in cash, cash-like items, and short-term assets after a large raise. That gives the firm more room to fund its plan. Still, Joby used $157 million in cash in Q4 and guided for $340 million to $370 million in cash use for the first half of 2026, not counting a $33 million site buy in Ohio.

As a result, Q1 cash use will be watched closely. If spending stays near plan, it may help ease some fear. If it runs hot, bears may point to more risk tied to the plant ramp, FAA work, and staff growth.

At the same time, the Blade business should help Joby show some near-term sales. In August 2025, JOBY acquired Blade Air Mobility’s (BLDE) short flights business in New-York for $125 million. Blade’s already registered more than 50,000 passengers prior to the acquisition. In Q4, JOBY had $31 million in sales, with $21 million from Blade. For 2026, the firm expects $105 million to $150 million in sales, with most coming from Blade. Even so, Blade is not the full story. It is more of a bridge while Joby works to launch its own aircraft.

The market will also look for fresh color in Dubai. On the last call, Joby said it had “plans to carry first passengers in the UAE this year.” If that goal still stands, it could help support the bull case.

Overall, Joby remains a high-risk, high-reward name. The firm has cash, partners, and real FAA progress. However, it still faces large losses, high cash use, and key launch risks. For Q1, the main question is simple: can Joby show that its path to paid flight is still on track?

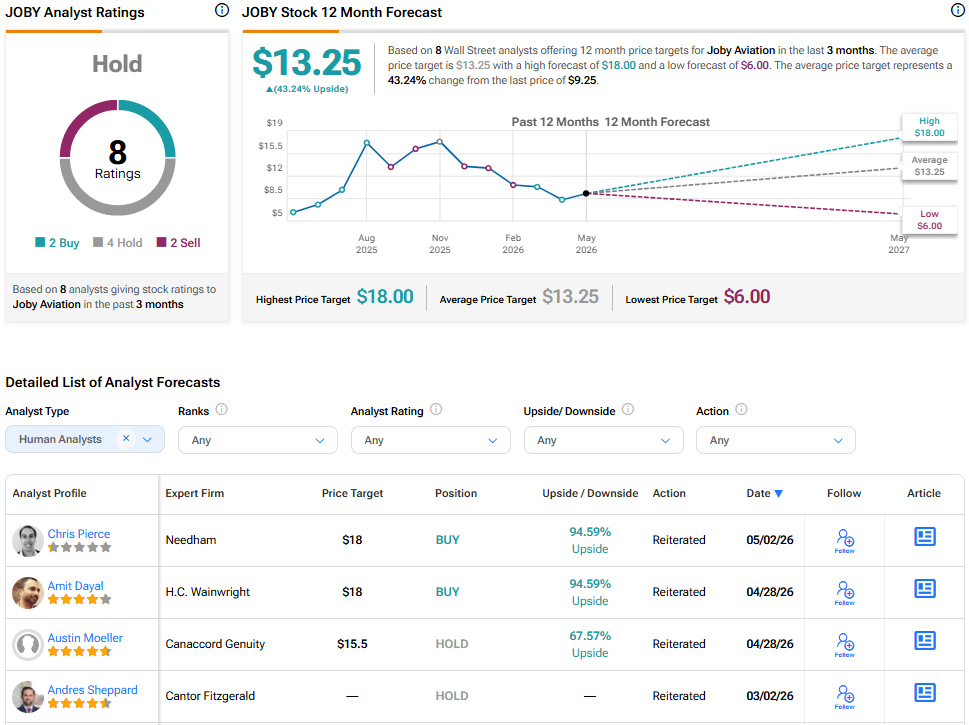

Is JOBY a Good Stock to Buy?

On the Street, Joby Aviation divides opinions with a Hold consensus rating. Out of eight analysts, two rate it a Buy, four rate it a Hold, and two rate it a Sell. The average JOBY stock price target is $13.25, implying a 43.24% upside from the current price.