Joby Aviation (JOBY) gave investors a clear message in its Q1 earnings report. The air taxi firm is still not a full-scale business, but it is moving closer to launch. The market gave Joby’s report a cool response. JOBY shares slipped 2% on Tuesday, while the stock rose slightly in pre-market trading.

Claim 55% Off TipRanks

Trade JOBY with leverageThe main bright spot was progress on its U.S. flight plan. Joby said it expects first operations to begin in 2026 through the White House-backed eVTOL pilot plan. The firm was named in several winning bids tied to states such as New York, New Jersey, Texas, Florida, and Utah.

Joby also had a strong show in the air. It kicked off its 2026 Electric Skies Tour with flights near the Golden Gate Bridge and then flew in New York City. The firm said it made the city’s first point-to-point eVTOL flights, from JFK to three Manhattan heliports.

In the report, CEO JoeBen Bevirt said, “This has been an extraordinary quarter for Joby.” He also said the firm ended the quarter with “a very strong balance sheet and the clearest path we’ve ever had to beginning passenger operations.”

Certification Progress Is the Key Point

For investors, the biggest point was not sales. It was FAA progress.

Joby said its first FAA-conforming aircraft for Type Inspection Authorization took flight in the quarter. The firm also said it completed its SR3 audit with the FAA. This is the third of four key reviews in the type approval path.

At the same time, Joby is building more of the base it needs to scale. The firm said parts are now in work for eight more conforming aircraft. It also said the output of composite parts is now more than 2.5 times last year’s level. In Ohio, Joby has started propeller blade work and has raised its total plant space to nearly 1.5 million square feet.

Still, the low points are clear. Joby is not yet a profit story. It is still a cash burn story. The firm ended the quarter with $2.5 billion in cash, cash-like assets, and short-term investments, which gives it room to fund its plan. However, large spend will remain part of the story as Joby works through FAA review, test flights, plant growth, and early launch work.

Bottom Line

Joby’s first quarter was a good update for the long-term story, but not a clean win in terms of numbers. The firm made real gains in FAA work, public flight demos, and plant scale. Also, its cash pile gives it more room than many peers.

However, investors still need to watch the same core risks. Joby must win full FAA approval, start safe service, make more aircraft, and show that air taxi demand can turn into a real business.

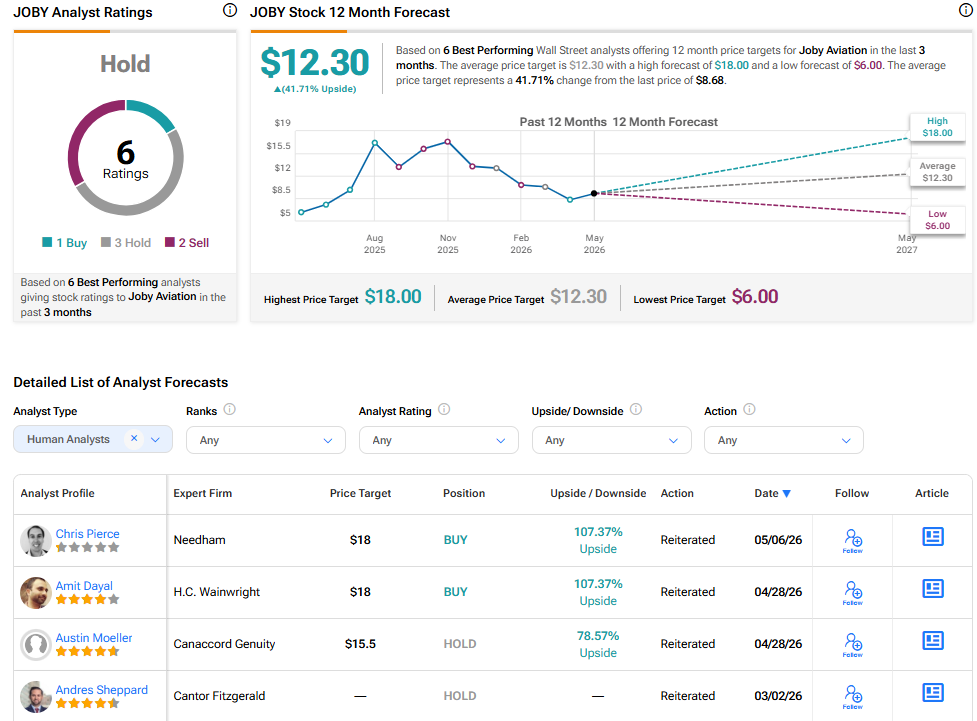

Is JOBY a Good Stock to Buy?

On the Street, Joby Aviation continues to divide opinions with a Hold consensus rating. Out of six analysts, one rates it a Buy, three rate it a Hold, and two rate it a Sell. The average JOBY stock price target is $12.30, implying a 41.71% upside from the current price.