Through whatever timeframe you look at it, Sandisk (NASDAQ:SNDK) stock’s performance has been nothing short of mind-blowing. The shares are up by 494% year-to-date and have climbed an amazing 4,068% over the past year.

Claim 55% Off TipRanks

Trade SNDK with leverageThe company is benefiting from the rapid expansion of AI data centers, which are driving strong demand for high-performance solid-state drives (SSDs) and NAND flash memory, products critical for storing and processing large-scale training datasets, while tight supply across the industry has given the company room to push through meaningful price increases, leading to exceptional revenue growth and a significant lift in gross margins and profits. At the same time, in an industry known to be highly cyclical, the company is now starting to lock in long-term contracts, which are making its revenue streams more predictable.

So, against that backdrop, the company has become a market darling, and its upward trajectory continued following the firm’s recent fiscal third-quarter results. The readout featured a double beat and a guide that exceeded expectations, and the shares reacted accordingly.

However, one investor, who goes by the pseudonym The Techie (TT), believes the market may be overlooking an important issue.

“SanDisk’s multi-year earnings path is now bracketed, as you can’t have a violent upside surprise in FY27/FY28 if a majority of bits are pre-sold at today’s economics,” TT argued.

The company has signed New Business Model (NBM) agreements with customers. These represent a strategic move to smooth out revenue in an industry known for its volatility and cyclicality. Rather than depending primarily on spot-market pricing, Sandisk is locking in multi-year deals with major customers that come with committed financial terms and guaranteed volumes.

But TT argues the NBMs are effectively locked in peak economics, limiting future upside, as five multi-year agreements covering more than one-third of FY27 bit output were secured at 4Q26 pricing levels, so any further ASP gains will apply only to a diminishing pool of uncontracted bits.

Additionally, TT says the gains were driven entirely by pricing and product mix rather than underlying demand, as bit shipments declined by the high-teens sequentially, and the FQ4 guide suggests a sharp slowdown in pricing momentum. At the same time, SNDK’s technical profile appears overextended, with an RSI of 74 and the shares trading well above all key EMAs, making for an “unfavorable risk-reward.”

Therefore, TT says the earnings call should be seen as a warning to investors and recommends staying away from this name.

“With most of the positives priced in a few quarters out, I’m maintaining the stock with a Sell at these levels, as the easy money in the stock has been made, and the risk-reward turns less favorable following the run,” TT summed up. (To watch The Techie’s track record, click here)

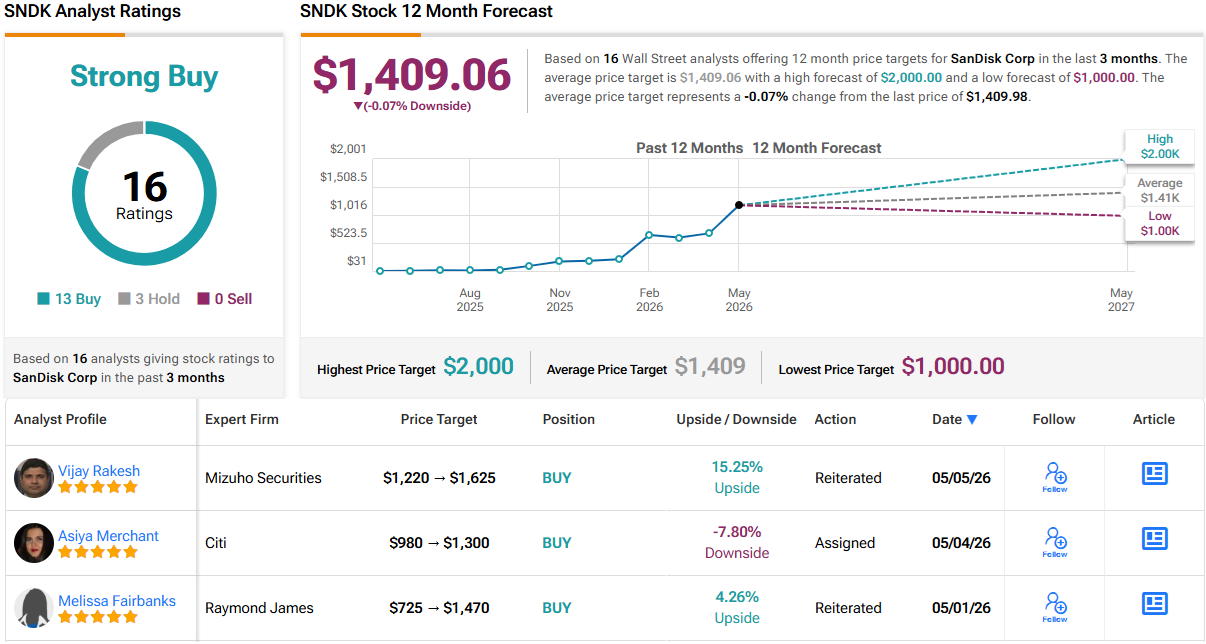

However, none of the Street’s analysts agree with that view. In fact, based on 13 Buys vs. 3 Holds, the stock claims a Strong Buy consensus rating. Still, that bullish stance may not be as convincing as it first appears, considering the average price target of $1,409.06 suggests shares will stay rangebound in the near term. With that in mind, investors should keep a close eye on potential price-target revisions in the coming weeks. (See SNDK stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.