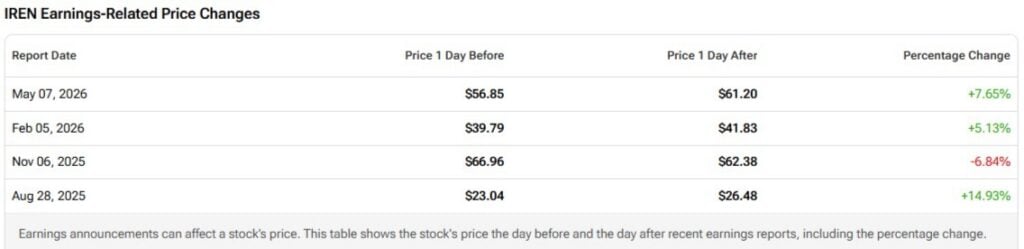

IREN Limited (IREN) is in the middle of a major transformation from a Bitcoin (BTC-USD) miner to an artificial intelligence (AI) infrastructure solutions provider. The AI data center business headquartered in Australia missed revenue estimates for Fiscal Q3, but the stock jumped nearly 8% on May 8 as investors focused on the company’s major expansion plans and its new $3.4 billion cloud AI deal with Nvidia Corporation (NVDA).

Claim 55% Off TipRanks

Forget margin or options. Here's how the pros trade IRENI am bullish on IREN for a few reasons, including its strong liquidity position, strategic partnerships with industry heavyweights, and its global expansion strategy.

IREN’s Business Transformation Is Gaining Momentum

At the center of my bullish stance on IREN is its strategic business transformation. IREN, formerly known as Iris Energy, was a Bitcoin miner. Over the past year or so, the company has laid the groundwork to transform itself into a cloud AI solutions provider. This decision continues to impact its short-term financial performance, but the company seems to be on the right track, going by its recent partnership wins.

IREN’s revenue declined from $184.7 million in Q2 FY2026 to $144.8 million in Q3 FY2026. While this may not look like a good sign, this revenue decline came on the back of Bitcoin mining revenue falling from $167.4 million in Q2 to just $111.2 million in Q3. This came as a result of lower average BTC prices and the company’s strategic steps to decommission mining hardware as part of its business transformation.

The good news is that IREN’s AI cloud business gained momentum in Q3. Revenue from this segment almost doubled from $17.3 million in Q2 to $33.6 million in Q3. The company also secured a new $3.4 billion cloud AI contract with Nvidia, pushing the total contracted backlog to a massive $3.1 billion of annual recurring revenue (ARR). Last year, the company guided for $3.7 billion in ARR by the end of 2026, and IREN seems to be well on track to achieve this goal.

IREN Maintains a Strong Liquidity Position

My bullish stance on IREN is strengthened by the company’s well-managed liquidity position. It is common to see companies struggling with liquidity constraints during business transformation, but IREN is proving to be an exception. The company ended Q3 with cash and cash equivalents of $2.6 billion.

A deeper dive into IREN’s capital deployment strategy reveals a unique funding structure in which the company uses funding commitments from its partners to cover capital expenditures. Microsoft (MSFT) provided an upfront prepayment as part of its multi‑year capacity agreement with IREN, approximately 20% of the contract value, and IREN says customer prepayments are a key funding source for its infrastructure buildouts.

IREN has assembled a financing package that combines those prepayments with graphics processing unit (GPU) and other debt arrangements to cover most of the project’s capital needs; some portions of that financing were arranged at unusually low interest rates, reported to be around 3%, for certain facilities or equipment financing.

IREN Is Expanding into a Global AI Company

IREN’s focus on global expansion while executing its business transformation also deserves praise. On May 7, the company announced the acquisition of Nostrum Group, a data center developer based in Spain. This marks the company’s entry into Europe. This deal adds about 490 MW of power to the company’s data center capacity. Leading data center operators have already identified Spain as a key strategic hub given favorable AI policies and access to cheap renewable energy, so IREN seems to have delivered a masterstroke with this acquisition.

On May 5, just two days before the Nostrum Group acquisition, IREN announced the acquisition of Mirantis for $625 million as well. This is a move aimed at expanding the company’s client base from hyperscalers, such as Microsoft, to large enterprise clients. Mirantis is focused on developing the orchestration layer for enterprises deploying AI, which includes virtual machines and Kubernetes.

Both acquisitions will help the company’s margin profile. Nostrum will primarily help IREN by ensuring the company has sufficient power capacity to execute the contracts it has secured from hyperscalers. Mirantis, on the other hand, will help the company expand into new revenue streams with higher margins. Mirantis is likely to help IREN emerge as a Managed Cloud Services Provider through its K0rdent AI platform.

Is IREN a Buy, According to Wall Street Analysts?

Based on the ratings of 11 Wall Street analysts, the average IREN price target is $69.90, which implies upside of 23.59% from the current market price.

Even with a 754% increase in market value over the past 12 months, IREN stock is still trading below analyst price targets, as the company’s business transformation has forced analysts to hike their price targets at regular intervals.

Takeaway

IREN is no longer the Bitcoin miner it used to be. While a significant percentage of its revenue is still generated from Bitcoin mining, the company has successfully laid the foundation to emerge as a global AI data center giant in the long run. The strategic partnerships it has secured with Microsoft and Nvidia, recent acquisitions, and its focus on maintaining strong liquidity levels during this business transformation make the company an attractive bet on AI data center growth.