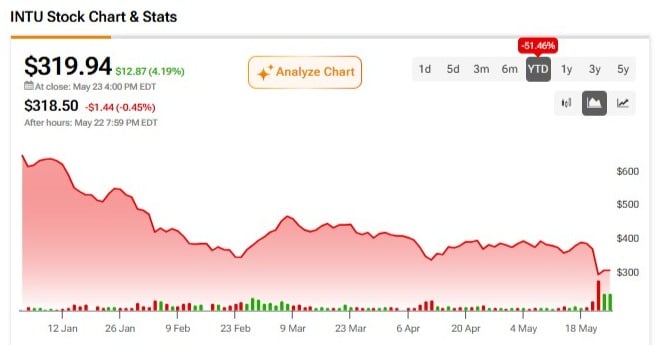

Intuit (INTU) stock looks broken after one of the sharpest valuation resets among premium software names. The “SaaSpocalypse” has hit the company hard, as investors increasingly question whether generative artificial intelligence (AI) could erode the moat around the company’s core tax and accounting platforms. Meanwhile, the latest Q3 report did not help much. Pressure among price-sensitive do-it-yourself (DIY) tax filers, weaker Mailchimp trends, and a large workforce reduction made the story look far messier than before.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Still, I don’t believe the business itself is broken. Intuit raised full-year guidance, remains highly profitable, and is still expected to grow revenue and earnings at a double-digit pace. With the stock now trading at a deep discount to its historical valuation, I believe the sell-off has gone too far, making INTU a Buy.

Why Investors Trusted Intuit for So Long

Until the middle of last year, Intuit was viewed as one of the most “secure” and premium fintech platforms in the market. After all, the company’s core products — TurboTax on the consumer side and QuickBooks for SMEs — are deeply entrenched and enjoy enormous trust among users who rely on reliable financial software.

With the advancement of AI over the last couple of years, Intuit has stopped being just an accounting software company and has evolved into an integrated, AI-driven financial platform. QuickBooks, TurboTax, Credit Karma, and Mailchimp became increasingly connected within a broader ecosystem.

Unlike many corporate software peers whose demand depends heavily on discretionary IT budgets, a meaningful portion of Intuit’s business is tied to a near-mandatory need: filing taxes. As a result, TurboTax started to resemble a financial utility for consumers.

Prior to the recent sell-off, Intuit was generating gross margins of nearly 81%, operating margins around 27%, and revenue growth in the mid-teens based on its trailing 12-month performance. That is exactly the kind of combination the market tends to reward in a premium software company: top-line growth, high profitability, and strong cash generation.

When the Market Started Questioning the Moat

Then came 2026, and with it the SaaSpocalypse — a period when the market began aggressively questioning the value and durability of software/SaaS moats in the age of generative AI. Intuit quickly became one of the symbols of that reset.

All of this accelerated dramatically following the evolution of models such as Anthropic’s Claude and OpenAI’s ChatGPT. The fear was quite obvious. If a Large Language Model (LLM) can understand natural language, analyze documents, fill out forms, and answer tax-related questions, why would consumers keep paying for TurboTax?

The concern was more than plausible. After all, AI agents handling accounting and administrative tasks have become increasingly common over the past several months. Even if this narrative is somewhat simplistic, it is exactly the kind of fear that can compress valuation multiples quickly, especially for a stock trading at highly stretched levels, such as roughly 65x trailing earnings in August of last year.

The Quality of Growth Starts to Deteriorate

Things started to deteriorate for Intuit after the company’s recent figures — more specifically, its Q3 results. It gave at least some validation to fears surrounding potential moat erosion. Management effectively confirmed a weaker version of the bear case, particularly through a less clean growth profile.

The April quarter, which is seasonally the company’s most important quarter due to the tax season, delivered revenue of $8.55 billion, up 10% year-over-year, below the 15% growth posted in the same period last year. That being said, Intuit delivered an earnings beat, surpassing earnings per share (EPS) estimates by $0.23, or roughly 1.8% above consensus, while revenue came in only about $21 million ahead of expectations.

Perhaps more concerning than the already expected normalization in Intuit’s growth was the quality of that growth. TurboTax disappointed on the low end, growing just 7% year-over-year, while management acknowledged pressure among price-sensitive DIY filers. Meanwhile, the broader Consumer platform grew 8% year-over-year.

At the same time, while revenue grew roughly 10% year-over-year, operating income increased only about 8%, partly reflecting cost-of-revenue growth that continued to outpace the top line, pressuring the operational leverage thesis. That matters because a key part of the bullish AI thesis was the expectation that Intuit would become structurally more efficient through automation.

A Restructuring at the Worst Possible Time

The workforce reduction of roughly 3,000 employees, announced just ahead of Intuit’s earnings release — on the very same day — made the story even harder for investors to interpret. Management framed the roughly 17% headcount reduction as an efficiency-driven move to simplify organizational layers and reallocate investments from slower-growing areas, such as Mailchimp.

The main issue, however, was the timing, especially in the middle of the SaaSpocalypse. Investors were unwilling to give Intuit the full benefit of the doubt. A large restructuring plan, combined with pressure in low-end DIY tax and weaker Mailchimp trends, made the quarter look less like a clean beat-and-raise and more like a business entering a more difficult transition phase.

A Broken Stock, Not a Broken Business?

For a company that had long been viewed as a premium compounder, what Intuit disclosed in Q3 did not exactly resonate as a “best-in-class software story,” even though there was still nothing that materially proved that AI is actively disrupting TurboTax or QuickBooks.

Importantly, Intuit still raised its full-year guidance, even though the increase was not enough to fully offset investor concerns. The company lifted its FY26 revenue guidance by roughly $266 million at the midpoint, non-GAAP operating income guidance by about $145 million, and non-GAAP EPS guidance by roughly $0.75.

With that in mind, consensus now expects Intuit to deliver FY26 adjusted EPS of roughly $23.60, representing about 17% year-over-year growth. If that number proves accurate, INTU would be trading at near 16.3x forward earnings — roughly 34% below the software industry average of 25x, and more than 72% below its own five-year historical average of about 58x.

Furthermore, consensus still expects Intuit to grow both revenue and EPS in the mid-to-low teens over the next five years — numbers that, at least for now, still do not support the narrative of a structurally broken business or a collapsing moat.

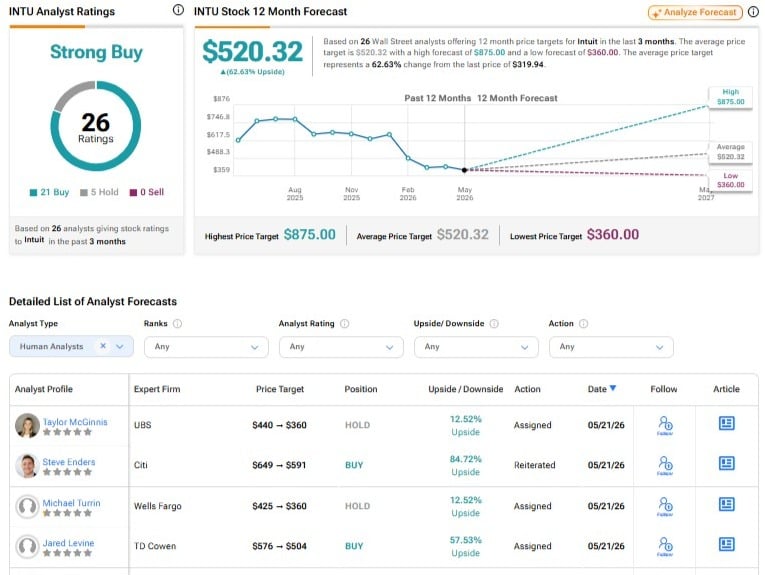

Is INTU a Buy, According to Wall Street Analysts?

Wall Street’s consensus on Intuit remains a Strong Buy. Among the 26 analysts who have covered the stock over the past three months, 21 rate it a Buy, while only five recommend Hold. Although several analysts lowered their price targets following the Q3 earnings report, the average price target for INTU still stands at $520.32, implying potential upside of roughly 63% from current levels.

Too Much Fear, Not Enough Deterioration

Following a significant valuation reset, I now see Intuit stock as a buying opportunity. In my view, the Q3 earnings report and the surrounding headlines do justify a less euphoric valuation range for INTU. However, the magnitude of the sell-off still seems inconsistent with a company going through a normalization phase of its growth profile, rather than one facing a structural collapse.

What ultimately keeps me bullish is that the bear case still appears far more narrative-driven than numbers-driven. As long as Intuit continues to grow both revenue and earnings at a double-digit pace while trading at a deep discount to its own historical valuation and the broader sector, I believe the risk/reward has shifted meaningfully back in favor of investors.