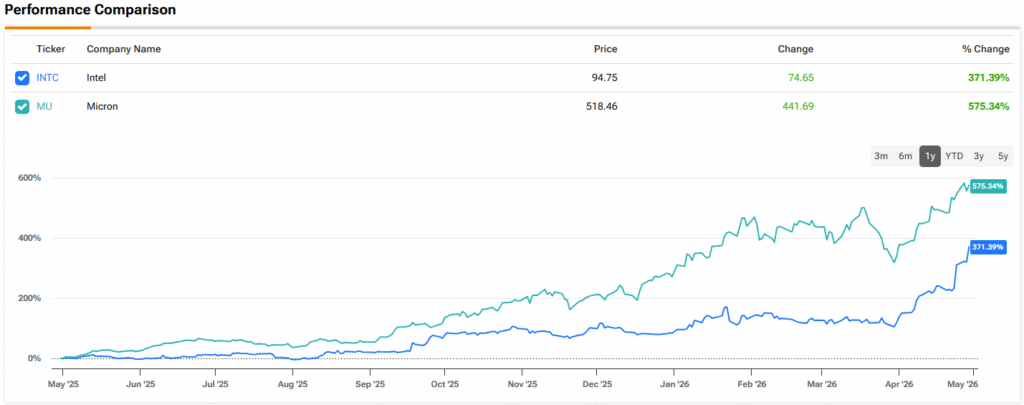

Two of the hottest stocks of the past year are ones that not long ago hardly set investors’ hearts racing, each for a different reason. One is Intel (NASDAQ:INTC), until recently considered a fallen chip giant, weighed down by mismanagement, its dominance eroded in the CPU segment and its AI products not seen as competitive enough. However, investors have been buying into its turnaround story in a big way. Furthermore, the company recently released Q1 results and a guide that blew past Street expectations. All of that has helped the stock surge by 371% over the last year.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Then there is Micron (NASDAQ:MU), which operates in the computer memory industry, a segment known to be highly cyclical, defined by boom-and-bust periods. However, AI’s insatiable demand for memory has been something of a game changer for the industry, a development Micron has taken full advantage of. The company has been generating unprecedented sales and profits, and that has helped the stock climb by a huge 575% over the last year.

But with both these names at elevated levels, which one presents a better case right now?

Morgan Stanley’s Joseph Moore, an analyst ranked among the top 2% on Wall Street, likes Intel’s cost reductions, tighter discipline around capex, a renewed emphasis on products, and a more grounded outlook on foundry and AI opportunities. Recent moves like the partnership with Nvidia are encouraging, but even though both management teams stress that the priority is product development, particularly NVLINK/CPU integration, Moore notes that bulls have been quick to jump to the conclusion that a foundry element will follow.

Meanwhile, the equity issued to the government effectively amounted to Intel selling shares to finance CHIPS Act funding that had already been allocated. Even so, Moore concedes that the “music is likely to keep playing for a while,” as there are no clear signs of supply catching up with demand. However, that is not enough to get him on board.

“We just see better risk reward in areas such as memory that do not have Intel’s market share concerns, where we feel more comfortable on duration, and where we see balance sheet transformation,” the 5-star analyst went on to say. “We just don’t have that conviction for Intel at these levels.”

Accordingly, Moore rates INTC stock as Equal-weight (i.e., Neutral), while his $73 price target points to one-year losses of 22%. (To watch Moore’s track record, click here)

Micron, on the other hand, is where Moore sees a more compelling setup – and it comes down to a structural shift in how the memory market behaves. The old playbook, built around cyclical peaks and inevitable downturns, may no longer apply.

“Our view is that looking for sell signals from prior cycles misses the point – this is not only likely to be durable as long as AI spending is maxed out, at this point based on our industry conversations we think that memory is one of the biggest gating factors on how much AI spending is possible,” Moore said.

For the past three years, Moore pushed back on that argument because there was clearly excess capacity in DRAM, but that surplus has now been absorbed. AI workloads are consuming so much DRAM that there is limited supply left for other end markets, and it is increasingly evident that memory has become a “true bottleneck.” While higher capex will eventually bring additional supply online, the demand backdrop has fundamentally shifted. This is no longer driven primarily by PC, smartphone, and server markets growing at 3–5%. Instead, AI-related spending is expanding at rates above 50%, potentially significantly higher based on commentary from processor companies, and its growing share of total demand is becoming more influential each year.

That shift is why Moore stays bullish on Micron, assigning an Overweight (i.e., Buy) rating. His $520 price target has already been reached amid the recent run, which may warrant a reset, but the broader takeaway is clear – between these two former underdogs, Micron currently offers the stronger AI-driven thesis.

As for the Street’s view, it mirrors Moore’s take. The analyst consensus rates INTC stock a Hold, based on 23 Holds, 9 Buys and 3 Sells, while the $77.27 average price target implies shares will decline by 18% over the one-year timeframe. (See INTC stock forecast)

On the other hand, MU stock claims a Strong Buy consensus rating, based on 27 Buys and 3 Holds. At $574.67, the average price target suggests the shares will add 11% in the months ahead. (See MU stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.