Intel (INTC) just had a blowout quarter, but I am not chasing the stock after the recent run. The Q1 results announced on April 23 clearly showed that demand for artificial intelligence (AI) is picking up, especially in data center central processing units (CPUs), and confirmed that Intel is back in the AI conversation. However, following the massive double-digit rally after Q1, much of that improvement now appears to be priced in. As a result, the path forward becomes more dependent on execution.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

About a year ago, when the stock was trading around $20, it would have seemed hard to imagine INTC reaching the high double digits it is trading at today. In this article, I share some insights into the leading semiconductor manufacturer’s recent momentum and explain why I remain more skeptical of the thesis, especially on valuation grounds.

How Intel Fits Into the Next Phase of AI

Over the past two years, the prevailing consensus around the AI story has basically been that it’s all about major large language models (LLMs) like ChatGPT by OpenAI and Microsoft’s (MSFT) Copilot. These models run primarily on graphics processing units (GPUs), and the companies that dominate the GPU market, like Nvidia (NVDA), were the biggest beneficiaries of this first “winner-takes-all” wave. However, that’s really only half the story. Training AI does use a lot of GPUs, but the more important phase comes after that: actual AI inference — think chatbots, enterprise use cases, autonomous systems, and so on.

This is exactly where Intel starts to matter again, through its CPU. If GPUs do the heavy lifting, CPUs come in right after, coordinating tasks and connecting networks, memory, and storage. That’s why CEO Lip-Bu Tan refers to the CPU as the “orchestration layer.” More specifically, during the training phase between 2022 and 2024, workloads were heavily skewed toward GPUs. CPUs mostly served as feeders, with roughly one CPU per six to eight GPUs.

As we move into inference and deployment, with more simultaneous requests, more data movement, and more coordination, the need for CPUs increases. This results in the CPU-to-GPU ratio starting to shift closer to 1:4, or even more CPU-heavy, depending on the workload.

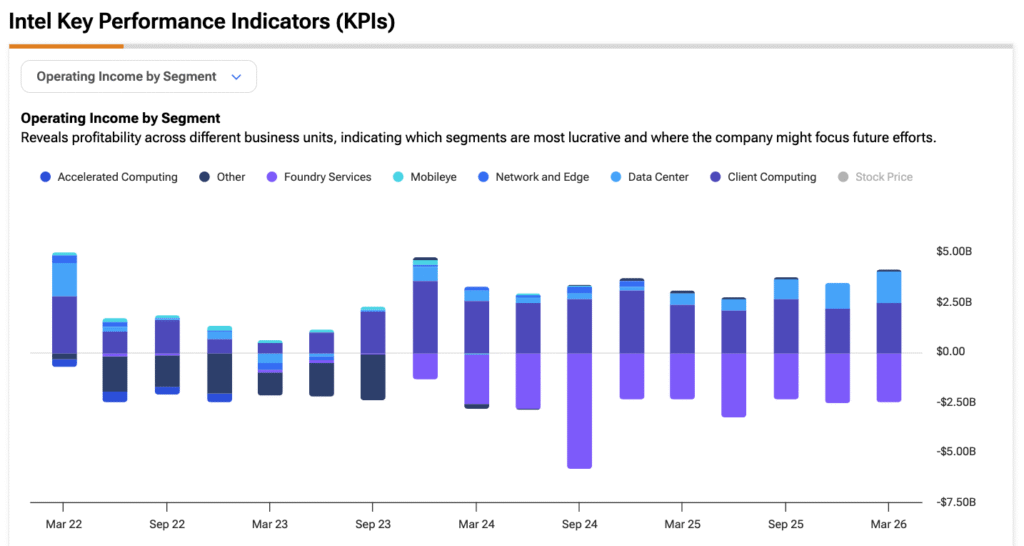

This is the stage where Intel fits in. The company dominates the data center CPU market with its Xeon franchise, particularly the Xeon Scalable family used across hyperscale data centers. That means it is directly exposed to this shift. This is already showing up in the numbers. In the most recent quarter, the sharp growth in Intel’s data center segment supports management’s view that demand for CPUs is running well ahead of supply.

The result is not just pricing power that supports margins, but also upside in volume, as Intel remains supply-constrained. That combination — higher pricing and higher volumes — creates operating leverage, meaning profitability can scale much faster than revenue from here.

What Drove Intel’s Post-Earnings Rally

Intel’s Q1 results were so well received by the market this time because the company managed to do three key things. First, it reported figures well above the high end of its own guidance for both revenue and earnings per share (EPS). On the top line, Intel delivered $13.58 billion, while consensus was roughly 9% lower. In terms of EPS, the $0.29 print was a clear beat versus nearly breakeven expectations.

The second point is margins. Intel posted non-GAAP gross margins of 41%, up 1.8 percentage points. While that may sound modest, the market tends to react strongly to margins in semiconductors — especially in Intel’s case. The company has been dealing with chronic margin pressure due to high foundry costs, node ramp-ups, and so on. So when margins come in above expectations — even with 18A still ramping and typically pressuring margins — it signals better execution than the market thought possible.

The third and final point is guidance. For Q2, Intel expects revenue to reach $14.3 billion at the midpoint, versus a consensus closer to $13 billion. The guided EPS of $0.20, compared to roughly $0.09 expected, also points to improving mix, pricing, and execution. It also suggests the company can still grow sequentially even with supply constraints, as Intel acknowledges it cannot meet all demand.

To support the broader AI infrastructure thesis, Intel reported 22% year-over-year growth in Data Center AI (DCAI) revenue in Q1. Management now expects double-digit growth in server CPU through 2027. Also, even though Intel guided gross margins down to around 39% for Q2, the market largely looked past the sequential decline. It was seen as temporary, tied to the 18A ramp, especially after Q1 suggested a higher underlying run rate.

How to Think About Intel’s Valuation after the Rally

Now, after the rally, Intel is trading at a forward P/E of roughly 80x. Yet arguably, that’s not the best way to look at the investment thesis. EPS remains depressed, margins are not yet normalized, and the foundry business continues to eat into a meaningful portion of profits.

A more appropriate approach, in my view, is to focus on normalized earnings power. In other words, estimate what Intel can earn in a reasonable — not perfect — scenario. Right now, estimates point to roughly $1 in EPS for FY26 and potentially around $2.1 by FY28. At a share price of $85, that implies a forward P/E of about 38.4x on those FY28 earnings.

The key question, then, is whether paying roughly 38x earnings two years out makes sense for a company like Intel. Doubling EPS over that period is clearly strong growth. However, the quality of those earnings still depends on execution, which is very much a work in progress. Intel today is arguably not yet a premium business.

To me, the market is now more confident that margins will improve, that earnings growth will accelerate, and that execution will remain on track. Even so, looking out to FY28, the path to justify that valuation still looks demanding.

Is INTC a Buy, Sell, or Hold, According to Wall Street Analysts?

The consensus on Intel shares remains quite divided among Wall Street analysts, with the stock currently rated Hold. Of the 35 ratings issued over the past three months, only nine are Buys, while 23 are Holds and three are Sells. The average price target stands at $77.27, implying roughly 9.09% downside from the current share price.

Where Things Stand for Intel

Intel’s recent earnings report leaves little doubt that the company is back in the AI conversation. The demand backdrop looks very strong, with Data Center AI revenue growing at a double-digit pace and management signaling that CPU demand is outpacing supply. At the same time, execution is clearly improving, with gross margins coming in well above expectations even as the 18A node is still ramping.

Even so, the bar has now been raised significantly. Intel is trading at a premium and still relies heavily on continued execution to justify those multiples. That leaves the upside looking more limited, so I lean toward a Hold stance on the stock.