When corporate insiders start buying shares hand over fist, investors tend to pay attention. After all, these are the executives and board members with the clearest view into a company’s operations, momentum, and long-term prospects. And while insiders can sell stock for all sorts of reasons – taxes, diversification, estate planning – they usually only buy for one reason: they believe the shares are headed higher.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

That’s especially true when the purchases aren’t small. Million-dollar buys are often viewed as a stronger signal because they suggest executives are willing to commit meaningful amounts of their own capital based on their confidence in the company’s outlook and future prospects.

With that backdrop in mind, we turned to the TipRanks Insider’s Hot Stocks tool to screen for companies seeing significant recent insider buying activity. The result was a group of stocks that not only attracted large insider purchases, but also boast Strong Buy consensus ratings from Wall Street analysts alongside sound upside potential. Here’s a closer look at three names standing out right now.

T-Mobile US (TMUS)

We’ll start with T-Mobile, one of the largest telecom companies in the US market – and in the world. By market cap, T-Mobile’s $209 billion valuation ranks at the top of the ladder in the US, and second from the top globally; the company realized $88.3 billion in revenue last year, putting it in fourth place in the US and seventh on the world scene.

That’s an impressive position to hold in a multi-trillion-dollar industry, and T-Mobile earned it by the simple process of offering its customers what they want and need. T-Mobile’s services include a wide range of telecom plans, including plans for mobile phones, home internet, smartwatches and tablet devices, business phone plans, and fiber optic networking plans.

At the end of April, T-Mobile announced that it would be expanding its fiber services to over 1 million additional households nationwide. The expansion will come from the planned acquisition and combination, through a joint venture with Oak Hill Capital, of GoNetSpeed and Greenlight Networks, as well as a second joint venture with Wren House to acquire i3Broadband. The transactions are expected to all be closed by next year, and T-Mobile plans to invest as much as $2.7 billion in these network expansions.

At about the same time that T-Mobile announced its fiber expansion plans – the end of April – the company also announced its 1Q26 financial results. T-Mobile’s total revenue in the first quarter, $23.1 billion, was up more than 10% year-over-year and beat the forecast by $91.7 million. The company reported a diluted earnings per share of $2.27, down 12% year-over-year but 30 cents per share better than had been anticipated. The adjusted free cash flow was up 5% from the prior-year first quarter, at $4.6 billion, and represented industry-leading growth.

Turning to the insider trades on this stock, we find that Andre Almeida, T-Mobile’s Chief Broadband, Enterprise, and Emerging Business officer, spent almost exactly $1 million to pick up 5,097 shares of TMUS last Friday. This brings his total stake in the company to about $8.7 million.

That’s the kind of move Scotiabank analyst Maher Yaghi can appreciate, as he believes T-Mobile remains well-positioned to keep delivering steady revenue and earnings growth in the periods ahead.

“Q1 reinforced a familiar setup with the company continuing to pair postpaid growth with network monetization, and that combination is translating into industry leading service revenue and EBITDA growth. For a market that is increasingly discriminating between telcos that can grow and telcos that can produce FCF, T-Mobile continues to do both. Q1 supports our thesis on the stock as customer acquisition costs continue to be well calibrated against customer lifetime value. ARPA growth and churn dynamics will be key for us in the coming quarters indicating if promotional intensity is heating up. TMUS has so far responded well to increased promotional intensity relying on its network leadership and strong NPS scores to maintain good economics,” Yaghi wrote.

Quantifying that stance, Yaghi rates TMUS stock as Outperform (i.e., Buy), and sets a price target of $263 to imply a one-year upside potential of 36%. (To watch Yaghi’s track record, click here)

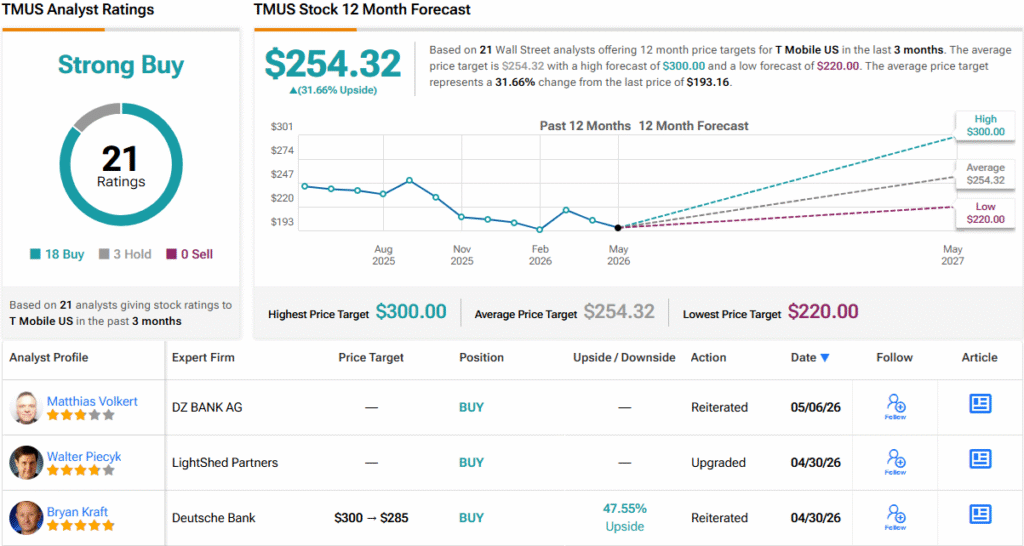

The 21 recent analyst reviews here break down to 18 Buys and 3 Holds, for a Strong Buy consensus rating. The stock is priced at $193.16, and its $254.32 average price target suggests a gain of ~32% in the coming year. (See TMUS stock forecast)

S&P Global (SPGI)

The second stock on today’s list of insider buys is S&P Global, one of the financial world’s most recognizable names. It is the holding company behind both the S&P 500 and Dow Jones stock indexes. S&P Global is the successor company to McGraw Hill and has been providing financial services, including market research, since 1860. At its core, S&P’s business is data – providing market data, from the most basic financial information to the high-level analysis that steers investors to the intelligence that drives commodities markets.

The key to its success has not just been delivering accurate market research and data, but also maintaining a broad and diversified range of services. S&P Global caters to financial institutions around the world, providing solutions for credit and risk management, commercial prospecting, global banking, insurance, real estate, and regulatory compliance. The company has built a reputation for giving businesses and investors the information they need when they need it.

We should note here that shares in SPGI took a hard hit this past February. The company reported, in its 4Q25 results, lower-than-expected earnings guidance for 2026. Specifically, the full-year EPS midrange guidance, as given, was $19.53; this was well below the consensus figure of $19.96.

However, the company’s latest quarterly report helped calm some of those concerns. S&P Global released its 1Q26 results at the end of April and delivered beats on both the top and bottom lines. Revenue came in at $4.17 billion, up 10% year-over-year and $98.9 million ahead of expectations, while adjusted diluted EPS of $4.97 topped estimates by 15 cents per share. Yet, despite the strong report, SPGI shares are still down ~19% this year.

The pressure on the stock has done little to scare off insiders. In fact, it may have had the opposite effect, with several of the company’s top executives stepping in to buy sizable blocks of shares. Three insiders – Martina Cheung, CEO & President; Catherine Clay, CEO of the S&P and Dow Jones indexes; and board member Robert Moritz – each purchased more than $500,000 worth of stock between late April and early May. Moritz made the smallest purchase, picking up 1,152 shares for $500,000, while Clay acquired 2,500 shares for just over $1 million. Cheung was close behind, spending nearly $1 million to buy 2,322 shares.

In coverage for RBC, analyst Ashish Sabadra notes S&P Global’s overall strengths, saying of the company, “Average deal size is expanding, reflecting both deeper penetration with existing customers and improved pricing realization. Together, these factors—coupled with anticipated acceleration in net sales—position subscription growth to meaningfully re-accelerate in 2Q26. The combination of improving unit economics, robust pipeline, and disciplined pricing execution suggests the 1Q26 deceleration is largely transitory, with visibility into near-term recovery.”

Put into a recommendation, Sabadra’s stance adds up to an Outperform (i.e., Buy) rating, which is complemented by a one-year price target of $560, suggesting a sound upside of 32%. (To watch Sabadra’s track record, click here)

Overall, S&P Global has earned a unanimous Strong Buy analyst consensus rating, based on 17 positive reviews set in recent weeks. The stock is currently priced at $423.57 and has an average price target of $534.07; together, these figures imply that a 26% gain lies ahead for the stock this year. (See SPGI stock forecast)

Sportradar Group AG (SRAD)

Last on our list here is Sportradar Group, a Swiss-based sports tech company that develops immersive experiences for sports fans and bettors. The company has been in the business since 2001, and it provides tech services across the sports industry to teams, leagues, betting concerns, and media. In all, Sportradar covers over one million popular sporting events annually.

The core of Sportradar’s business is its database, built up through a series of long-term partnerships with leaders in the sports and sports betting industries. These names include such storied leagues as the NBA, Major League Baseball, NASCAR, the PGA Tour, the NHL, and Euroleague Basketball, as well as betting and fantasy league providers like FanDuel and DraftKings or media giants like ESPN. Every sports-related business requires up-to-date data – it’s essential, you can’t follow the leagues without it – and Sportradar provides the latest in-game results and league standings, player stats, and even the odds and futures on the betting side.

Sportradar complements its data services by providing customer platforms in the betting industry to support iGaming and sports betting. The company’s flexible platforms allow customers – betting vendors – to select any set-up from single sportsbook modules to full turnkey solutions. The platforms cover sports betting, iGaming options, and a wide range of online lotteries and digital casino gaming. Sportradar boasts that its betting platforms can be customized to make them relevant to providers’ local conditions.

This stock has been falling all year, and for the year-to-date, it is down ~44%. Factors putting pressure on SRAD shares include an earnings miss on the Q1 financial results and, earlier in April, allegations that the company was knowingly serving illegal betting venues. That allegation brings with it serious legal and/or regulatory repercussions.

In a show of confidence, however, the company’s CEO Carsten Koerl and Board member Marc Walder both made large purchases at the end of April and the start of May. Koerl’s purchase, in two blocks totaling 254,100 shares, was the larger, and cost him about $3.34 million. Walder spent nearly $843 thousand on 66,000 shares of SRAD.

That insider activity also lines up with the view from Canaccord analyst Jason Tilchen, who argues that Sportradar’s depressed valuation now presents one of the best entry points the stock has offered in quite some time, particularly given the company’s history of meeting deliverables.

“SRAD is currently trading at ~8x FY26 EBITDA, the lowest levels in its nearly five years as a public company, and we continue to feel the current valuation does not properly reflect Sportradar’s track record of execution nor its critical role in the global sports ecosystem. The core business set to deliver consistent margin expansion & strong cash flow generation going forward, while prediction markets and the recent expansion into iGaming products provide upside to estimates over time,” Tilchen commented.

That outlook underpins Tilchen’s Buy rating on the shares. His $28 price target suggests the stock could climb about 110% over the next year. (To watch Tilchen’s track record, click here)

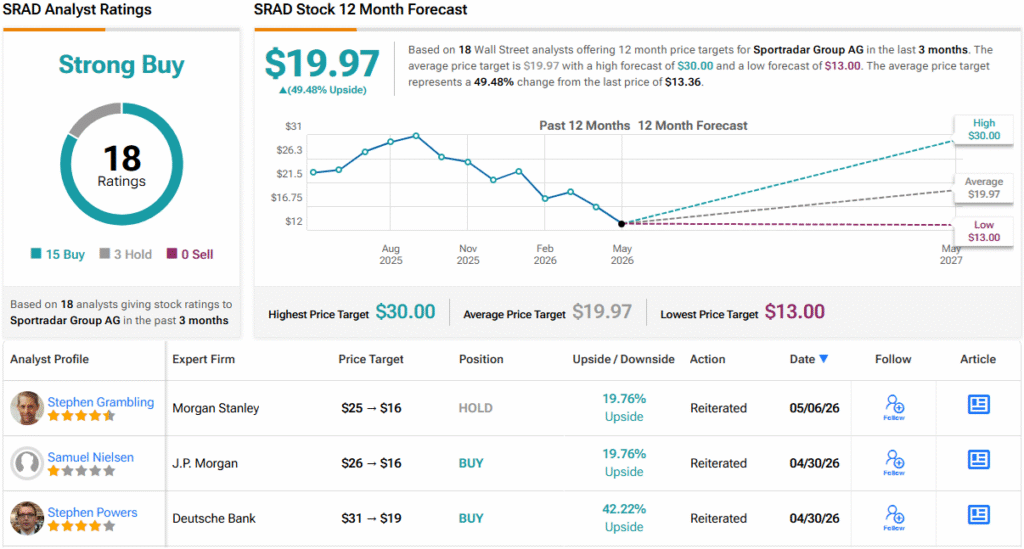

Tilchen’s target is on the higher end; yet, the broader Street remains constructive as well. Among 23 recent analyst reviews, 18 rate the stock a Buy while 5 recommend Hold, giving SRAD a Strong Buy consensus rating. With shares currently trading at $13.36, the average price target of $20.50 implies upside potential of 49% over the coming 12 months. (See SRAD stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.