Indie Semiconductor (INDI) is a unique player in the automotive sector, focusing on advanced driver assistance systems, connected cars, and electric vehicle (EV) applications. With its comprehensive suite of sensor solutions and growing partnerships with global OEMs, Indie is well-positioned to capitalize on the booming automotive semiconductor market, expected to surpass $130 billion by 2029. Despite a challenging market environment, driving the stock down over 56% year-to-date, the company projects profitability by 2025, and analysts are bullish on the stock’s potential for significant growth.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

However, significant upside potential does not eliminate risks, and Indie must demonstrate strong execution to meet these ambitious growth targets. The stock appears undervalued, presenting an opportunity for investors seeking high-risk, high-potential return exposure to the semiconductor industry.

Indie Semiconductor Looks to Differentiate Itself

Indie Semiconductor provides automotive semiconductors and software solutions essential for various advanced vehicle applications. Its solutions range from ultrasonic sensors for parking assist systems to LiDAR installed for obstacle detection. The company caters to global clients across South America, North America, Greater China, South Korea, Asia Pacific, and Europe.

Indie’s strategic focus on product development, securing key design wins, and partnerships with leading global OEMs position it to capitalize on the industry’s promising market trends. The company is currently the only chip vendor to offer all four crucial Advanced Driver-Assistance System (ADAS) sensors: radar, vision, LiDAR, and ultrasound. The company differentiates itself from the competition by offering any combination of these sensors and being able to contribute to scalable ADAS processing architectures that carmakers require.

Despite the current subdued automotive climate, Indie anticipates substantial opportunities in the medium to long term. Projections suggest that the total value of automotive semiconductors could exceed $100 billion in 2026 and surpass $130 billion in 2029.

Indie Semiconductor’s Recent Financial Results

The company recently released its second-quarter results for 2024. Revenue was $52.36 million, slightly below the analysts’ expectations of $53.70 million, with a non-GAAP gross margin of 50.3 percent. The company’s operating losses of $36.6 million marked a decline compared to the $40.7 million in the same period of the previous year. Earnings per share (EPS) were -$0.09, which aligned with consensus expectations.

Following its second-quarter results, INDI’s management has issued guidance for the third quarter, projecting a revenue rise within a 0% to 5% range and an approximate gross margin of 50%. With production plans for its Radar and Vision programs on track, Indie anticipates a return to its industry-leading growth trajectory in 2025 and the following years.

What Is the Price Target for INDI Stock?

The stock had been relatively range-bound the past few years before breaking downward and shedding 52% in the past three months. It trades at the low end of its 52-week price range of $3.73 – $8.69 and demonstrates negative price momentum as it trades below its 20-day (4.28) and 50-day (5.02) moving averages. However, the price decline has driven the stock into deep value territory, with a P/S of 2.4x, well below the Semiconductor Equipment & Materials industry average of 6.5x.

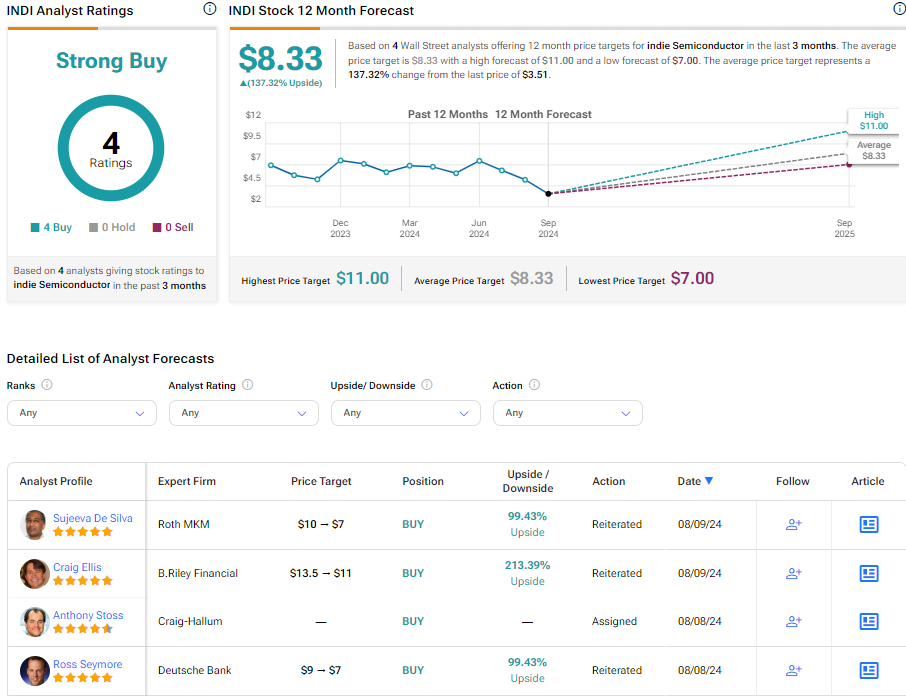

Analysts following the company have been bullish on INDI stock. Roth MKM analyst Sujeeva De Silva, a five-star analyst according to Tipranks’ ratings, recently reiterated a Buy rating on the shares while lowering the price target from $10 to $7, noting the firm’s second-half outlook is dampened by falling global auto/EV demand with a revenue bounce anticipated in 2025.

Based on four analysts’ recommendations and price targets, indie Semiconductor is rated a Strong Buy. The average price target for INDI stock is $8.33, representing a potential upside of 137.32% from current levels.

INDI in Summary

Despite a challenging market environment, indie Semiconductor remains optimistic, projecting profitability by 2025 due to its strategic focus on product development and strong partnerships with global OEMs. The stock is undervalued relative to industry peers, suggesting an opportunity for value-oriented investors eyeing risky but potentially high-return semiconductor industry exposure.