Alphabet (NASDAQ:GOOGL) saw its ongoing battle with lawmakers escalate last week after the Justice Department confirmed it is pushing for the company to spin off its dominant Chrome web browser. Rumors had circulated that the DOJ might seek to separate the browser, and the department’s filing last Wednesday made it official. This follows Google’s antitrust trial, where the company was found to have maintained an illegal monopoly in search and search ads.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

This isn’t the only step the DOJ might take. It’s also considering significant changes to how Google search operates on the company’s Android mobile platform and wants an end of payments to Apple. The remedies trial is set for April and Google is expected to respond to the DOJ’s proposals before the year wraps up.

The news sent Alphabet stock tumbling, but Baird’s Colin Sebastian, an analyst ranked in the top 4% of Wall Street stock experts, thinks plenty of the DOJ’s recommendations are “unlikely to be approved by the court, or to survive an appeals process.”

“Beyond the reasonable ask to prohibit search distribution agreements,” the 5-star analyst goes on to say, “the DOJ remedies are, in our view, a wish-list of restrictions on Google that stray well beyond the court’s ruling.”

For instance, the DOJ’s call for Chrome to be sold is unlikely to find favor with the court, appearing to Sebastian as “very punitive compared to simply prompting users to pick their default search engine.” Sebastian thinks that the DOJ might have proposed this measure because user choice initiatives in Europe have had little effect on reducing Google’s search market share.

The most “egregious of the government’s requests” are those that demand Google share its core search index, user data, and ad insights with rivals. The DOJ is also requesting that Google be required to share its search results, ranking algorithms, and query processing capabilities with rivals for a period of ten years.

“In our view,” says Sebastian on the matter, “this could be a textbook definition of government over-reach, and in a ‘worst-case scenario,” not only would hand over much of Google’s proprietary search capabilities to competitors, but also risks degrading the quality of Google’s search results. We do not expect the court to approve this remedy.”

It’s interesting to note that the original lawsuit was filed under the first Trump administration, so what will be the new administration’s stance here? Trump is no fan of Google, having recently said search results were biased against him, and he threatened criminal action over “bad stories.” However, Trump’s current stance on Google is unclear.

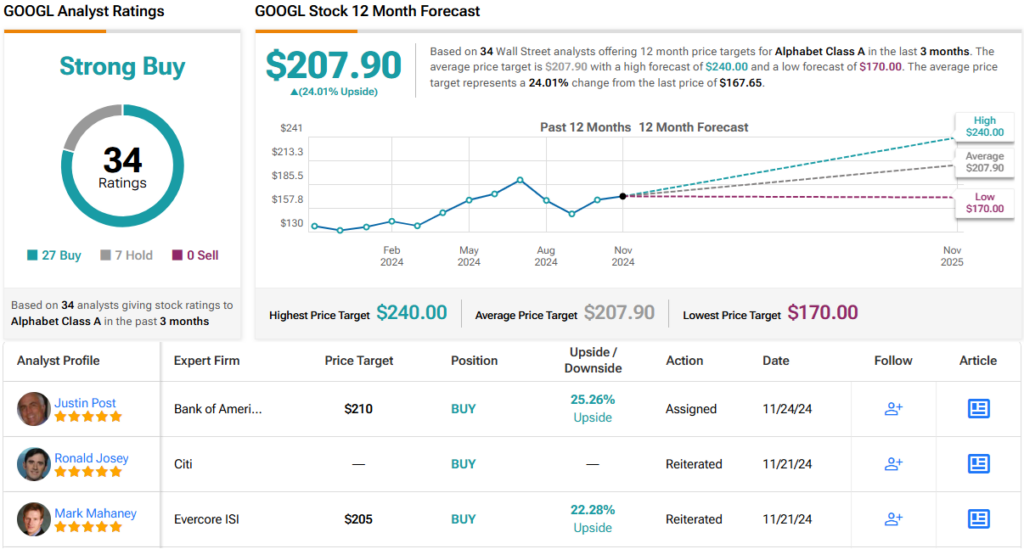

All that said, Sebastian remains a GOOGL bull, giving the stock an Outperform (i.e., Buy) rating, along with a $205 price target. If the target is achieved, and based on the last closing price of $167.65, GOOGL shares could provide a potential return of ~22% over the next 12 months. (To watch Sebastian’s track record, click here)

That target is just a little lower than the Street’s average, which stands at $207.90 and implies ~24% upside from current levels. All in, based on 27 Buys and 7 Holds, the analyst consensus rates this stock a Strong Buy. (See GOOGL stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.