The market has spent the past few years obsessing over the AI GPU boom, with those chips becoming some of the most sought-after products in tech. But Advanced Micro Devices (NASDAQ:AMD) recently reminded investors there’s another highly profitable opportunity gaining momentum alongside it.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

That opportunity is the server CPU market, which CEO Lisa Su said is expected to grow at a 35% CAGR and reach $120 billion by 2030. AMD is already preparing for that expansion, with Su noting the company is increasing both wafer supply and back-end capacity to meet the anticipated surge in demand.

Su is not the only executive pointing in that direction. Intel CEO Lip-Bu Tan echoed a similar view during the company’s recent earnings call, reinforcing the growing belief that server CPUs could become one of the semiconductor industry’s next big growth engines.

So why does all of this matter for AMD stock? According to top investor Stone Fox Capital, this is precisely where the company’s next leg higher could come from.

In fact, it’s not only the “huge” CPU opportunity that has the investor bullish, though Stone Fox believes AMD’s server CPU revenue could climb 10x by 2030. The bigger point may be that expectations still appear surprisingly restrained, with Wall Street currently projecting revenue of “only” $75 billion for 2027 despite the scale of the AI and datacenter buildout now underway.

Indeed, Stone Fox assesses that upside from AMD’s deals with OpenAI and Meta Platforms – plus the additional CPU demand – puts the company within striking distance of $100 billion in sales next year (and not 2028 as analysts are predicting).

Moreover, Stone Fox sees a realistic path for AMD to “soar past” $175 billion by 2030, even potentially reaching $200 billion. The investor calculates that AMD’s share price could hit $600 based on a price-to-earnings multiple of 20x, whereas it could go much higher if the valuation inches further upward.

“My investment thesis remains ultra bullish on the stock,” said Stone Fox, who ranks among the top 4% of stock pros tracked by TipRanks. Unsurprisingly, the investor maintains a Strong Buy rating on AMD shares. (To watch Stone Fox Capital’s track record, click here)

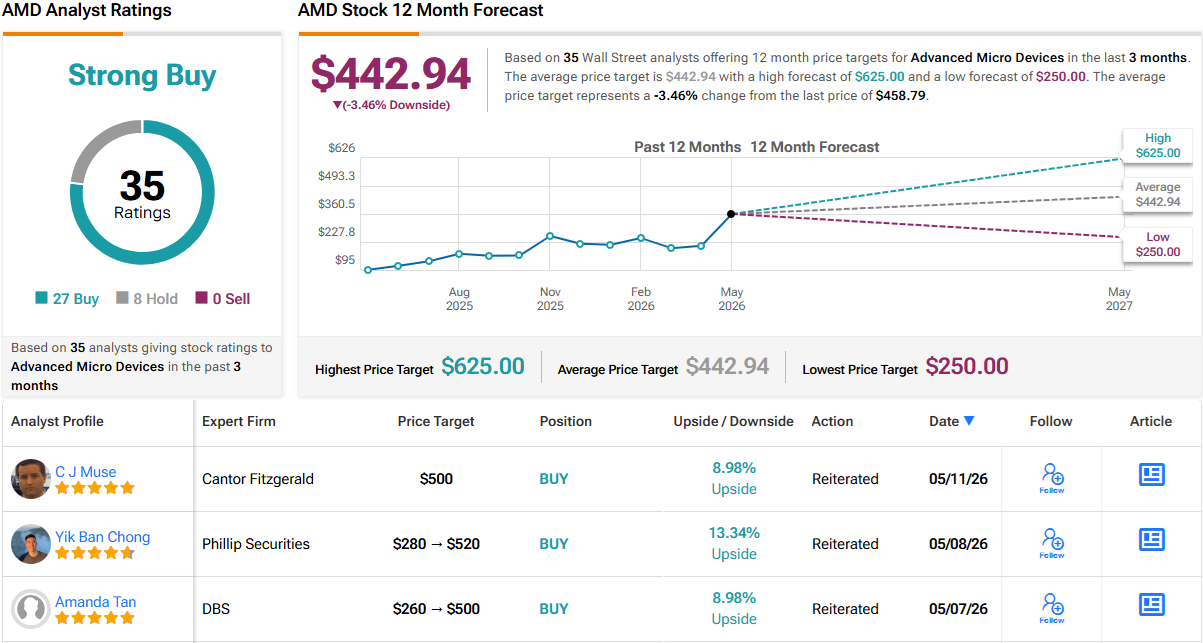

Meanwhile, Wall Street finds itself at a bit of a crossroads. Though 27 Buys and 8 Holds combine to give AMD a Strong Buy consensus rating, its 12-month average price target of $442.94 implies modest downside from current levels. (See AMD stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.