Norwegian Cruise Line (NCLH) sank 9% on Monday after the company slashed its full‑year 2026 outlook, citing weakening consumer demand, higher fuel costs, and mounting geopolitical uncertainty. The cruise operator now expects adjusted EPS to be between $1.45 and $1.79, well below its prior forecast of $2.38 and under Wall Street’s roughly $2.10 consensus.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The company also lowered its expectations for 2026 net yield, now projecting a 2.7% to 4.7% decline versus an earlier outlook for a slight 0.4% increase. Management noted that Norwegian entered the year behind its targeted booking curve, pointing to earlier “execution missteps” that left the company playing catch‑up.

The weaker outlook overshadowed an otherwise solid quarter. The company reported a Q1 adjusted EPS of $0.23 that jumped 228% and beat expectations of $0.14 per share. Also, revenue rose 9.6% to $2.33 billion, slightly below the $2.36 billion analysts were expecting.

Efficiency Gains Clash with Softer Demand and Margin Pressure

CEO John Chidsey said Norwegian has been working to stabilize performance, cutting an estimated $125 million in annual run‑rate costs through efficiency initiatives. These savings are intended to offset near‑term pressures, including elevated fuel prices tied to disruptions in the Middle East.

However, cost cuts alone are not enough to counter the broader demand slowdown. Norwegian said consumers are reevaluating travel plans to Europe and the Middle East as regional conflict escalates, weighing on bookings and pricing. Higher fuel expenses are also likely to squeeze margins throughout the year.

Is NCLH a Good Stock to Buy Now?

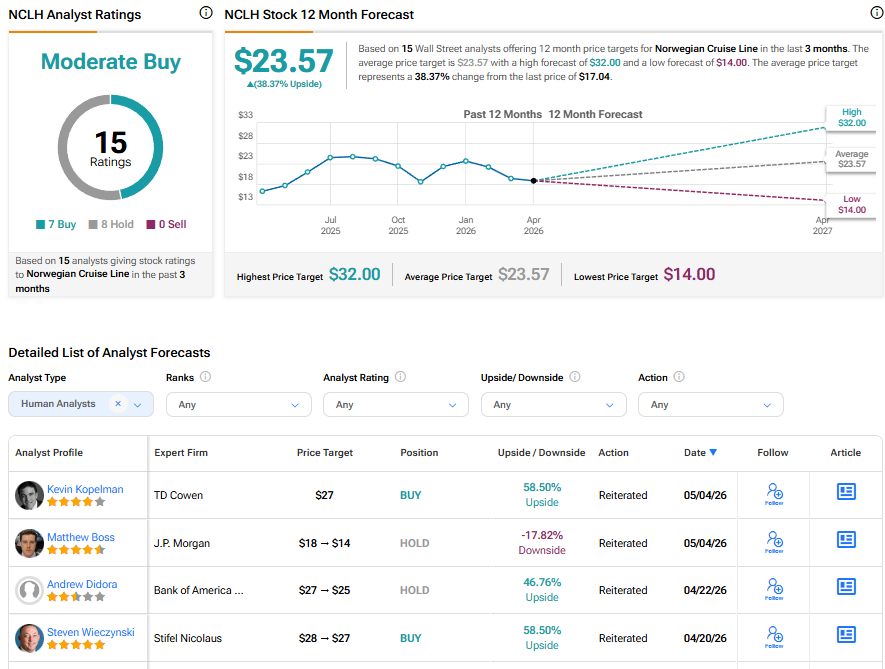

Turning to Wall Street, analysts have a Moderate Buy consensus rating on Norwegian Cruise Line stock based on seven Buys and eight Holds assigned in the past three months. Further, the average NCLH price target of $23.57 per share implies 38.37% upside potential.