Chinese automaker BYD (BYDDF) recently reported a drop in its passenger vehicle sales for April, marking the eighth consecutive month of decline. Rising competition and lower subsidies have impacted BYD’s domestic sales, while overseas business looks encouraging. That said, following a group call with BYD management, JPMorgan analyst Nick Lai highlighted some positive aspects, including the company’s expectation to deliver higher sales in 2026, driven by an improved domestic market outlook and rapid expansion in international markets. Lai has a Buy rating on BYD with a price target of RMB 120.

Claim 55% Off TipRanks

Looking for exposure to SpaceX & Anthropic? Check out AGIX ETF

It is worth noting that BYD overtook Tesla (TSLA) as the world’s top seller of EVs in 2025. However, there have been concerns about rising competition and price wars in the company’s domestic market.

JPMorgan Analyst Highlights BYD’s Optimistic Outlook

Lai highlighted three key takeaways following the group call:

- BYD management now expects sales volume in its domestic market to be in the range of 3.5 million to 4 million in 2026, reflecting 0-14% growth, depending on the “competitive dynamics” in China. Interestingly, management’s projection is quite optimistic compared to JPMorgan’s estimate of 3.5 million and the market’s consensus estimate of flat to a moderate yearly decline. Lai added that BYD’s outlook range is wide, indicating management’s confidence in strong order flow for newly launched models equipped with the company’s ultra-fast charging solution. BYD showcased new models like the Great Tang six-seater sport utility vehicle at last month’s Beijing Auto Show.

- For the overseas markets, BYD continues to expect 1.5 million units in 2026, reflecting 50% year-over-year growth. That said, management indicated potential upside, driven by strong demand, mainly after the spike in oil prices due to the U.S.-Iran war. Management highlighted that its own eight vessels will be ready to support its targets.

- Lai contends that BYD’s enhanced domestic profitability from new models with flash-charging solutions is not yet evident to investors. He expects more than 30% of sales volume in the domestic market to come from new models (priced above RMB 200K) by Q4 2026. This contrasts with about 70% domestic volume at a price point below RMB 150K in 2025. Overall, Lai noted that higher pricing will help mitigate the impact of cost inflation and price competition.

International business is now a key growth driver for BYD. While the company’s total sales declined for the eighth consecutive month in April 2026, overseas sales surged 71%. Lai expects BYD’s overseas business to contribute about 60% of vehicle revenue this year.

Furthermore, Lai expects industry passenger vehicle demand to recover about 25% to 30% quarter-over-quarter in Q2 2026. Specifically, for BYD, the analyst expects about 60% sequential growth in volumes in Q2 2026. Lai expects volumes to grow by another 60% in the second half of 2026 compared to the first half.

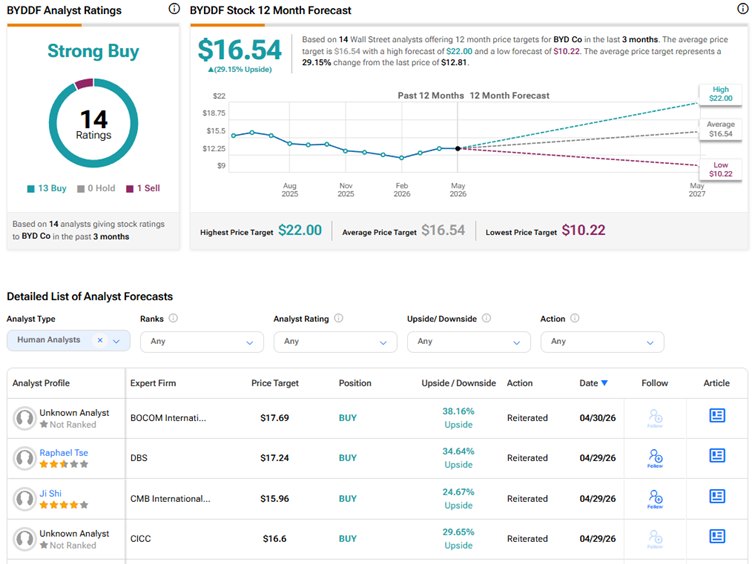

Is BYDDF Stock a Buy, Sell, or Hold?

Wall Street is highly bullish on BYD Company stock, with a Strong Buy consensus rating based on 13 Buys and one Sell. The average BYDDF stock price target of $16.54 indicates 29.2% upside potential. BYDDF stock has risen only 5% so far this year.