Shopify’s (SHOP) post-earnings pullback looks overdone, in my view, as the latest quarter still showed strong execution across the business. Investors are focusing on signs of moderating growth, but the broader story remains intact. Shopify continues to gain scale, deepen its role in commerce infrastructure, and generate growing free cash flow, all of which support the long-term bull case.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

While guidance may have given investors a reason to reset expectations in the near term, I think the market reaction underestimates the durability of the cloud-based e-commerce platform and its growth drivers. That is why I remain bullish on SHOP stock.

Decoding the Market’s Disappointment

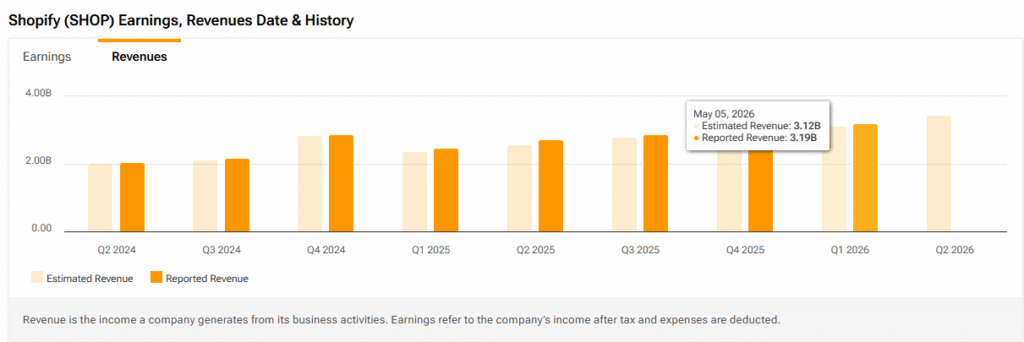

Shopify reported its Q1 results on May 5. Despite posting $3.2 billion in revenue, marking a great 34% year-over-year jump, the stock is currently sliding in pre-market trading. I believe this is a classic case of “perfection not being enough.” The market took one look at the Q2 guidance, which hinted at “high-twenties” revenue growth, and immediately screamed “deceleration.” The very same knee-jerk reaction that can make professional traders roll their eyes is the one that can make long-term investors check their bank balances for spare cash.

The skepticism isn’t entirely baseless, of course. The bears may point to the gross margin trajectory, which saw a nearly 200-basis-point squeeze late last year and continues to weigh on Shopify Payments’ success. Because Payments carries a lower margin than pure software subscriptions, the very thing that makes Shopify essential to its merchants is also what makes the spreadsheets look “messy.”

There’s also the shadow of operating expenses, as management expects it to be around 35%–36% of revenue next quarter. For a market currently obsessed with “efficiency at all costs,” I can understand why that number feels like a pebble in a shoe and is annoying enough to cause a temporary sell-off.

A Juggernaut in Full Flight

However, I believe that the reality panic-sellers might be missing is that Shopify just surpassed $100 billion in Gross Merchandise Volume (GMV) in a single quarter for the first time in its Q1 history. While the “high-20%” guidance for Q2 might look like a slowdown compared to Q1’s 34%, it’s important to remember that Shopify is lapping some of its most aggressive growth periods. Growing a business of this scale at nearly 30% is hardly a “slowdown.” There are a handful of companies that can boast such prolonged and sustained momentum.

I also like that the growth isn’t just more of the same. It is being driven by a massive, structural pivot into the enterprise and wholesale markets. Shopify’s B2B GMV has been exploding as major brands like Nike (NKE), SKIMS, and Supreme shift more of their “heavy lifting” to the platform. Remember that these are complex, multinational operations that use Shopify’s Sidekick, powered by artificial intelligence (AI), to automate workflows and Commerce Components, replacing aging, clunky legacy systems.

When a company becomes the backbone of a $100 billion-per-quarter economy, I believe quarterly “guidance” becomes a distraction from the sheer gravitational pull it exerts on the retail world.

Is SHOP’s Valuation Attractive?

Now, with shares trading around $115, roughly 30%–35% below their 52-week highs, I believe we’re looking at a valuation that finally reflects reality rather than euphoria. In fact, I would argue that at today’s price, the market is not accounting for Shopify’s tremendous cash flow potential. Shopify has now delivered 10 consecutive quarters of double-digit free cash flow (FCF) margins. In Q1, even with all the “noise,” they maintained a 15% FCF margin.

If we look at the full-year numbers, consensus revenue is pegged at roughly $16.3 billion. With a prudent FCF margin estimate of 16%, Shopify is on track to generate upwards of $2.3 billion in free cash flow this year. Sure, that yields a rich P/FCF of nearly 66x. However, for a business growing revenue at 25%–30% and mid-teen FCF margins, the stock should be able to quickly grow into this valuation if execution holds. You also have to consider Shopify’s moat, which warrants a premium on its own.

Is SHOP a Buy, Sell, or Hold?

Despite the stock’s lackluster performance, Shopify still has a Strong Buy consensus rating on Wall Street, based on 28 Buy and five Hold ratings. Notably, no analyst rates the stock a Sell. Further, SHOP’s average price target of $157.64 implies nearly 41% upside potential over the next 12 months.

Final Thoughts

The market is currently punishing Shopify for being honest about the law of large numbers. Nevertheless, it’s apparent that the business’s momentum, whether it’s GMV growth, enterprise wins, or rising free cash flow, is more robust than ever. I’ll take the “weak” guidance discount any day of the week.

At the end of the day, Shopify remains the future of how we buy things. Today, that future might be on sale. Shopify is the undisputed king of the merchant stack, and so I can’t buy into the idea that a single quarter’s guidance can mask a decade of structural dominance. Thus, the post-earnings dip might prove a compelling entry point for those sitting on the sidelines or waiting for a better one.