All eyes are on ‘Hyperscaler Wednesday,’ with the market’s biggest cloud names set to report after the close. Boasting the leading cloud platform in AWS, Amazon (NASDAQ:AMZN) is naturally among them, heading into its Q1 readout at a particularly opportune moment.

Claim 55% Off TipRanks

Trade AMZN with leverageAfter a period in the doldrums, the shares have surged back to new highs. The next move, however, will depend on how quickly AWS can reaccelerate.

RBC’s Brad Erickson, an analyst who ranks among the top 4% on Wall Street, believes this report could be decisive. Following a modest AWS beat last quarter and more encouraging commentary, he sees the upcoming print as a turning point, one that needs to show enough acceleration to justify Amazon’s hefty $200 billion capex plan, a figure that has already outpaced Street expectations.

Erickson thinks that with AWS accounting for roughly one-third of incremental industry spend over the last three quarters, alongside sequential revenue increases of $1 billion for two straight quarters, indicates the business is “hitting its stride.” However, to strengthen confidence in capex returns, investors will likely need to see a more meaningful acceleration beyond the current sub-$1 billion upside.

The bull case hinges on AWS reaccelerating toward the mid-20% growth range or better, driven by a widening pace of revenue outperformance, stronger backlog conversion, and more explicit signals from management on when – and how – the next leg of growth materializes.

The bear case, however, centers on whether Google Cloud’s rapid sequential gains in both revenue and backlog – now at $240 billion and approaching AWS’s $244 billion despite operating at roughly half the scale – suggest rising competitive pressure, with potential share erosion or pricing dynamics that could challenge Amazon’s AI infrastructure leadership thesis.

Elsewhere, with chip revenue surpassing $10 billion and growing at a triple-digit rate in 4Q25, and Trainium 3 capacity likely fully allocated by mid-2026, the Q1 results will serve as a key test of whether AWS’s custom silicon strategy is delivering “durable differentiation” and customer stickiness that can justify its heavy infrastructure spending. Management added 1.2 GW of capacity in Q4, slightly ahead of expectations, and plans to double its footprint by 2027 with further expansion into 2028, underscoring a sustained buildout. The focus now shifts to whether this added capacity is being “absorbed at target utilization rates and pricing.”

There’s also an ongoing debate about ROIC (return on invested capital). AWS maintained strong 35% margins in 4Q25 despite record levels of “capex intensity,” creating a tension where operating performance remains robust, but investor patience is strained by the scale of spending.

“We believe the 1Q26 print will be a test of whether management can articulate a credible framework for long-term ROIC that satisfies investors concerned about returns on the massive AI infrastructure build-out,” Erickson further said.

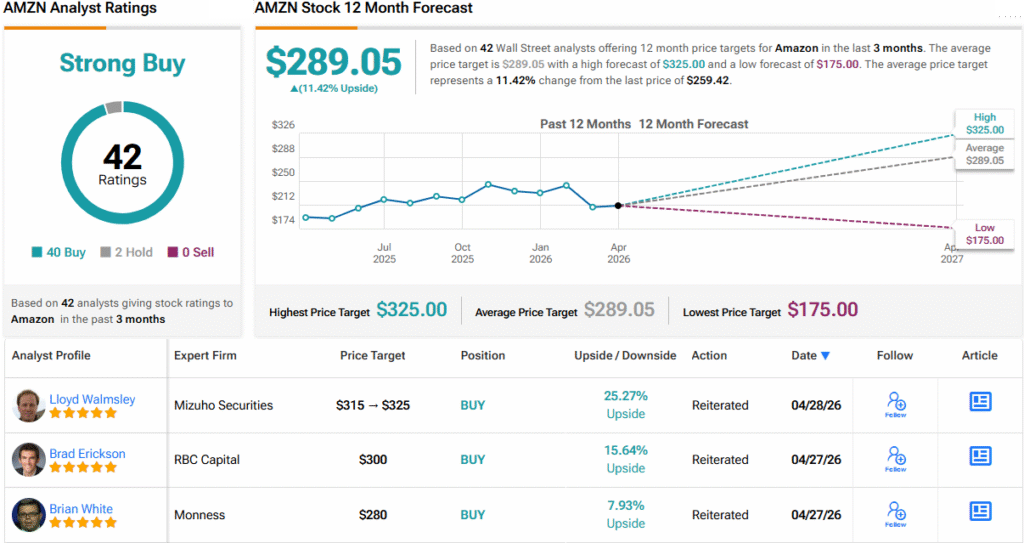

Bottom line, heading into the print, Erickson remains bullish on AMZN, assigning an Outperform (i.e., Buy) rating alongside a $300 price target, implying ~16% upside over the next 12 months. (To watch Erickson’s track record, click here)

The broader Street is slightly more conservative, with an average price target of $287.33 pointing to about 11% upside. Still, sentiment remains overwhelmingly positive, with 40 Buys versus just 3 Holds combining for a Strong Buy consensus. (See AMZN stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.