When it comes to Nvidia (NASDAQ:NVDA) and its quarterly earnings, the question is simple: it’s not whether the company will surpass expectations, but by how much. And all signs are pointing upward as Nvidia gears up to report its fiscal Q1 2027 numbers this Wednesday.

Claim 55% Off TipRanks

Trade NVDA with leverageThat growing confidence is largely tied to what investors have already heard from the companies spending the most on AI infrastructure. The hyperscalers have all weighed in with their earnings reports, and their massive capex numbers have made it crystal clear that the AI spending craze has yet to crest. Moreover, CEO Jensen Huang has given zero indication that Nvidia’s joyride is coming to an end. He recently joined President Donald Trump on his delegation to China, potentially greasing the wheels for the company to resume GPU sales into the world’s second-largest economy.

Against that backdrop, Nvidia has guided for $78 billion ±2% in revenue for the recently concluded quarter, which would represent a sequential jump of roughly $10 billion. Yet, top investor James Foord wouldn’t be surprised if even more is in store for the market leader.

Nvidia has guided for $78 billion ±2% in revenue for the recently concluded quarter, which would represent a sequential jump of $10 billion. Yet, top investor James Foord wouldn’t be surprised if even more is in store for the market leader.

“This earnings report could remind the market why there is only one Nvidia,” states the 5-star investor, who is among the top 3% of stock pros covered by TipRanks.

The investor cites a number of bullish catalysts that could help Nvidia deliver another strong quarter, while simultaneously raising expectations for future growth. He notes that GPU rental pricing is elevated while AI hyperscaler spending is in overdrive, both of which should translate into continued demand for Nvidia’s wares.

Going forward, with the “very real possibility” that sales to China will resume, Foord calculates that this could add another $10 billion to $16 billion in revenue. He points to recent reports that China has approved purchases of more than 400,000 H200 chips by ByteDance, Alibaba, and Tencent.

“Despite all the geopolitical noise, Chinese firms still want Nvidia GPUs because they are arguably the best out there,” states Foord.

When it comes to the earnings, the investor will be keen to understand the outlook on Blackwell, gross margins, and forward guidance. He foresees bullish signals emanating from all three of these elements.

And that makes Foord quite optimistic that another leg up is in the offing for Nvidia.

“I reiterate my Strong Buy on Nvidia and suggest buying ahead of earnings,” concludes the investor. (To watch Foord’s track record, click here)

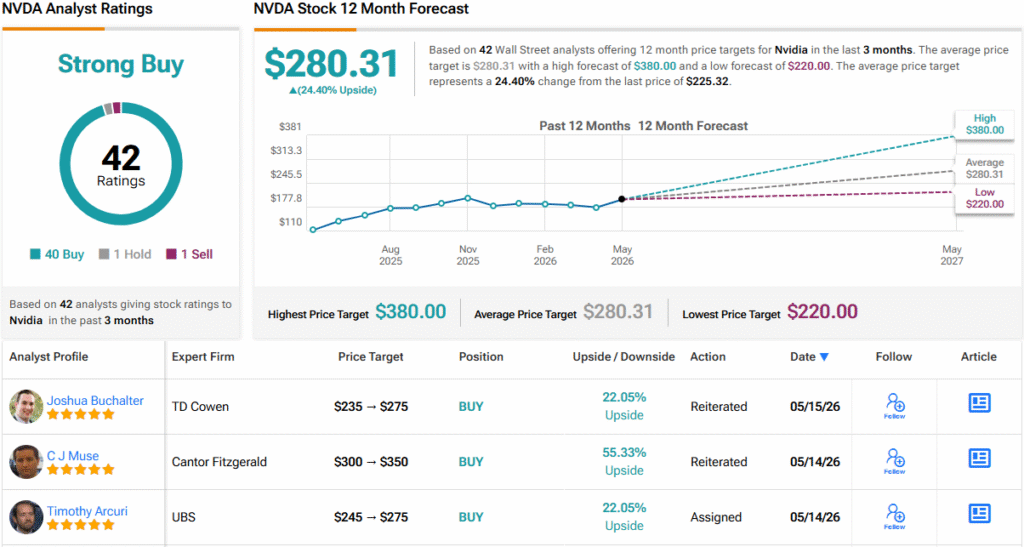

That optimism is echoed across Wall Street. Nvidia carries an overwhelmingly bullish analyst consensus, with 40 Buys, just 1 Hold, and a lone Sell rating, earning NVDA a Strong Buy consensus. Its average 12-month price target of $280.31 implies about 24% upside from current levels. (See NVDA stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.