General Motors (GM) posted strong Q1 results, but the cash story falls short, at least for now. That is why I remain bullish on GM stock, with one important caveat. The Q1 earnings beat looked much cleaner on the income statement than on the cash flow statement. The Detroit-based automaker delivered strong adjusted earnings per share (EPS), solid adjusted EBIT growth, and a modest guidance raise. However, investors still seem unconvinced about how much of that profit will convert into near-term free cash flow.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

In my view, this does not break the bullish thesis. GM still looks deeply undervalued at a very modest FY26 earnings multiple compared to peers. The company also continues to guide for stable adjusted automotive free cash flow this year. However, with electric vehicle (EV) restructuring payments, capex, and commodity costs still weighing on cash conversion, the stock remains cheap for a reason — just, in my view, too cheap.

A Solid Beat, but the Stock Says Otherwise

GM confirmed the bearish post-earnings momentum, with shares falling about 3% even after reporting a solid beat across the board in Q1. This comes despite the stock having already traded in the red for the past six consecutive sessions.

That being said, the reported results were far from bad. Adjusted EPS came in at $3.70, well above the market’s $2.62 expectations, implying 33% year-over-year growth. Revenue reached $43.62 billion, about $50 million above consensus, although still down 0.9% year-over-year.

Looking at adjusted EBIT — arguably the key operational metric for automakers — GM delivered $4.3 billion, up 22% year-over-year. Even though U.S. dealer inventory declined 6% year-over-year and constrained volumes, resilient truck and sport utility vehicle (SUV) demand still helped support profitability, alongside cost efficiencies and a more favorable foreign exchange (FX) backdrop.

As a result, GM raised its FY26 adjusted EBIT guidance by $500 million to a range of $13.5–$15.5 billion, driven primarily by tariff-related adjustments. The consensus for FY26 adjusted EPS now sits around $12.4–$12.8, implying a robust year-over-year growth from roughly $9.2 in FY25. Management’s updated EPS guidance band also reflects a modest increase over its pre‑Q1 midpoint.

A Good Free Cash Flow Story, with a Catch

I believe the market’s muted reaction to General Motors’ earnings can be best explained through the lens of cash conversion quality. To recap, GM reported $10.6 billion in adjusted automotive free cash flow (FCF) for FY25. That’s down from $14 billion in 2024, reflecting the impact of EV‑related charges, regulatory and tariff headwinds, and transformation costs. Still, for the year, it was solid cash generation for an automaker of this size — especially considering the high capex of $9.2 billion, ongoing EV costs, and regulatory pressure.

The most bullish stretch was the second half of 2025, when GM shares rallied over 55% for the full year, with most of that move coming between June and December. Q3 alone delivered $4.2 billion in adjusted auto FCF, followed by $2.8 billion in Q4. This shows that when working capital and timing align, GM can still convert EBIT into cash quite effectively.

However, the caveat shows up in Q1 2026. At first glance, adjusted auto FCF improved to $1.27 billion, up from $811 million in the same quarter last year, which looks like a positive development. The issue lies in the composition. Automotive operating cash flow was just $533 million, while capex totaled $1.5 billion. Adjusted auto FCF only turned positive after a roughly $2.2 billion add-back from “EV strategic realignment.”

In other words, adjusted FCF was positive, but the underlying cash flow before adjustments was actually negative, and that’s the key point. Even on a trailing twelve-month basis, GM’s cash flows still look strong, with more than $11 billion in adjusted FCF generated over the period. However, the most recent quarter shows that part of that generation still depends on adjustments and the normalization of EV-related costs.

Too Cheap to Ignore?

The key takeaway from GM’s earnings call is that the company maintained its adjusted auto FCF guidance of $9–$11 billion, but noted that it will be more heavily weighted toward the second half of 2026 and that it excludes tariff refunds due to uncertainty around timing.

To make matters worse, GM still faces significant EV-related cash charges. Since the second half of 2025, the company has recorded $5.6 billion in cash charges, of which $2.6 billion had already been paid by March and another $600 million in April, with most of the remaining outflows still expected in FY26.

At the same time, even with strong Q1 earnings, there is a natural question about how much of that profit will translate into cash in the near term, and how much will continue to be absorbed by EV restructuring, capex, and commodity costs.

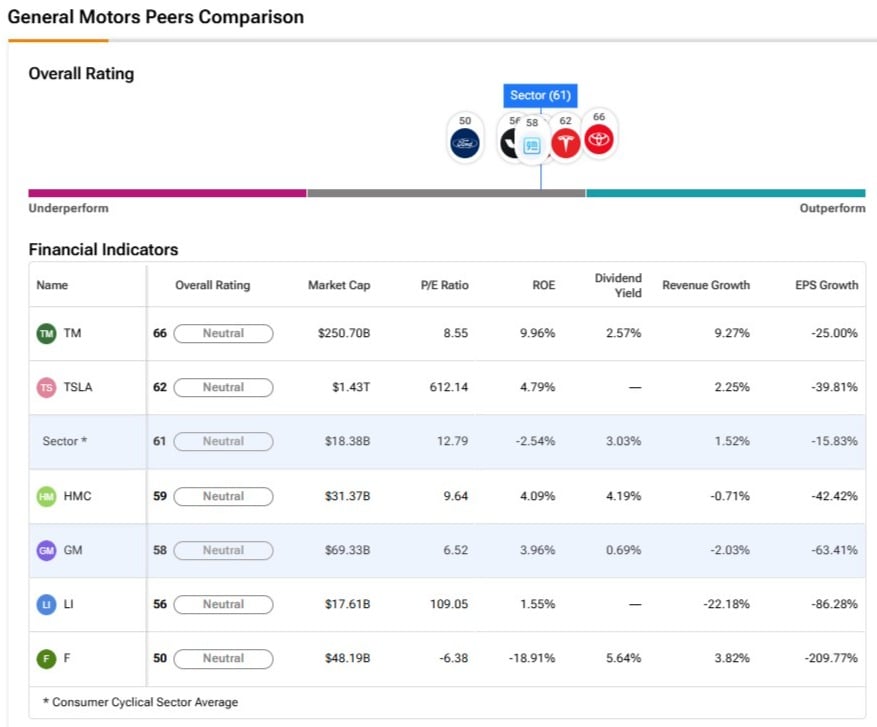

So this helps explain the recent valuation compression. Right now, GM trades at a forward P/E of about 6x FY26 earnings. The market consensus expects GM to grow EPS at about 14.5% per year over the next three to five years, well above the auto sector’s long‑term EPS‑growth rate of around 11%. When you apply that growth to GM’s forward multiple, it implies a forward PEG ratio of roughly 0.40, which screens as deep‑value territory.

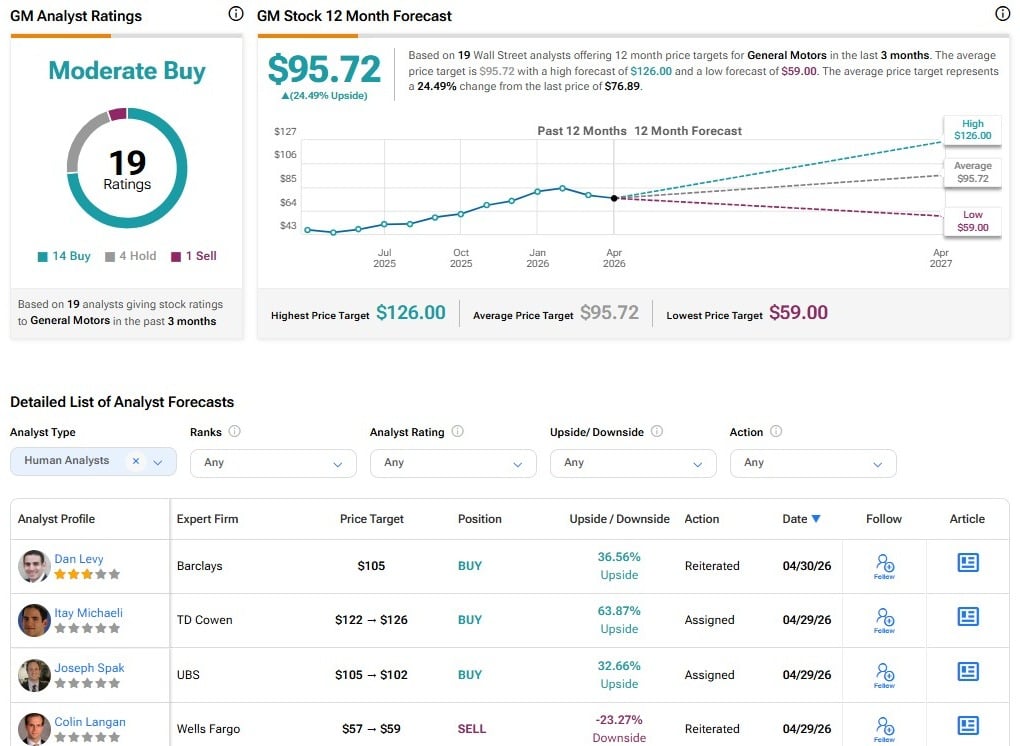

Is GM a Buy, Hold, or Sell, According to Wall Street Analysts?

The consensus view on General Motors is a Moderate Buy. Out of 19 analyst ratings, 14 are Buy, four are Hold, and one is Sell, leading to an average price target of $95.72 — implying about 24.9% upside from current levels.

Cheap for a Reason, but Still Too Cheap

On the surface, General Motors posted solid Q1 numbers and a reassuring upward revision to its guidance, but there are still some flaws — mainly around cash conversion quality — that continue to weigh on the investment thesis.

I think the low valuation multiples are somewhat justified by the cyclical nature of automotive earnings, with EPS growth partly driven by buybacks rather than pure operational expansion, and by the ongoing EV transition, which makes the overall picture less clean.

Still, even with these caveats, the valuation seems to be pricing in a much worse scenario than what GM has actually been delivering. GM doesn’t have perfect cash conversion, but it isn’t burning cash in its core business either. The company still expects to generate $9–$11 billion in adjusted automotive free cash flow this year, which is meaningful for a stock trading at such low multiples.

That’s why I see GM as a great stock to buy on current weakness, with material upside as the market starts to recognize that this level of cash generation is not consistent with a multiple of just 6x earnings.