GameStop’s (GME) proposed $56 billion bid for eBay (EBAY) seems more strategic than realistic, in my view, which is why I rate GME stock as a Hold. While the offer has caught the market’s attention and created some uncertainty around eBay’s outlook, the structure of the deal raises major concerns —especially tied to financing, execution, and dilution risk — for the video game retailer.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The transaction would require a much smaller company to acquire a far larger one using a mix of cash, debt, and significant stock issuance. As the deal currently stands, I believe investors are unlikely to fully embrace the mergers and acquisitions (M&As) narrative at this stage. In my view, GameStop management — particularly Ryan Cohen — may be signaling a broader strategic direction rather than seriously pursuing the acquisition.

At the same time, the setup looks asymmetric on both sides. eBay, the global online marketplace, benefits from a potential valuation floor and the possibility of exploring strategic alternatives. GameStop, meanwhile, would absorb most of the skepticism tied to whether this transaction can actually happen.

A Minnow Trying to Swallow a Whale

After several quarters of market speculation about what Ryan Cohen’s next move would be at the helm of GameStop, we finally have something meaningful. GameStop sent a letter to eBay’s chairman proposing to acquire the company in its entirety for $125 per share. That represents a sizable premium over the approximately $103 level at which eBay traded before the announcement. The total transaction would come in at around $56 billion.

However, that naturally raises the question: how could GameStop, with a market cap of roughly $11 billion and about $9.4 billion in cash on its balance sheet, realistically pull off a deal of this size? According to Cohen, the structure would include $20 billion in financing from TD Securities (TD), which has reportedly indicated a strong willingness to raise the capital. The remainder would be split between cash and stock.

In practical terms, that means $29.4 billion from financing and existing cash, plus another $26.1 billion from issuing GameStop shares as deal currency.

Simply put, raising $26.1 billion in equity would mean issuing more than twice GameStop’s current market cap. That implies massive dilution, which in most cases leads to sustained selling pressure and can push the stock into a classic negative loop. The only way this works is if the market fully buys into the M&A narrative, GME shares rally hard, and effectively become a “strong currency.” To be fair, we’ve seen that dynamic before during the meme rallies over the past five years.

What’s in it for eBay Shareholders?

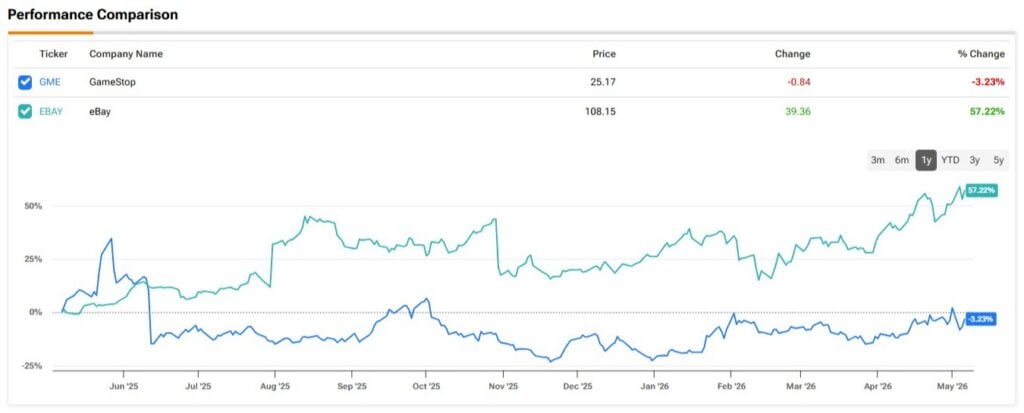

To begin with, eBay has a fiduciary duty to at least review the proposal, especially considering that GameStop has accumulated roughly 5% of the company’s shares since February. That also helps explain why eBay stock has been performing well this year. On top of that, the premium is meaningful. GameStop’s offer sits about 20% above the current share price, while analyst consensus puts the implied value at around $108 per share — effectively offering shareholders a near-term “exit.”

That being said, eBay today is not exactly a growth story. User growth remains modest, and the company continues to spend heavily on marketing just to maintain its base. This is where Ryan Cohen’s pitch comes in. His turnaround narrative is largely based on efficiency, with potential cost savings of around $2 billion. The plan also suggests a significant pro forma operating margin expansion — from 20.5% to roughly 38%–40% as early as year one.

However, the key detail sits in the structure. eBay would receive only $29.6 billion in cash at closing. The remaining $26.1 billion would be paid in GameStop shares, meaning the final value realized by shareholders would depend on GME’s stock price at or near completion. In practice, that introduces a mark-to-market component, as GameStop’s stock could move materially between the announcement and the close.

That’s where the risk increases. If this were a 100% cash deal, eBay shareholders would simply take the $125 per share and move on. With stock in the mix, part of the consideration becomes uncertain. If GME shares fall by about 25% to 30% before closing, that premium could effectively disappear.

Is This Deal Really the Goal?

M&A situations where a smaller company tries to acquire a much larger one are not unprecedented. However, more often than not, they are about strategy or signaling rather than a straightforward acquisition. I believe the GME-eBay situation may fall into that category.

Ryan Cohen, who rarely gives interviews or hosts earnings calls, recently went on CNBC and came across as fairly dismissive, even suggesting that eBay is poorly run. To me, it felt quite clear that the goal was to oversell how “broken” eBay is in order to justify the deal. That aligns with the idea that this situation could be about something else. Maybe it surfaces a reverse scenario, where GameStop ends up being acquired instead, or it simply creates optionality rather than actually following through with the acquisition.

I also think the market may be giving Cohen a bit too much credit at this point. Investors aren’t taking the bid entirely at face value, and the whole situation still feels highly speculative. Even if nothing ultimately happens, the setup looks asymmetric. eBay gets the optionality with relatively limited downside, while GameStop absorbs the skepticism, financing concerns, and execution risk. That helps explain why the stock reaction tends to diverge in the short term.

Are GME and EBAY Buy, Hold, or Sell According to Wall Street Analysts?

At this point, analysts have largely stepped away from covering GameStop, with no ratings issued on the stock over the past three months. On the other hand, eBay is currently rated a Moderate Buy based on 24 ratings in the same period, including 10 Buy and 14 Hold recommendations. The average price target is $108.87, which implies virtually no downside from the current share price.

Where the Risk-Reward Stands Now

I rate GameStop a Hold because, although upside potential remains, the current setup introduces more uncertainty than clarity in the near term. The proposal, as structured, relies heavily on external financing and meaningful stock issuance, which increases dilution risk and raises questions about how feasible this actually is to execute.

Even if the deal doesn’t materialize, the asymmetry looks fairly clear. eBay benefits from increased market attention, a potential valuation floor, and the possibility of alternative strategic paths being explored. GameStop, on the other hand, ends up absorbing the skepticism, financing concerns, and execution risk, which tends to weigh on sentiment in the short term. That said, I wouldn’t underestimate Ryan Cohen or the potential for retail investors to step back in and push the stock into another strong rally.

For that reason, I see GameStop’s risk-reward as more balanced at this point, while eBay appears better supported — though with more limited upside after the recent move.