It was not that long ago that Intel (NASDAQ:INTC) stock was persona non grata, with its inferior products losing share in the CPU market, and the company considered well behind peers in the AI game.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

However, perception about the stock has shifted dramatically. In fact, it is currently one of the market’s hottest names, surging by 86% year-to-date and up by 262% over the past year. Investors are evidently buying into the turnaround story, with the chipmaker recently announcing a series of deals that have encouraged both investors and Wall Street about the outlook for its foundry business.

Meanwhile, demand for server CPUs driven by agentic AI is rising sharply, with ASPs (average selling prices) potentially increasing by 10% to 15% this year. Against this backdrop, analysts have also revised price targets and earnings estimates higher.

With the Q1 earnings season now at play, Rosenblatt analyst Kevin Cassidy expects companies with significant exposure to data centers to report upside to March quarter estimates and to issue June quarter guidance above consensus, too, driven by rising demand for compute capacity.

So that bodes well for Intel, right? Not so, says Cassidy, who ranks among the top 1% of Street stock experts.

“We are most cautious on INTC due to the limited ability to respond to increasing CPU demand,” Cassidy opined.

With Intel slated to report Q1 earnings on Thursday (April 23), Cassidy is “less constructive” on the near-term setup, as healthier server demand is likely to be offset by a Q1 “supply trough” following a better-than-anticipated 4Q25, along with “continued margin pressure” from the 18A ramp. Cassidy’s Q1 revenue and profit estimates of $12.2 billion and roughly breakeven non-GAAP EPS sit slightly below consensus, and his 2QF26 forecast also remains below Street forecasts.

Cassidy thinks investor attention will be on Intel’s 18A node and whether the ramp can proceed without further weighing on gross margins. Eyes will also be on potential foundry customer wins following recent announcements involving Google and Terafab. With management talking of possible foundry customer disclosures in the second half of the year and production targeted for 2028, any “incrementally positive commentary on external customer traction should be supportive to the stock.”

Longer term, Cassidy sees Intel benefiting from strengthening data center demand and broader growth in compute. However, the analyst continues to see the turnaround as a multi-year process that remains heavily dependent on execution.

“While Intel is making progress in process technology and products, we still need to see better yields, stronger gross margin, and clearer evidence the company can translate product/process improvements into durable earnings power,” the analyst summed up.

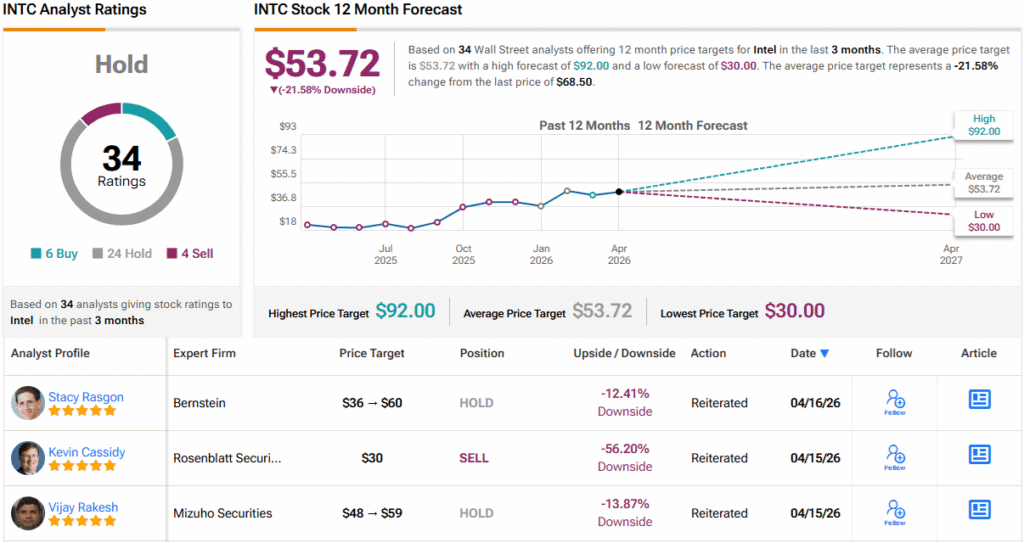

Accordingly, Cassidy assigns INTC shares a Sell rating, while his Street-low $30 price target suggests the stock is overvalued by 56%. (To watch Cassidy’s track record, click here)

3 other analysts are also INTC bears, yet with an additional 24 Holds and 6 Buys, the Street rates the stock a Hold (i.e., Neutral). The $53.72 average price target is not as bad as Cassidy’s objective, but still points to a 12-month decline of ~22%. (See Intel stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.