Advanced Micro Devices (NASDAQ:AMD) stock is surging 18% on Wednesday after the chipmaker delivered exactly the kind of report investors were hoping for – another quarter of accelerating AI-driven growth, a clean double beat, and guidance that pointed to demand remaining very much intact. While Wall Street had already entered the print with elevated expectations following AMD’s massive rally over the past month, the company still managed to clear the bar with room to spare.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Revenue climbed 38% year over year to $10.25 billion, topping consensus estimates by roughly $330 million, while non-GAAP earnings per share reached $1.37, beating expectations by $0.08. The main engine remained the data center business, where revenue jumped 57% to $5.8 billion as demand tied to AI inference workloads and agentic AI deployments continued to ramp. Looking ahead, AMD guided for second-quarter revenue of roughly $11.2 billion, implying another quarter of growth approaching 50%.

At first glance, the story appears straightforward – AI demand remains strong, AMD continues gaining traction, and the growth outlook still points higher. Yet, top investor Jonathan Weber argues investors should be careful about assuming the rally can continue indefinitely.

“AMD stock isn’t a buy at current prices, despite a good Q1 report and positive Q2 outlook,” says Weber, who is among the top 2% of stock pros covered by TipRanks.

Weber is stuck on the company’s valuation, which has soared upward by more than 200% over the past twelve months. That’s left AMD trading at a hefty price-to-earnings multiple in the high-50s.

Another issue for the investor is AMD’s bottom line. Though non-GAAP gross margin grew by 1% in Q1, non-GAAP operating expenses surged by more than 40%, and that’s not a great sign.

“AMD’s operating expenses actually grew a little faster than its revenues, which suggests that its cost controls aren’t very tight for now,” adds Weber. “I think that’s unfortunate.”

And while the company is “smashing” its all-time highs, almost any discussion of AMD will also reference the much bigger Nvidia. It’s not such a favorable comparison, asserts Weber, who notes that Nvidia is growing at a faster rate (a 73% year-over-year increase in revenues last quarter) and trades at a lower multiple (a price-to-earnings ratio in the mid-20s).

“One can argue that AMD’s smaller size gives it more room to grow in the coming years, but it is not guaranteed that this will play out,” concludes the investor, who gives AMD a Hold (i.e., Neutral) rating. (To watch Weber’s track record, click here)

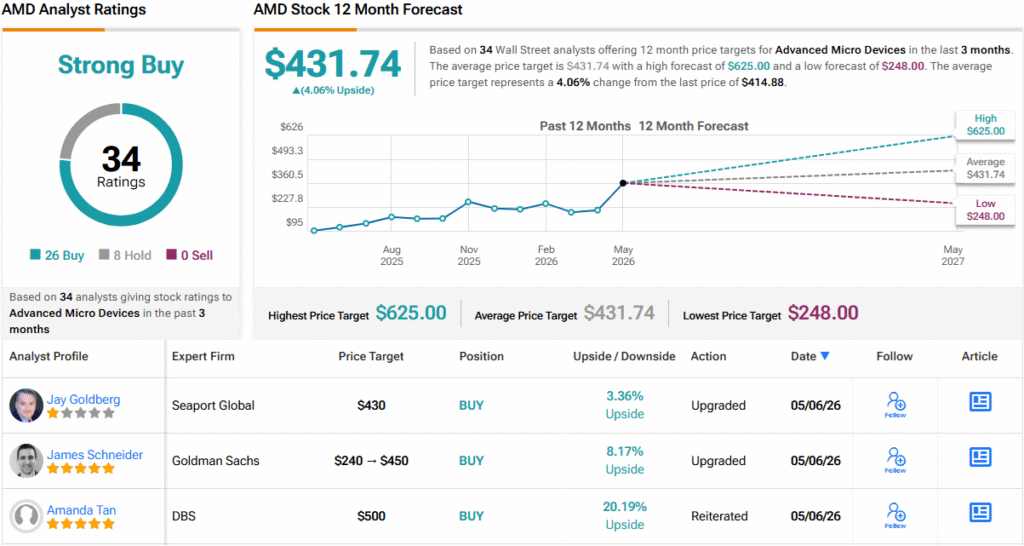

Wall Street, however, continues to lean bullish. AMD currently carries a Strong Buy consensus rating based on 26 Buys and 8 Holds. Yet, after the stock’s enormous run, the average 12-month price target of $431.74 implies upside of only about 4%, suggesting expectations may already be running close to full speed. (See AMD stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.