Advanced Micro Devices (NASDAQ:AMD) shares are surging 15% in after-hours trading Tuesday after the AI chip giant delivered a quarterly report that gave investors exactly what they wanted to see – strong AI demand, accelerating data center growth, and guidance that moved past Wall Street expectations.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The print arrives after weeks of debate over whether enthusiasm surrounding AI infrastructure spending had run too far ahead of reality, particularly following recent updates from hyperscalers discussing their own custom silicon ambitions. Instead, AMD’s results suggested the spending wave remains very much intact. Data center revenue climbed 57% year-over-year to $5.78 billion, above Street expectations of $5.61 billion.

More broadly, AMD reported non-GAAP earnings per share of $1.37, beating consensus estimates by $0.08, while revenue climbed 37.8% year over year to $10.25 billion, topping expectations by $330 million. Looking ahead, the company expects second-quarter revenue of approximately $11.2 billion, plus or minus $300 million, well ahead of the Street’s $10.52 billion forecast. Management also projected non-GAAP gross margin of approximately 56% for the quarter.

Still, not everyone is convinced the rally can continue unchecked. Top investor Oliver Rodzianko, who ranks among the top 1% of stock pros tracked by TipRanks, believes the market’s “AI fervor” has already gone too far.

While Rodzianko still views AMD as a “high-quality long-term compounder” led by an “elite” management team, he argues that the stock has entered momentum territory where exceptional results are needed to justify additional upside. The investor also pointed to potential dilution tied to performance-based warrants connected to OpenAI and Meta, warning that while the impact would unfold gradually, it could still act as a background drag over time.

“The greatest investors and traders know when to let the suckers play, and the pro goes home,” Rodzianko said.

Even so, Rodzianko is not turning bearish on AMD’s broader story. The investor still sees room for gains over the next 12 months, though he believes the period of easy gains has likely passed and that future returns may become harder to achieve as valuation pressures build. In his view, risks tied to hyperscaler digestion, energy bottlenecks, or slowing AI GPU momentum could eventually trigger a sharper pullback toward fair value.

“Long-term growth targets are compelling, but rational allocators ought to be trimming into strength here,” adds Rodzianko. “Better entry points probably lie ahead.”

Rodzianko is therefore assigning a Hold (i.e., Neutral) rating for AMD. (To watch Rodzianko’s track record, click here)

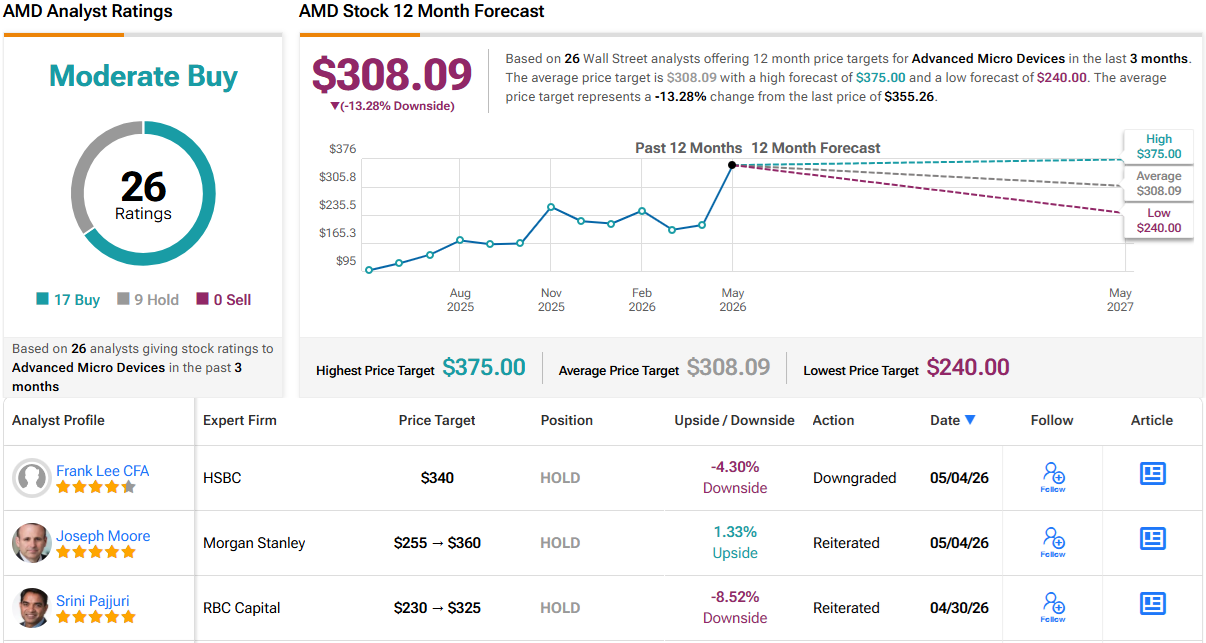

Wall Street offers a mixed picture. With 17 Buys and 9 Holds, AMD enjoys a Moderate Buy consensus rating. However, based on Tuesday’s closing price, the stock’s 12-month average price target of $308.09 points to downside of nearly 13%, suggesting the “AI fervor” Rodzianko cited may have gone further than even some bulls anticipated. (See AMD stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.