Last week, EV maker Tesla (TSLA) stock experienced its biggest single-day dip (12.3%) in over four years following its disappointing earnings print. Not only did Tesla miss earnings expectations, but it also failed to provide details on the much-awaited Robotaxi. Further, EV price wars are intensifying, putting pressure on margins and profitability. Therefore, I am neutral on the stock and will wait on the sidelines to buy TSLA until I see more clarity on its sales growth and future roadmap. Overall, it may not deserve its spot in the Magnificent Seven.

Claim 55% Off TipRanks

Looking for exposure to SpaceX & Anthropic? Check out AGIX ETF

Q2 Earnings Miss and Continued Margin Compression at Tesla

On July 23, Tesla’s adjusted earnings of $0.52 per share missed the consensus estimate of $0.61 per share. Growing competition in the EV space led to a slowdown in the EV sales growth at Tesla. Also, Q2 EPS came in much lower (-43%) than the Q2FY23 figure of $0.91 per share, negatively impacted by price cuts. This marks the fourth consecutive quarter of negative earnings growth at Tesla.

Meanwhile, total revenues grew 2% to $25.5 billion, beating expectations. However, the main concern during the quarter was Auto revenues, which fell 7% year-over-year to $19.9 billion. Auto sales declined year-over-year for two quarters in a row. It’s important to note that the price cuts exercised by the company failed to notably boost sales during the quarter.

Moreover, margins suffered as competition in the EV space intensified. To combat the rising competition, Tesla cut prices globally and offered incentives and discounts to boost sales. As a result, adjusted operating margins (EBITDA margin) declined to three-year lows of 14.4% compared to 18.7% reported a year ago. This marks the fourth consecutive quarter of margin compression witnessed at Tesla.

During the quarter, Tesla delivered 443,956 vehicles, registering a decline of 5% year-over-year compared to 466,140 vehicles sold a year ago. Sequentially, though, deliveries improved from the 386,810 reported in Q1. For the first half of the year, Tesla delivered 831,000 vehicles globally. Given the run rate, it may be difficult for Tesla to meet its prior full-year target of selling 1.8 million vehicles globally.

No wonder the company didn’t update its sales outlook for the full year. Further, adding to investors’ disappointment, management stated that the vehicle volume growth rate may be “notably lower than the growth rate achieved in 2023.”

Old Product Lineup and Lack of Clarity on the Future Roadmap

What is the possible reason the Tesla stock is hugely underperforming the benchmark index? Tesla stock is down 16% year-over-year versus gains of 19% posted by the S&P 500 over the same period. Further, it is the only stock among the Magnificent Seven that has yielded negative returns in the past year.

Despite rising competition, Tesla continues to remain the number one seller of EVs in the U.S. However, its line-up of cars, including sedans and SUVs, has become old, highlighting the need for new models. In that context, CEO Elon Musk stated during the earnings call that the company is expected to launch a new “more affordable” vehicle during the first half of 2025.

Contrary to investors’ expectations, Musk did not give any clear details on the full self-driving system roadmap. While he stated that the system should be able to function without human supervision by year-end, he also left investors confused, stating that his prediction has a history of being “overly optimistic.”

On top of that, the company postponed the Robotaxi unveiling event to October 10 versus August 8, as expected earlier, citing design changes sought by the CEO. The company has yet to clear regulatory and technical challenges before its expected launch.

Aiming to fill investors with optimism on other revenue probabilities, Musk spoke about the scope of artificial intelligence and humanoid robots. Production of the humanoid robot Optimus is expected to begin early next year for internal use at Tesla, with ramped-up production expected in 2026.

Last week, Musk said that Tesla is contemplating investing $5 billion in Elon Musk’s AI startup xAI. The news sparked concerns about conflict of interests. Further, it may not add value for Tesla investors, given that the AI business needs gigantic investments with an uncertain generation of profits in the near term.

While the diversified revenue stream is welcome, investors particularly yearn to learn more about the future of its core revenue generator: EVs. However, investors were left more clueless than before on that front after the call. Markedly, Telsa has a history of not meeting its scheduled targets. Therefore, it’s best to wait and watch until the new lineup has greater visibility.

Tesla’s Valuation Is High at Current Levels

Tesla stock has mostly traded at a high premium to its peers in terms of its valuation. TSLA is currently trading at a forward P/E ratio of 93x, at a significant premium to the peer group median (16x).

Still, the current multiple is still low compared to its own five-year average of 115x. Crucially, hedge funds have a “very negative” confidence signal and have sold 677,500 shares of TSLA stock during the last quarter.

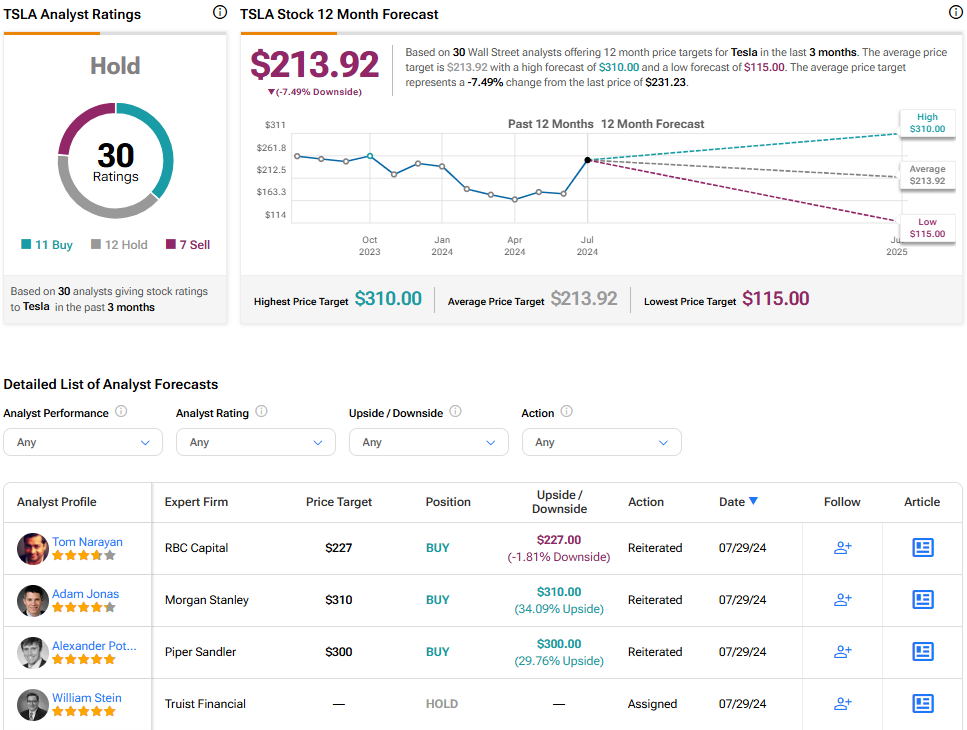

Is Tesla Stock a Buy, According to Analysts?

As per TipRanks, analysts are cautiously optimistic about TSLA stock and have a Hold consensus rating based on 11 Buys, 12 Holds, and seven Sells. The average TSLA stock price forecast of $213.92 implies 8.2% downside potential.

Conclusion: Remain on the Sidelines

Tesla is no longer among the 10 largest stocks in the world, having been overtaken by other tech stocks. Competition has certainly intensified in the EV industry, as seen with the ongoing price wars. Lower prices and decelerating sales growth will likely continue to weigh on the margins and share price performance in the near term.

While the current share price weakness may look like an attractive entry point to buy the shares, I would rather wait and watch before obtaining more clarity on the future of this EV giant.