Shares of Cummins (CMI) are crushing the broader market this year, gaining 29.1% compared to the S&P 500’s (SPX) 18.1% gain. Despite this outperformance, it’s still not too late to invest in this company, as shares are still remarkably cheap.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

I’m bullish on Cummins based on its recent strong performance, undemanding valuation, and solid and growing dividends.

A Powerhouse Innovating for the Future

Founded in 1919 and based in Columbus, Indiana, Cummins is a preeminent manufacturer and seller of diesel engines for commercial trucks, off-highway machinery, railroad locomotives, natural gas engines, and other parts and components. It also makes generators.

However, just because this is a 105-year-old company doesn’t mean it isn’t positioning itself for the future.

The company’s small but growing zero-emission business segment, called Accelera, is developing fuel cell electric vehicles (FCEVs) and battery electric vehicles (BEVs). Although Accelera is currently a small segment of CMI’s business, generating just $111 million in sales during the second quarter, it is growing rapidly, with a 31% increase compared to 2023.

Accelera was also recently awarded a $75 million grant from the Department of Energy to convert part of its Columbus, Indiana, engine plant to facilitate the manufacture of battery packs and electric powertrains.

Cummins Expands with Battery Plant and Power Systems

Cummins has also formed a joint venture with leading truck manufacturers PACCAR (PCAR) and Daimler (DTRUY) called Amplify Cell Technologies, aimed at localizing battery cell production in the United States. The joint venture recently began construction on a new battery manufacturing plant in Mississippi.

Meanwhile, the company’s power systems business serves the red-hot data center market, and this business is booming. During the most recent quarter, revenues for the company’s North American power generation business segment grew by 23%, driven in large part by continued strong data center and mission-critical power demand.

Inexpensive Valuation

Despite CMI’s strong performance, which has seen it significantly outperform the S&P 500 in 2024, the stock is still very cheap, so it’s certainly not too late to invest in the company.

Trading at 15.7 times consensus 2024 earnings estimates, it is notably cheaper than the broader market, which trades at 24.5 times earnings. Looking ahead to 2025, the stock looks even cheaper, trading at just 14.11 times consensus forward earnings estimates.

And while some stocks trading at discounted valuations are value traps with declining businesses, Cummins is not one of them. The company just posted record second-quarter revenue of $8.8 billion.

A Dividend Growth Stock with its Foot on the Gas Pedal

Right now, Cummins yields 2.17%. This is far better than the broader market (the S&P 500 currently yields 1.3%), but understandably, may not be enough to draw the attention of income-focused investors.

However, Cummins is a great dividend stock with a long track record of dividend growth. The Indiana-based company has been around for over a century, and it has been paying a dividend for the last 34 years. Not only that, but it has also increased the level of its payout for the last 18 years in a row.

The stock also has a low dividend payout ratio of just 35.0%, meaning that the dividend looks quite safe and that the company has plenty of room to continue increasing its dividend payment going forward.

Further, Cummins is committed to its long-term goal of returning 50% of operating cash flow back to its shareholders.

With the company likely to continue to grow its dividend payment over the long term, investors buying the stock today are likely to enjoy a better yield on cost than the stock’s current yield of 2.4%.

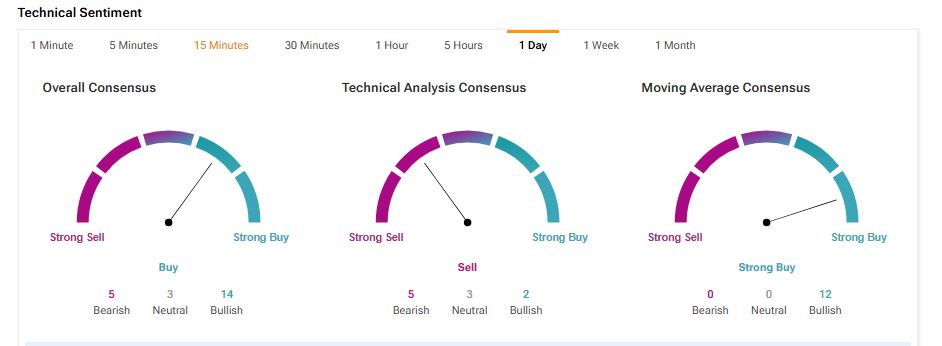

Technical Perspective

Cummins stock also looks strong from a technical perspective. According to TipRanks’ data, CMI’s technical indicators suggest a Buy, implying further upside from current levels.

Is CMI Stock a Buy?

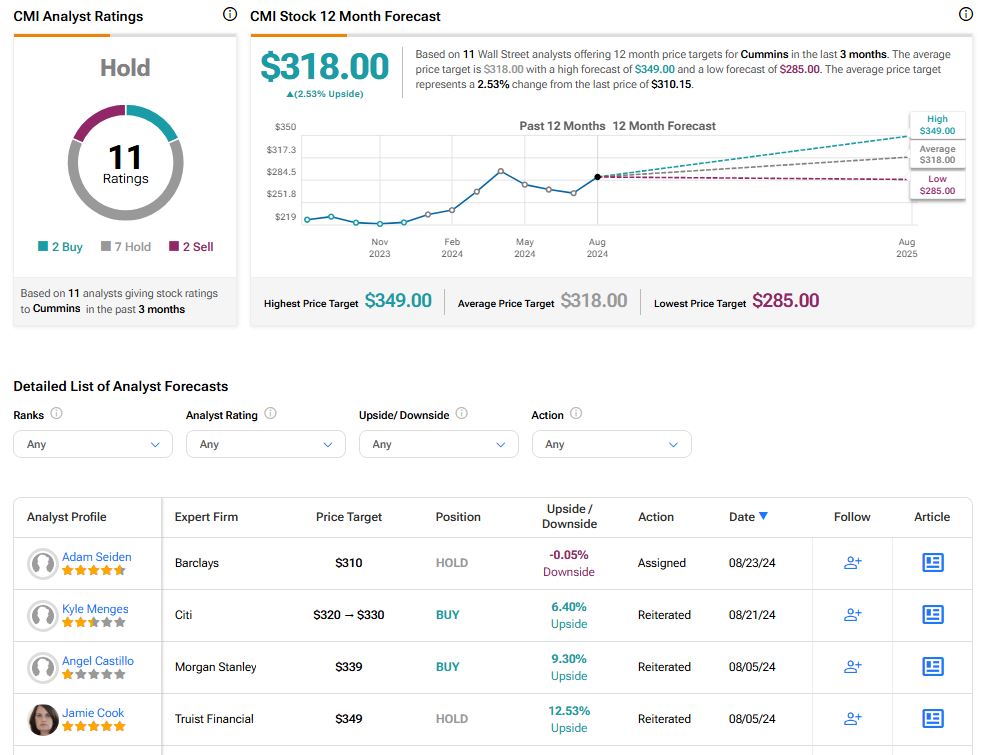

Turning to Wall Street, CMI earns a Moderate Buy consensus rating based on 22 Buys, five Holds, and zero Sell ratings assigned in the past three months. The average CMI stock price target of $318.00 implies 2.53% upside potential from current levels.

Full Steam Ahead

I’m bullish on Cummins based on its recent momentum and strong performance, coupled with an appealing valuation even after this strong 2024 run. Plus, the stock’s forays into fuel cell and battery electric vehicles present intriguing long-term growth potential.

Furthermore, with an above-average yield and 18 years of consecutive dividend increases, Cummins stands out as an attractive choice for dividend growth investors.