Costco (COST) is hard not to like, but the stock already reflects that quality, which keeps me on the sidelines for now. The warehouse-club retailer continues to execute at an impressive level, helped by its powerful value proposition, loyal member base, and consistent traffic growth. However, with the stock up over 17% year-to-date versus roughly 5% for the S&P 500 (SPX), much of that quality already appears reflected in the share price. I remain neutral on COST.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

March Sales Show the Business Is Still Robust

Costco’s March sales report showed another solid month. Net sales rose 11.3% year-over-year to $28.41 billion, while U.S. comparable sales increased 8.7%. Excluding fuel and foreign exchange, U.S. comps rose 6.2%, slightly ahead of February’s 6.0% increase. The numbers were even stronger after adjusting for the Easter calendar shift, which created one fewer shopping day and reduced total ex-fuel or foreign exchange (FX) comps by about 160 basis points. Excluding that impact, total comps were closer to 7.8%.

Traffic rose 1.5%, while the average ticket increased 7.8%. Gasoline played a big role, with higher gas prices and stronger volume pushing the ancillary business up to the mid-20% range. Gas prices were up 17.8%, adding a meaningful boost to reported sales.

Still, the core business was healthy too. Food and sundries were up low-to-mid single digits, while fresh foods and non-foods were up mid-to-high single digits. That mix suggests Costco is still winning across both everyday needs and discretionary categories.

Costco’s Value Proposition Fits the Current Consumer

One reason Costco continues to perform well is that its model is built for a value-seeking consumer. In an environment where shoppers remain careful with spending, Costco’s combination of bulk savings, limited stock-keeping units (SKUs), strong private-label offerings, and treasure-hunt merchandising remains highly attractive.

The company’s traffic trends support this. In Q2, worldwide traffic rose 3.1%, and management continues to deliver mid-single-digit-plus comp growth despite Costco already operating at a nearly $300 billion sales run rate.

Costco also benefits from very low inflation across much of its system, with outright deflation in some categories. That helps reinforce its price-gap advantage versus traditional retailers. In other words, Costco is not just benefiting from inflation-driven ticket growth; it is gaining share because consumers trust its value.

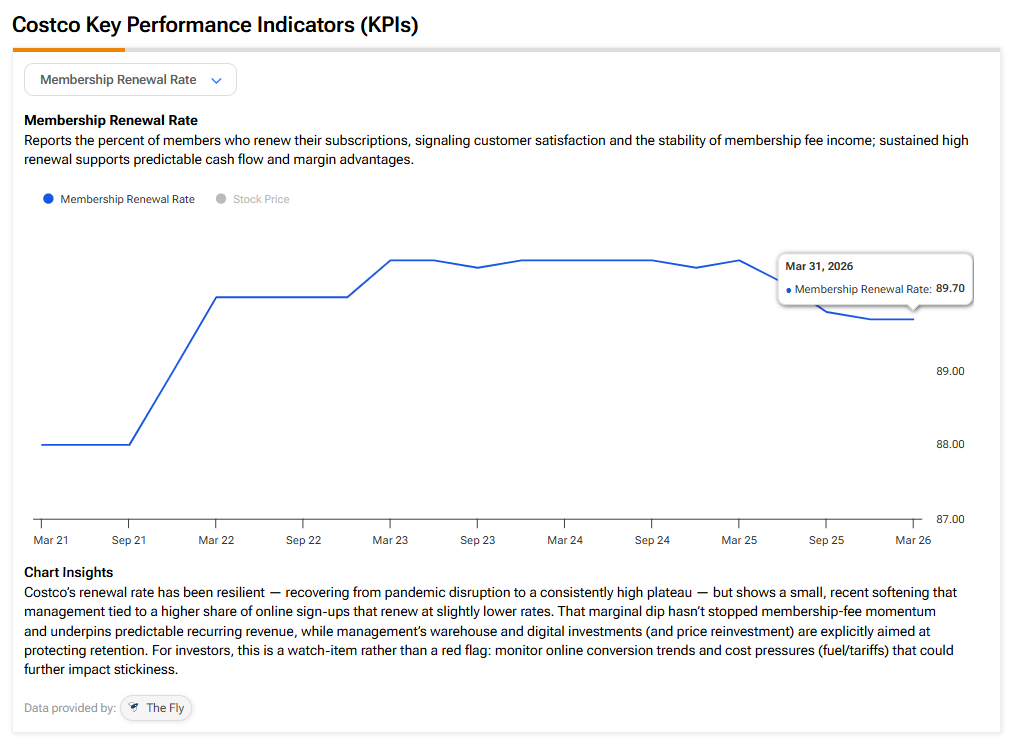

Membership Trends Are Solid, but Worth Watching

Costco’s membership model remains one of the strongest in retail. Membership fee income is a high-margin revenue stream, and the company continues to benefit from fee increases and member upgrades. In Q2, membership fee income rose about 13.6%, or 7.5% excluding fee increases and FX. A key driver is the company’s effort to increase the mix of Executive members, who pay roughly double the standard Gold Star membership fee.

However, paid membership growth has slowed. It rose 4.8% year-over-year in Q2, down from 5.2% in Q1, 6.3% in Q4, and 6.8% in Q3. Renewal rates also remain slightly below recent history, with worldwide membership renewal at 89.7%.

This is not a major red flag, but it matters because Costco’s valuation leaves little room for small disappointments. Investors likely want to see membership growth and renewal rates stabilize before assigning an even higher multiple to the stock.

Valuation Is the Main Problem

Costco has a rare combination of recurring membership income, consistently high traffic, international growth potential, strong management, and a long track record of returning value to shareholders. Yet, the issue is not the business. The issue is the price. Costco currently trades at a P/E ratio of about 55.5x, far above the sector median of roughly 16. Its price-to-operating-cash-flow ratio is about 30.0, versus the sector median of around 10. That is a significant premium, even for a best-in-class retailer.

I also calculated Costco’s fair value using 13 valuation models, including P/E multiples, a multi-stage dividend discount model, and a five-year discounted cash flow (DCF) growth exit model. My fair value estimate is around $840 per share, implying roughly 17% downside from the current stock price.

That does not mean Costco is a bad stock. It means the market is already paying heavily for future consistency. At about 55x earnings, the risk/reward looks balanced rather than compelling.

Wall Street’s View

According to TipRanks, Costco has a Moderate Buy consensus rating, with 16 Buy, six Hold, and one Sell rating. Based on 23 Wall Street analysts, the average 12-month price target is $1,102, implying 8.81% upside from the last price of $1,012.79.

Conclusion

Costco remains one of the highest-quality retailers in the market. Its March sales were strong, Q2 execution was steady, membership fee income continues to grow, and the company’s value proposition is highly relevant in today’s environment.

However, quality is not the same as upside. With COST stock already up strongly this year and valuation sitting at a steep premium to the sector, I do not see enough margin of safety at current levels. For now, I am neutral on COST and would wait for a better entry point.