Shares of CoStar Group, Inc. (CSGP) tanked 21.5% in Tuesday’s extended trading session after the company provided a disappointing outlook for full-year 2022. Nevertheless, the commercial real estate information and online marketplaces provider was able to surpass revenue and earnings estimates.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

During the quarter, adjusted earnings jumped 20.7% year-over-year to $0.35 per share and surpassed analysts’ expectations of $0.29 per share. Similarly, revenues increased 14.2% year-on-year to $507 million, topping the Street’s estimate of $503.1 million.

The company said that net sales bookings in the fourth quarter of 2021 reached an all-time high of $67 million.

Adjusted EBITDA came in at $193.4 million, compared to $166.8 million in the year-ago quarter. As of December 31, 2021, CoStar had about $3.8 billion in cash, cash equivalents, and restricted cash.

For 2021, the company reported adjusted earnings of $1.14 per share, up 15.2% from the previous year. Also, sales rose 17.2% year-over-year to $1.9 billion.

The Founder and CEO of CoStar, Andrew C. Florance, said, “With an addressable market almost three times the size of our existing business, we believe that the residential property opportunity has the potential to add billions in revenue to CoStar Group over the medium to long term. In order to take advantage of this significant growth opportunity, we plan to increase the level of investment in residential products, content, sales and marketing in 2022.”

Outlook

For 2022, the company projects revenue in the range of $2.15 billion to $2.17 billion versus the consensus estimate of $2.2 billion. Also, CoStar is planning to increase the level of investment in Residential to a range of about $300 to $320 million.

Adjusted EBITDA is expected to be between $565 million and $605 million. Adjusted earnings per share (EPS) are anticipated to be in the range of $0.95 to $1.02 versus analysts’ expectations of $1.35 per share.

In the first quarter of 2021, CoStar expects revenue in the range of $510 million to $515 million against the consensus estimate of $516.5 million. Also, adjusted EPS is projected to be between $0.27 to $0.28, compared to the Street’s estimate of $0.32 per share.

Price Target

On February 23, JMP Securities analyst Joe Goodwin maintained a Buy rating on CoStar and lowered the price target to $85 from $105. The new price target implies 35.1% upside potential from current levels.

Goodwin said, “We view the stock’s after-market reaction as a buying opportunity, and continue to like CoStar for several reasons, which include: 1) the company’s dominant market position; 2) it is well led, in our opinion, by Founder and CEO Andrew Florance, who has a track record of success in entering and capturing share in new markets; 3) the CoStar Suite has rebounded nicely and is expected to continue to accelerate growth into 2022; and 4) we like the company’s decision to increase its investment in the large residential opportunity that is estimated to be $72B in the U.S. and $210B globally.”

Overall, the Street has a bullish outlook on the stock with a Strong Buy consensus rating based on 3 unanimous Buys. The CoStar stock price prediction of $90 implies upside potential of about 43% from current levels.

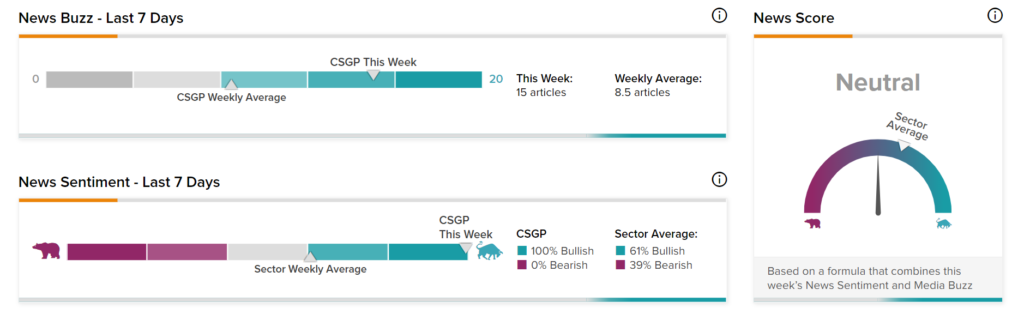

News Sentiment

News Sentiment for CoStar is Neutral based on 15 articles over the past seven days. All the articles have Bullish sentiment, compared to a sector average of 61%, and none have Bearish Sentiment, compared to a sector average of 39%.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure

Related News:

FDA Lifts Clinical Hold on Ocugen’s New Drug Application for COVAXIN; Shares Gain 15.6%

APA Reports Record Revenue in Q4; Shares Pop

Home Depot Posts Strong Q4 Results; Shares Gain Pre-Market