Intel (NASDAQ:INTC) just continues to climb upward, posting a whirlwind surge over the past few weeks. Indeed, its share price has more than doubled in value since the end of March.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

While the AI craze has lifted many a boat, that’s a particularly steep rise. More gains came today, as news surfaced that Apple was considering a partnership with Intel. According to a Bloomberg report, Apple is in discussions with Intel about the possibility of using its chipmaking services.

That follows a number of positive developments that have been adding wind to Intel’s sails. The company’s Q1 2026 earnings report was well-received, especially since its AI and Data Center revenues grew by 22% to hit $5.1 billion.

That’s certainly one of the reasons that INTC has been gaining, notes top investor Anders Bylund. But there’s more going on here.

“It takes a village to raise a child, and it takes several catalysts to double a classic semiconductor stock in 30 days or less,” says the 5-star investor, who is among the top 1% of stock pros covered by TipRanks.

Bylund cites a number of important events that have primed the run over the past few weeks.

First off, he points to the news from early April regarding Intel Foundry’s long-term partnerships with Google Cloud and the Elon Musk-driven Terafab. He posits that this helped to establish Intel as a strategic manufacturing partner.

And then, the earnings numbers later in the month added more fuel for the rally. It wasn’t just the strong revenues – especially in the AI and Data Center segment – as the adjusted earnings per share of $0.29 easily surpassed the expectations of $0.02.

Moreover, the intense demand has pushed up Intel’s yield salvage rate, further boosting revenue. “Intel is making money from imperfect wafers formerly destined for the scrap heap,” states Bylund, underscoring the extraordinary market conditions.

And Bylund sees more gains on the horizon.

“I’m a happy shareholder as Intel’s changing business plan helps it capitalize on unprecedented chip demand from AI customers,” concludes Bylund. “I expect the success story to continue from here.” (To watch Bylund’s track record, click here)

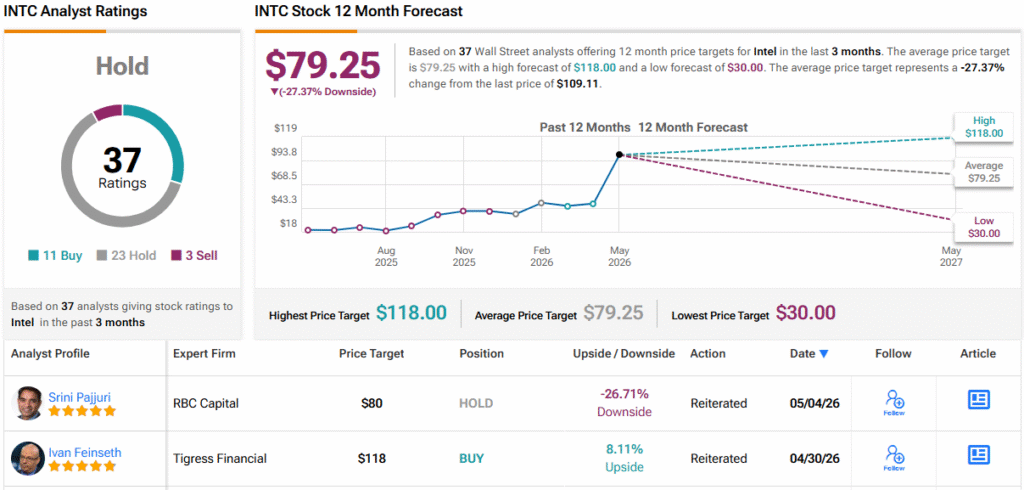

Wall Street isn’t quite as gung-ho. With 11 Buys, 23 Holds, and 3 Sells, INTC carries a consensus Hold (i.e., Neutral) rating. Its 12-month average price target of $79.25 points to losses of ~27%. (See INTC stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.