Coinbase (COIN) continues to build an increasingly ambitious crypto ecosystem, but I’m bearish after its Q1 miss. The May 7 report offered plenty of strategic talking points, from Base to derivatives to prediction markets, but the actual numbers made the story much harder to defend. That disconnect is critical because the cryptocurrency exchange company is still being valued as if its ecosystem progress can easily outweigh weaker trading activity, shrinking transaction revenue, and a much uglier bottom line.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

For me, the quarter reinforced the growing concern of a narrative that keeps improving faster than the actual financial results. That is why I am bearish on Coinbase stock.

The Shiny Bits: Market Share and the Base Renaissance

To give credit where it’s due, Brian Armstrong and company have built a formidable ecosystem that has gone far beyond just buying and selling tokens. In the Q1 results reported yesterday, Coinbase hit a new all-time high in crypto trading volume market share, now at 8.6%. Investors were clearly enamored with the “Everything Exchange” pivot. The derivatives business is finally doing well, too, with retail derivatives revenue alone surpassing $200 million annually.

Even more impressive is the Prediction Markets vertical, which reached $100 million in annualized revenue in its first two full months, making it one of the fastest-scaling products in the company’s history.

The real star of the show, though, remains Base. Coinbase’s Layer-2 has become a behemoth, processing a staggering 62% of global on-chain stablecoin transaction volume. So to back the bull case, Coinbase is really becoming the primary rail for the “agentic economy,” where artificial intelligence (AI) agents settle transactions in USDC. With subscription and services revenue projected between $565 million and $645 million for Q2, I get why the growth-hungry crowd is still sticking around. They see a company that has delivered 13 consecutive quarters of positive adjusted EBITDA, a feat that theoretically proves Coinbase can survive any weather.

The Grim Reality: Layoffs and the Proxy Trap

Despite a couple of positive angles on Coinbase, the company missed Wall Street expectations on both the top and bottom lines. Revenue came in at $1.43 billion, a notable 10% miss, while the bottom line was a bloodbath. We’re looking at a net loss of $394.1 million, resulting in earnings per share (EPS) of -$1.49, while analysts were expecting a profit of $0.29. That is a huge miss that cannot be brushed off as “market volatility.”

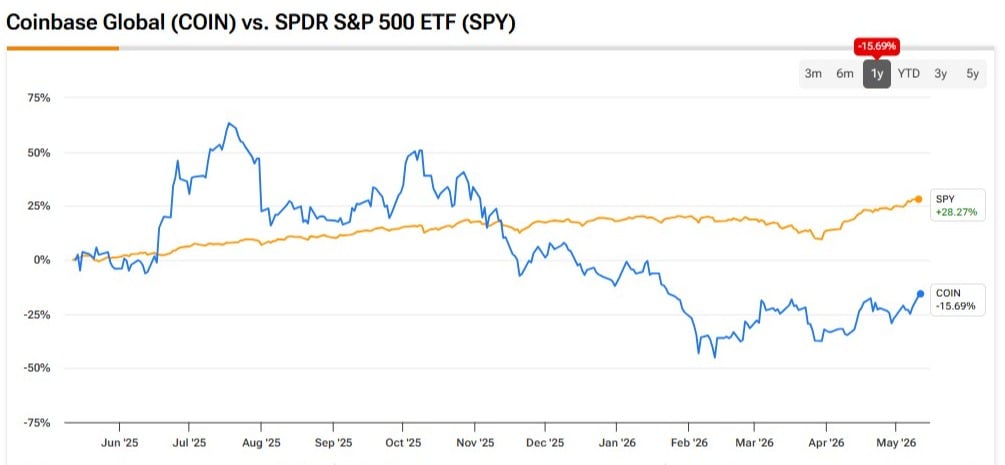

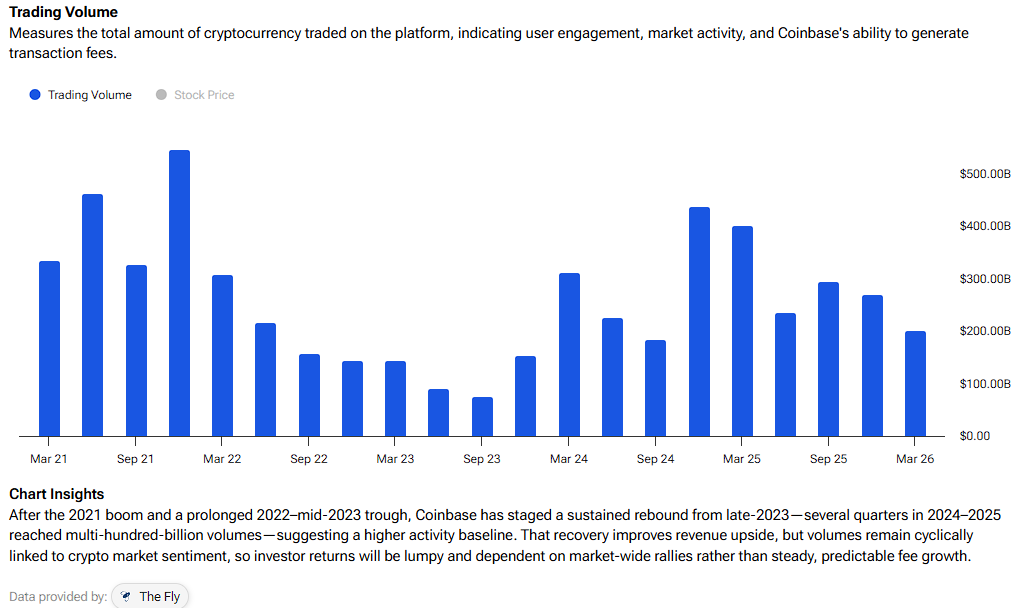

Total revenue fell 21% quarter-over-quarter, with trading volumes plunging 23%. It turns out that even with the best tech in the world, if people aren’t trading, Coinbase isn’t making money.

To add to this, we got the layoff news recently. Coinbase said it’s cutting 700 workers, which is about 14% of the company. Management is trying to frame it as part of this move toward an “AI-native” operating model, but I’m not totally buying that as the full story. To me, this looks much more like a cost-cutting move because they had to do it. Sure, getting leaner can be a good thing in the long run, but cuts this big usually don’t happen without some real pain. It feels like Coinbase is heading into a longer restructuring period, and that could hang over the business for a while.

Also, since I’m bullish on Bitcoin (BTC-USD), I just don’t really buy the whole argument that COIN is a proxy for BTC or crypto overall. The argument feels weaker by the day. If you want exposure to Bitcoin, just buy Bitcoin. Coinbase has to deal with regulators, brutal competition, and all the costs that come with running a big exchange. Bitcoin doesn’t have any of that baggage. So why pay extra for the middleman, especially when that middleman is still burning through cash?

The Valuation Trap

Now, the valuation is where the investment case truly falls apart for me. Coinbase is now trading at a market cap of roughly $52 billion, and some people are still calling it a value play. Note that while Q1 free cash flow (FCF) was technically positive at about $165 million, it is anemic. If you annualize that, you get about $660 million, which is miles away from the consensus annual estimate of $2 billion. In fact, I believe that Wall Street’s $2 billion forecast is wildly overblown.

Even if we do give them the benefit of the doubt and assume they hit that $1.95-$2 billion mark, the stock is trading at over 24x forward FCF. That’s quite steep for a traditional financial exchange or capital markets firm, which typically trades at a multiple closer to 15x–20x FCF. However, the market consistently prizes COIN as a high-beta technology and infrastructure play.

That being said, the real “silent killer” here is Stock-Based Compensation (SBC). In Q1 alone, SBC was a whopping figure. This year, it is likely to top $1 billion. The company is essentially printing shares to pay its people, relentlessly diluting shareholders quarter after quarter. When you add back that SBC to the cash flow, you can see why the “positive” FCF is more like a mathematical trick rather than a healthy business result.

Is COIN a Buy, Sell, or Hold?

Wall Street remains relatively optimistic on Coinbase, with a consensus Moderate Buy rating based on 19 Buy, three Hold, and two Sell ratings. Furthermore, COIN’s average price target of $242.57 implies a 11.99% upside over the next 12 months, despite the company’s troubling position, in my view.

Final Thoughts

Coinbase has parts of the story I like, but not enough to make me want to own the stock at this price. Base gives the company a real technology angle, and the derivatives business is becoming more interesting. The problem is that the main business is still heavily tied to crypto trading activity, and that backdrop looks like it is cooling again.

Add in another earnings miss to the mix and relentless dilution from stock-based compensation, and I don’t think the risk/reward is compelling at today’s inflated valuation. For now, I’m staying on the sidelines. I’d rather own Bitcoin directly than pay a middleman.