After suffering a severe downturn during the pandemic, Carnival Corp.’s (CCL) stock has risen nearly 25% in the last year. With bookings on its cruise ships above pre-pandemic 2019 levels, and profits on the rise, there’s reason to believe that the share price of this cruise line operator has more room to run. For this reason, I am bullish on CCL stock.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Travel Demand is Strong

People rushed to travel the moment that Covid-19 lockdowns were lifted, and that momentum has continued into this year, which is a big reason why I am bullish on Carnival. The company delivered $5.8 billion in Q2 2024 revenue, which was 17.7% higher than a year earlier. Carnival, and other cruise line companies, are posting robust revenues as their bookings strengthen. The revenue growth at cruise operators is even surpassing the sales acceleration seen among airlines.

A rising tide appears to be lifting all boats as Carnival competitor Royal Caribbean Cruises (RCL) also posted strong revenue growth in recent quarters, with its sales rising 16.7% year-over-year in this year’s second quarter. Consequently, Royal Caribbean has reinstated its dividend payment to shareholders after suspending it during the pandemic. There’s speculation that Carnival may do the same in the near future.

Carnival’s Improving Metrics

Another reason I’m bullish on Carnival is that the company’s net income is steadily improving. Revenue has completely recovered from the pandemic and should continue to grow in 2025 and beyond. Net income has a ways to go to surpass 2019 levels, but is making strides. This year’s second quarter was a big step in the right direction, as Carnival reported $92 million in net income, improving from a loss a year earlier. Operating income rose five-fold from a year earlier in Q2 to reach $560 million.

Carnival CEO Josh Weinstein said in the company’s Q2 earnings release that demand for cruises continue to accelerate with bookings stretching into 2025 and beyond. The company reported $8.3 billion worth of customer deposits at the end of Q2 this year. That’s a new record and suggests that 2025 will be a very strong year for Carnival. The global cruise industry is forecast to grow at an 11.5% compound annual growth rate (CAGR) from now until 2030. This high growth rate should benefit Carnival as the world’s biggest cruise operator.

Although CCL stock has gained 25% in the last 12 months, the share price remains 61% lower than where it was trading at five years ago before the pandemic struck. However, given the company’s strong bookings and the expected growth in the cruise industry in coming years, there is reason to believe that this security will eventually test new all-time highs.

Is Carnival Stock a Buy?

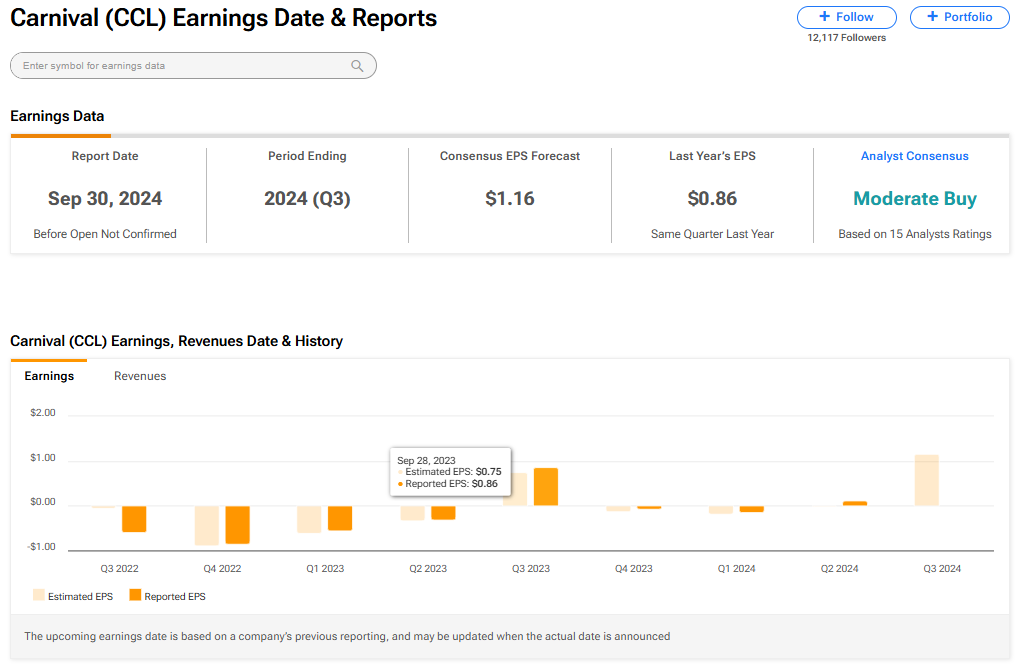

Carnival is currently rated a Moderate Buy among 15 Wall Street analysts who cover the company. That consensus rating is based on 12 Buy, two Hold, and one Sell recommendation made within the last three months. The average price target on CCL stock of $21.64 indicates 15% upside potential from current levels.

Read more analyst ratings on CCL stock

The Bottom Line on CCL Stock

The global cruise industry is enjoying robust demand and Carnival is one of the top beneficiaries. Record bookings and rising revenue portend good things for the company heading into 2025. Carnival’s revenue now exceeds pre-pandemic levels, and its profits are rapidly improving. The company raised its full-year guidance following its Q2 print, and it could reinstate its dividend payment in the near future. For all of these reasons, I remain bullish on CCL stock and see more runway ahead for this security.