Wall Street is bracing for one of the biggest earnings clusters of the year as Microsoft (MSFT), Alphabet (GOOGL), Meta (META), and Amazon (AMZN), a group that is collectively expected to spend $600 billion to $645 billion in AI CapEx in 2026, report results tomorrow, April 29. After a year of record AI spending and OpenAI reportedly missing targets, investors are looking for proof that the massive investments in data centers, GPUs, and AI products are translating into real revenue and profit.

Claim 55% Off TipRanks

Trade AMZN with leverageMSFT: Azure Growth and Copilot Adoption Take Center Stage

Microsoft heads into Q3 earnings with one metric in focus: Azure growth of 38% in constant currency. Anything below that raises concerns about a slowdown in enterprise AI adoption. The bar is even higher as roughly 12% of that growth must come from AI services, everything from model inferencing to Azure OpenAI workloads, to justify Microsoft’s $145 billion annual AI and cloud capex. Investors want evidence that this massive infrastructure buildout is leading to recurring cloud demand.

The company also enters the quarter as the market’s strongest AI winner, but expectations are high. Azure’s AI‑driven workloads, Copilot adoption, and cloud margins will determine whether the company can maintain its lead.

GOOGL: Cloud Margins and $70B Backlog Under the Microscope

Regarding Alphabet’s Q1 earnings, Wall Street expects operating margins above 17%, a sharp turnaround for a business that was losing money not long ago. If the company beats that level, it would show that Google Cloud is becoming a real profit driver.

Another key catalyst is Google Cloud’s $70 billion backlog (RPO). If this grows, it signals that pharma, finance, and other large enterprises are signing long‑term Gemini‑powered contracts, the clearest sign that Google is gaining share in the AI platform race.

At the same time, investors will watch whether AI search features pressure ad revenue and whether rising AI capex is starting to pay off rather than weighing on margins.

Meta: MTIA 450 and a New AI Strategy Drive the Quarter

Meta heads into Q1 earnings with a clear focus on its massive $115 billion to $135 billion capex guide. This spending cycle is all about the company’s shift toward proprietary AI infrastructure, highlighted by the new MTIA 450 chip. After years of open-sourcing its top models, Meta is shifting to a more controlled, API‑driven approach for its high‑end Llama 4 versions, a move meant to protect its technology and create a clearer path to monetization.

Despite the heavy investment, Meta still carries the strongest margin profile among the Big Techs. Its AI‑powered ad‑targeting engine, Advantage+, is delivering record ROI for small businesses, helping offset the cost of its AI buildout. Investors are looking for clues as to whether Meta can balance this shift toward proprietary AI with continued efficiency.

AMZN: Trainium3 Demand and AWS Momentum Take the Spotlight

Amazon’s Q1 earnings will center on whether AWS can keep pace with Microsoft Azure. To do that, AWS needs revenue growth above 25%, which would signal strong demand for AI‑driven cloud workloads. The spotlight is also on Trainium3, AMZN’s new 3nm custom AI chip, which is reportedly “nearly fully subscribed.” That suggests AWS is becoming a go‑to platform for cost‑efficient, high‑performance AI training at scale.

The bigger reveal came from CEO Andy Jassy, who hinted that Amazon’s custom chip portfolio, including Graviton, Trainium, and Nitro, is now over a $20 billion run-rate business on its own. That position makes AMZN a key semiconductor player. If AWS growth and Trainium3 adoption keep surging, investors may start valuing Amazon not just as an e‑commerce and cloud leader, but as a vertically integrated AI chip company with major long‑term leverage.

Bottom Line

Together, these four companies are pouring billions of dollars each quarter into AI infrastructure. Tomorrow’s results will show whether massive AI spending generates sufficient revenue growth, or if a cash flow squeeze threatens shareholder returns.

For now, expectations are high, and so are the risks. With valuations stretched and AI optimism priced in, Big Tech needs to deliver more than hype.

What Is the Best AI Stock to Buy Now?

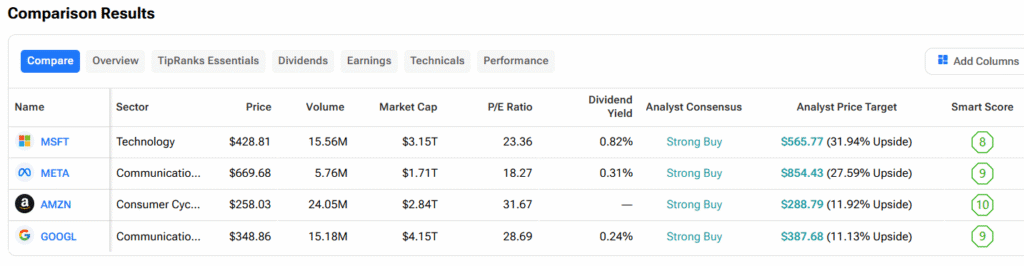

We used TipRanks’ Comparison Tool to see which of the above-mentioned AI stocks analysts favor. According to analysts, MSFT stock has the highest upside potential of 31.94%.