Earnings season is upon us, with some of the biggest companies around reporting last week. Apple (NASDAQ:AAPL) was among those the market was eagerly anticipating.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The company’s total sales clocked in at $111.2 billion, a 17% year-over-year increase and a new record for the post-holiday quarter. Leading the charge was iPhone revenue at $57 billion, which was up 21.7% from the prior year.

Apple also hit a new all-time peak for services revenue, which grew by 16% year-over-year to $31 billion. The company seems set to extend its hit streak in the current quarter as well, guiding for year-over-year revenue growth of 14% to 17% in fiscal Q3 2026.

Apple’s growth was reflected across the ecosystem, with a number of big tech firms reporting expanding revenues. Synthesizing the data, top investor Daniel Sparks is saving his biggest stamp of approval for Apple.

“I think Apple was the best report of the bunch,” states the 5-star investor, who is among the top 1% of stock pros covered by TipRanks.

Sparks cites a number of reasons for his bullish view, with Apple’s disciplined spending practices high on the list. The investor points out that while the headlines for the other companies “all looked great,” Apple is the only one that isn’t committing to enormous capex spending.

In fact, Apple is moving in the opposite direction, as its capex for the first half of fiscal 2026 was $4.3 billion, a decrease from the $6 billion it spent in the same timeframe during 2025. That contrasts dramatically with the hundreds of billions of dollars that the hyperscalers are planning to spend this year.

“That could become a meaningful free cash flow advantage if Apple can still deliver good AI to its users without spending like its peers are,” adds Sparks.

The investor is also encouraged by Apple’s year-over-year revenue growth and Q3 guidance, while also noting that the high-margin services business segment is “accelerating.” Apple’s installed global base of more than 2.5 billion devices provides fertile ground for the company to continue “feeding its services business.”

Lastly, Sparks likes the company’s upcoming product launches, including the “more personalized Siri” that CEO Tim Cook announced is slated for later this year.

With a price-to-earnings ratio in the 30s, Sparks does acknowledge that AAPL is not cheap. Still, he believes Apple’s accelerating revenues and servcies — and its success in sidesteppng the AI spending race — makes the premium valuation worthwhile. (To watch Sparks’ track record, click here)

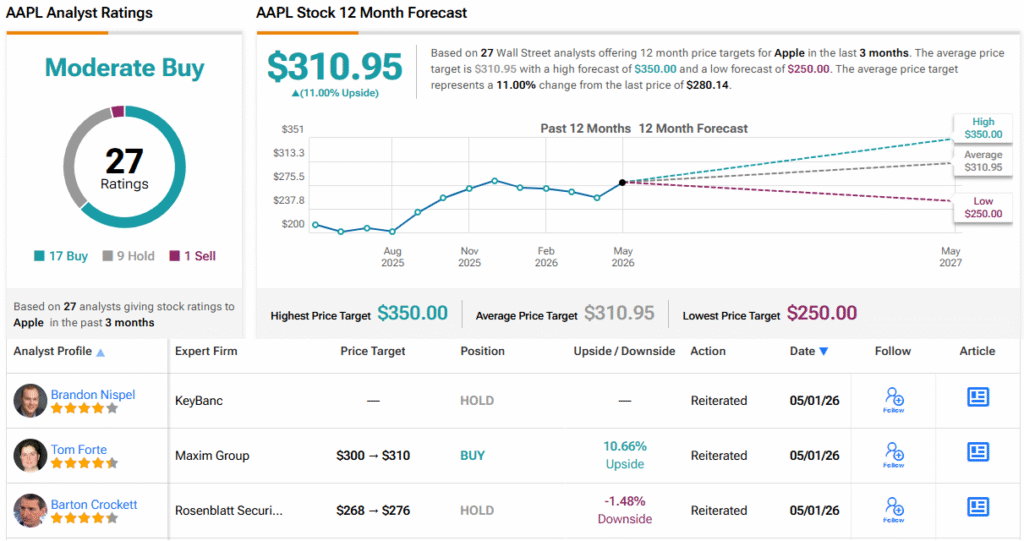

Wall Street is feeling pretty good about Apple as well. With 17 Buys, 9 Holds, and 1 Sell, AAPL enjoys a Moderate Buy consensus rating. Its 12-month average price target of $310.95 points to an upside of 11%. (See AAPL stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.