Baidu (BIDU) is a China-based tech firm best known for search, AI cloud, robotaxi service Apollo Go, and its ERNIE AI tools. The company is set to report Q1 2026 results tomorrow, on May 18, with Wall Street looking for EPS of $1.70, down from $2.72 in the same quarter last year. That drop sets a clear tone for the print: investors want to see whether AI growth can start to offset weak ad trends and heavy spend.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Baidu shares have had a rough stretch before the report. The stock closed at $135.33 on Friday, down 5.56% for the day.

AI Cloud and Apollo Go Remain the Main Bull Case

The main focus will likely be on Baidu’s AI shift. On the last call, management said AI would remain the key growth driver in 2026 and said AI Cloud Infra should “maintain strong momentum.” That matters because AI Cloud Infra revenue reached about ¥20 billion in 2025, up 34% from the prior year. In Q4, subscription-based AI accelerator revenue rose 143% year-over-year.

Baidu also said its core AI-powered business generated more than ¥11 billion in Q4 and accounted for 43% of Baidu General Business revenue. Management added that this AI-powered unit could become the majority of Baidu General Business in the “foreseeable future.” That line will be important again this quarter, since investors want proof that AI is not just a cost center, but a real revenue driver.

Apollo Go is another key part of the story. The robotaxi unit delivered 3.4 million fully driverless rides in Q4 and more than 10 million in 2025. Baidu also said total rides had topped 20 million by February 2026, with service across 26 cities. In this report, investors will likely look for signs that more cities are moving closer to better unit economics.

The Bear Case Is Still About Ads and Spending

Even so, Baidu still has some clear issues to solve. The company reported a 3% decline in revenue for the full year 2025. It also booked a ¥16.2 billion impairment charge, which pushed it to a GAAP operating loss for the year. On top of that, the cost of revenue and AI-related spend remain high.

The near-term risk is simple. If ad demand stays weak while AI spend remains heavy, profit growth may stay under pressure. Analysts also flagged ad headwinds, increased competition for AI user traffic, and softer macro demand as key risks. These points could weigh on the stock if Q1 results show slow core growth or weak margins.

That said, Baidu still has a large balance sheet. It ended 2025 with ¥294.1 billion in cash and investments. It also announced a new $5 billion buyback plan and its first dividend policy, which could help support investor trust while the AI shift plays out.

Overall, Baidu’s Q1 report is less about one quarter of earnings and more about proof of progress. If AI Cloud, Apollo Go, and AI apps continue to scale, the stock could maintain its bullish case. However, if ad weakness and spending pressure take the lead again, investors may stay cautious even with the stock still trading below the average analyst target.

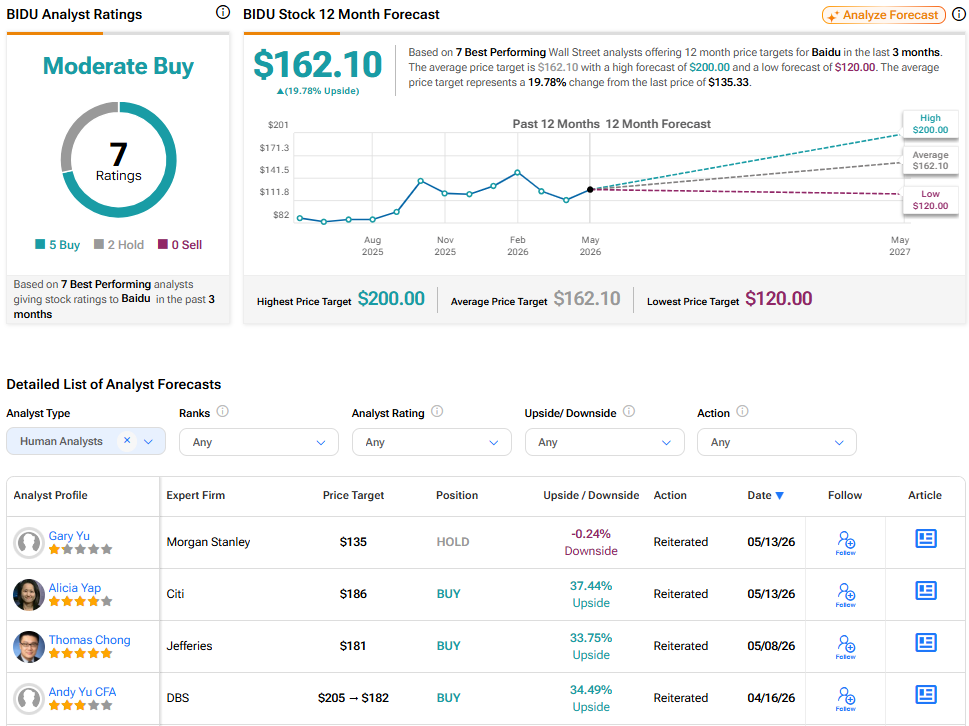

Is BIDU a Good Stock to Buy Now?

On the Street, analysts remain fairly upbeat about Baidu with a Moderate Buy consensus, based on seven top analyst ratings. The average BIDU stock price target is $162.10, implying about a 19.78% upside from the current price.