Two chip giants are chasing the same AI opportunity, but only one has the clearer path to turning that demand into durable growth. Qualcomm (QCOM) has a promising data center and AI story, especially as it tries to diversify away from smartphones, but the company still has to prove that this pivot can offset losses in Apple modem share, soft Android demand, and rising competition. However, Broadcom (AVGO) already appears deeply embedded in the AI infrastructure buildout through custom silicon, networking, and major hyperscaler demand. So between the two, analysts see Broadcom as the better buy.

Claim 55% Off TipRanks

New trading tool for NVDA bearsWhy Broadcom Stock (AVGO) Is a Good Buy

The analyst case for Broadcom is much cleaner than the case for Qualcomm. Most analysts view Broadcom as one of the best-positioned semiconductor companies for the AI infrastructure boom, especially because of its strength in custom AI chips, networking, and enterprise software. The key difference is that Broadcom is not just telling investors it wants to become a bigger AI player. Analysts already see real demand from hyperscalers, and it’s showing up in the numbers.

Here are the key comments on Broadcom from top-rated analysts:

- Citigroup (C) named Broadcom its “#1 Semis Pick in 2026,” with analyst Atif Malik raising his price target to $500 from $475. Citi pointed to better earnings and revenue visibility through Fiscal 2028, supported by Broadcom’s enterprise software base and strong hyperscaler demand for custom AI chips.

- Wells Fargo’s (WFC) Aaron Rakers raised his Broadcom price target to $545 from $430. The analyst said that Broadcom’s AI-related semiconductor revenue is tracking 30% to 40% above prior Wall Street expectations, which supports the idea that estimates may still have room to move higher.

- Baird analyst Tristan Gerra issued a Street-high price target of $630. His bullish view is tied to Broadcom’s multi-year custom AI chip contracts with major customers like Google (GOOGL) and Meta (META), including a new 2-nanometer partnership with Meta.

Overall, analysts see a clearer path to large-scale revenue growth. The stock is not cheap, but analysts appear willing to give Broadcom a premium multiple because the company is deeply embedded in the AI infrastructure supply chain. That makes Broadcom the better buy in this comparison, as evident in the analysts’ recommendation trends shown below, where the number of Strong Buy ratings has increased.

Why Qualcomm Stock (QCOM) Is Currently a Hold

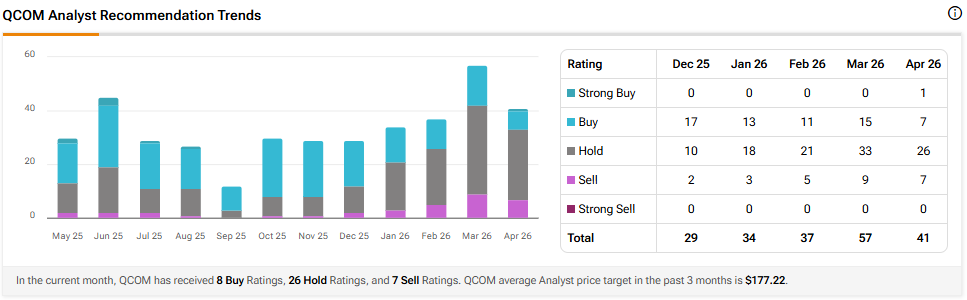

However, when it comes to Qualcomm, analysts are more divided. For instance, bulls believe that the company is moving past smartphones and could become a more important player in AI, custom silicon, and data centers. Still, bears argue that the stock has already priced in too much optimism. That is why Qualcomm has a Hold consensus instead of the wide analyst support that Broadcom enjoys.

Here are the key bullish analyst comments on Qualcomm:

- Daiwa Securities upgraded Qualcomm to Outperform and set a $225 target. The firm’s bullish view is based on Qualcomm’s data center AI pivot and the possibility that the company can enter a much larger addressable market.

- Tigress Financial’s Ivan Feinseth reiterated a Buy rating with a $280 target, one of the highest targets on Wall Street. The firm pointed to Qualcomm’s opportunity in advanced AI infrastructure.

- Argus and TD Cowen (TD) also remain positive. Argus’s Jim Kelleher issued a $220 target, while TD Cowen’s Joshua Buchalter raised its target from $150 to $200, with both analysts highlighting Qualcomm’s solid underlying fiscal fundamentals.

However, the bearish side of the Qualcomm debate is hard to ignore:

- Mizuho (MFG) analysts, led by Vijay Rakesh, warned that Qualcomm is losing its premium share of Apple’s (AAPL) modem business. They also pointed to softness in the broader Android market and warned that Qualcomm’s Windows processor push will face fierce competition from Nvidia (NVDA).

- Wells Fargo and UBS (UBS) downgraded Qualcomm to Sell. Their concern is that a forward P/E multiple above 20x looks too expensive for a company that’s facing near-term negative earnings growth.

- DZ Bank downgraded Qualcomm to Hold with a $195 target. Analyst Ingo Wermann pointed to tougher competition in AI infrastructure and said that Qualcomm still needs to prove it can scale that opportunity profitably.

And there lies the main issue with Qualcomm. The upside potential is there, but it is still more speculative than Broadcom’s outlook. Therefore, although Qualcomm may eventually become a bigger player in AI infrastructure, analysts are clearly split on how much credit the stock deserves today. This is evident in the analysts’ recommendation trends shown below, where the number of Hold and Sell ratings has increased, while the number of Buy ratings has decreased.

AVGO and QCOM Consensus Price Targets

Overall, out of the two chip stocks mentioned above, analysts think that AVGO stock has more room to run than QCOM. In fact, AVGO’s price target of $473.74 per share implies 11.4% upside versus QCOM’s 12% downside risk.